With US valuations ostensibly high compared to global peers, many investors are asking themselves if now is the time to dip their toes into international equities. They’re asking the wrong question. It’s better to focus instead on optimal sector allocation. After all, international stocks are mostly just a means of diluting one’s exposure to technology companies.

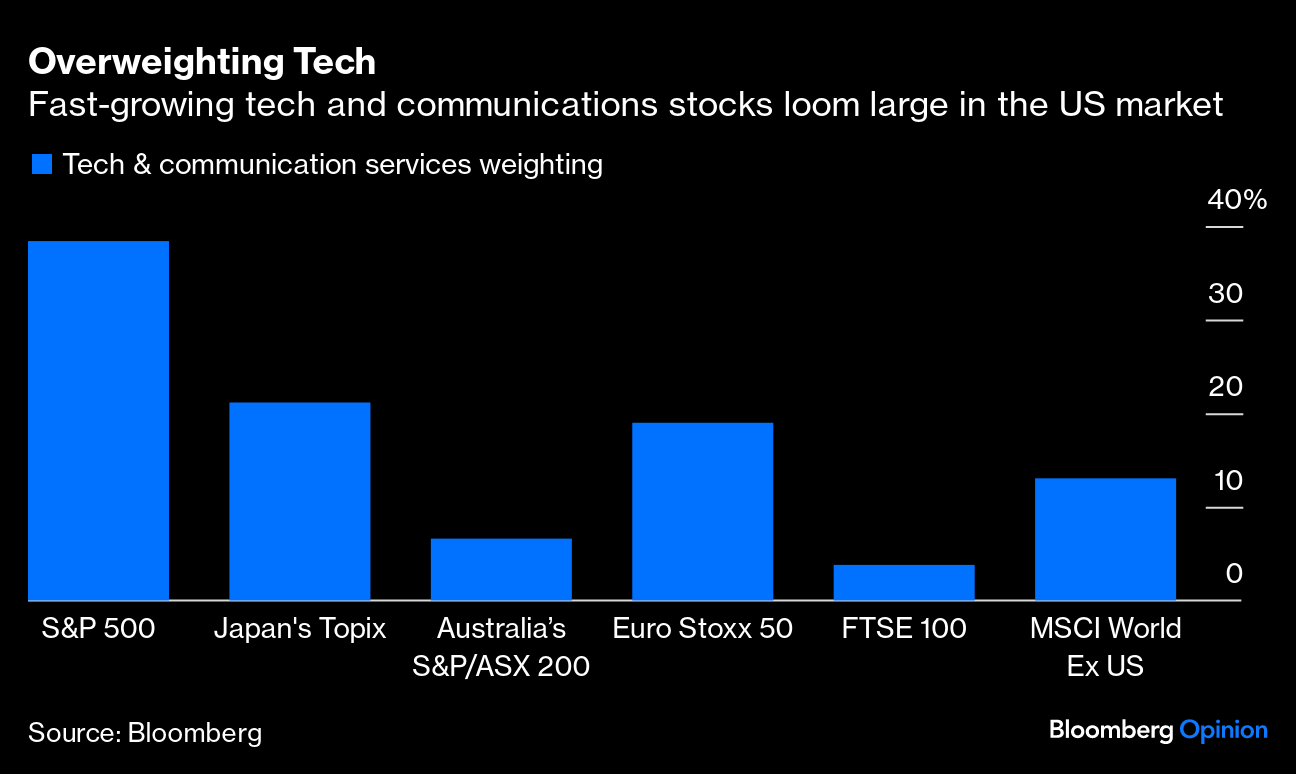

In fact, the entire narrative about “relatively expensive” US stocks is a bit misleading. The S&P 500 trades at about 20 times forward earnings, versus about 14 times for all other developed markets. The US index looks expensive principally because it has the largest weightings in tech (Nvidia Corp., Microsoft Corp., etc.) and communication services (Meta Platforms Inc., Alphabet Inc., etc.) by a wide margin. Those categories make up about 38% of the S&P 500, and just about 13% for the rest of the developed world. In America, as in other countries, investors have been willing to pay up for the potential, however uncertain, that strong growth in those sectors will continue.

Investing in Japan’s broad equity indexes, on the other hand, translates to a heavy concentration in the industrial sector; for Europe, it’s financials and consumer discretionary; while Australia has more than half of its index weight in financials and materials.

Looking back at history, it’s understandable that investors have come to think about diversification in geographic terms. US stocks have trounced the rest of the world for about 15 years, and there’s a temptation to believe that secular trends must necessarily die of old age. Past periods of US outperformance (1989-1992; 1995-1999) have been considerably shorter and have tended to be followed by underperformance (1993-1994; 2000; 2002-2008).

Yet the growth of global trade and the emergence of multinational giants have made decisions about “country allocation” less relevant than they were in the past, and fast-moving markets tend to zap away any cross-border relative-value arbitrage opportunities as fast as they can appear.

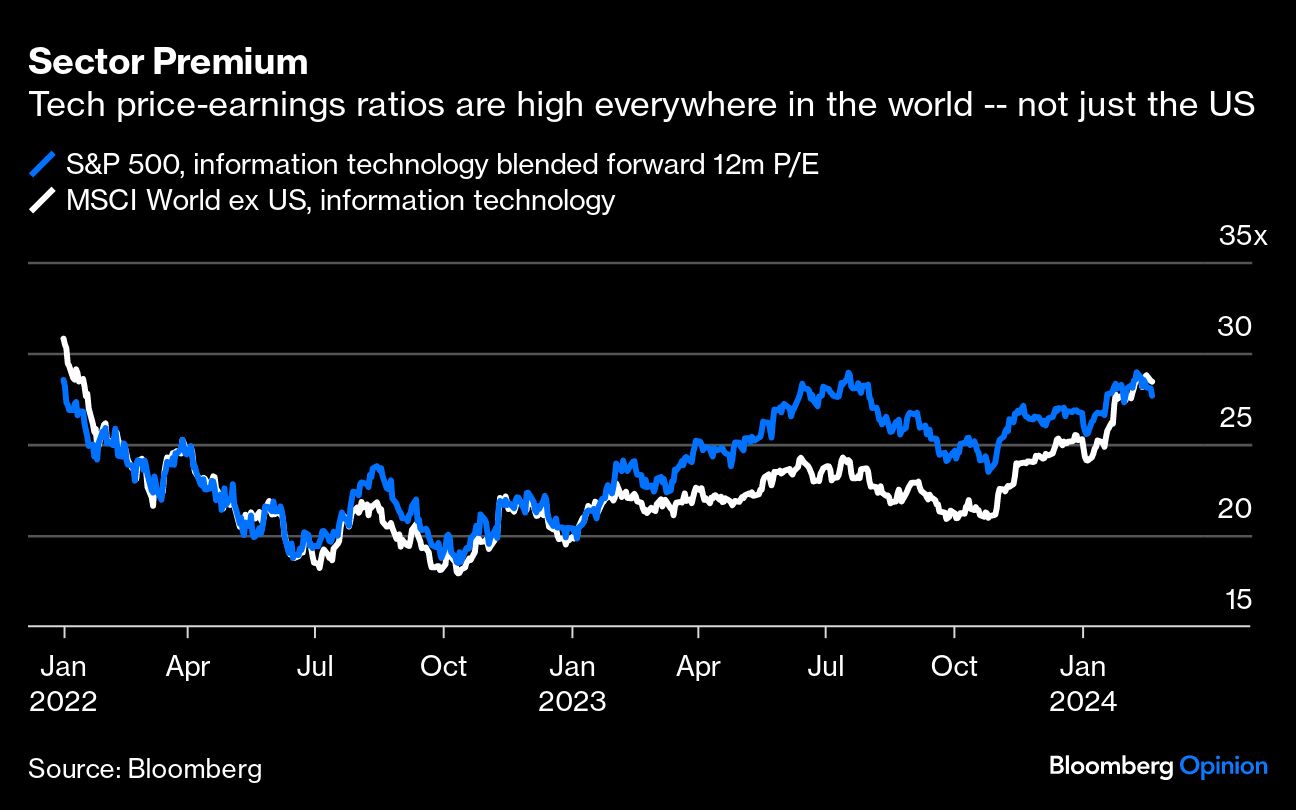

Case in point: on an apples-to-apples basis, US tech — for all the handwringing about its valuations — actually trades at roughly the same price-earnings multiples as its developed market peer group.

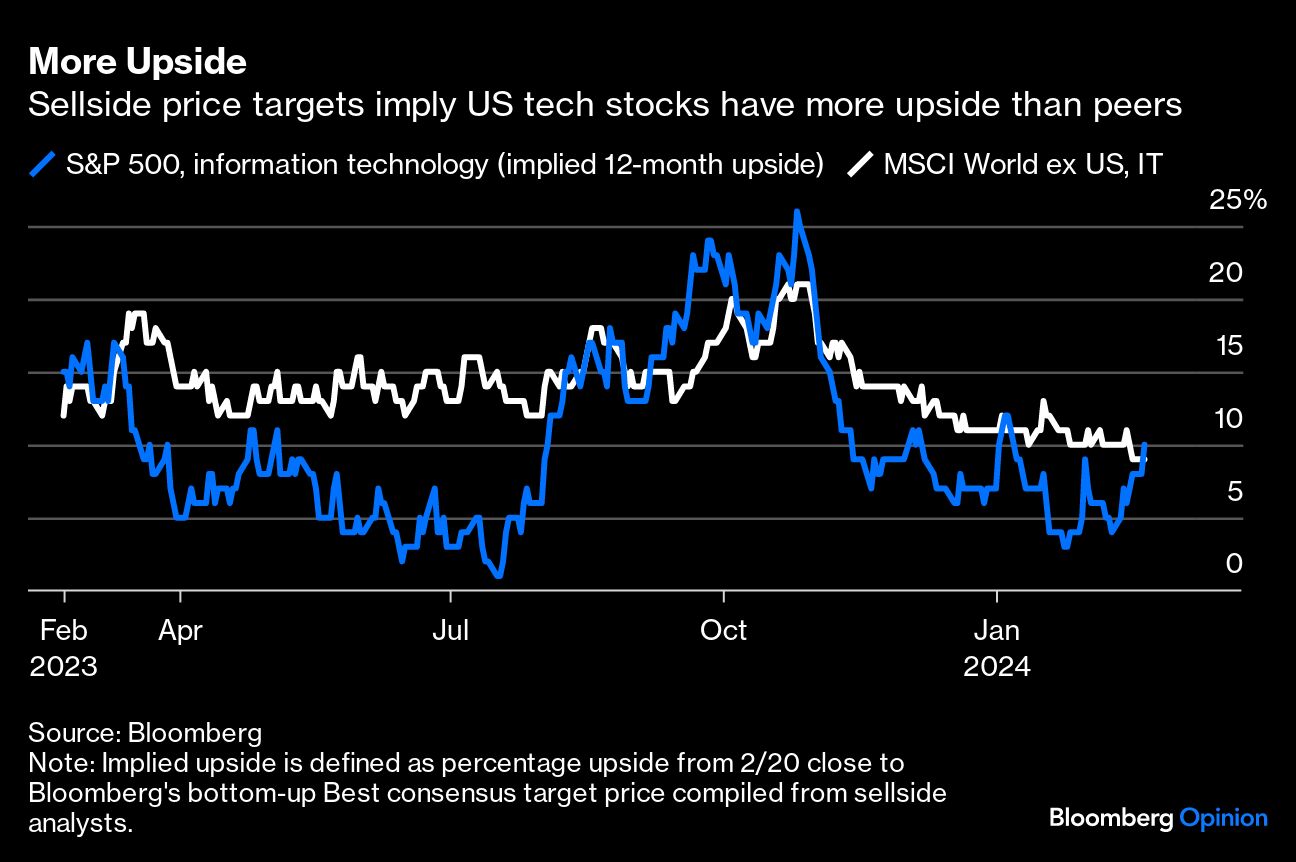

And according to sell-side analysts, the two tech groups have very comparable upside today, looking 12 months out1.

International equities also come with currency risk. Not only have international stocks underperformed the US for a decade and a half, but their returns have been even worse in dollar terms. With the Federal Reserve preparing to lower policy rates later this year, there may be good reasons to expect that trend to change in the short-term. Over a longer horizon, however, the momentum of King Dollar still looks overwhelming.

Emerging markets are a slightly different animal. By definition, they have idiosyncratic and difficult-to-price risks related to local governments and those may, on occasion, create opportunities for investors that understand them better than the crowd — and perils for those who don’t. (It’s worth reading my Bloomberg Opinion colleague Shuli Ren’s recent column that describes China, the king of emerging markets, as a value trap.)

Clearly, there are good reasons to think hard about diversification. There’s no denying that investors blindly buying the S&P 500 today are tying their fortunes to the fate of a handful of uber-dynamic (and also intrinsically risky) growth stocks, which have thrilled shareholders in the past but polarize Wall Street analysts today.

The so-called Magnificent Seven stocks alone (five of them fall under the tech and communications rubric) have accounted for a third of the benchmark’s post-financial-crisis gain. Nvidia itself has the potential to swing full-year index returns by several percentage points in either direction following a stunning 239% rally last year. Its enviable performance was on display again Wednesday, when the poster child for artificial intelligence predicted another massive sales gain for the current quarter, helping to justify its place among the world’s most-valuable companies.

For investors jittery about high US valuations, a straightforward solution is simply to underweight the richest US stocks and sectors. A diet version of this strategy is to own the equal-weighted version of the S&P 500, while another is to sell some tech holdings and buy discounted sectors such as energy. Another group may decide to keep their chips on the most dynamic stocks of the past 15 years.

Certainly, there are very special situations when country diversification makes sense. If war or economic sanctions are in the offing, it would be senseless to ignore the country of risk. Ditto major corporate tax reforms. But the discourse today seems to be primarily about rich valuations, and international equities simply aren’t a silver bullet for that problem, which is best addressed through sector reallocation right here in the US.

1My standard disclaimer applies here: this is based on consensus price targets from sellside analysts. I think they contain information about risks and growth prospects that aren't captured by simple price/earnings ratios. But I also know that consensus price targets historically have a bullish tilt, so I take them with a grain of salt.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More Active Management Topics >