Flawed Valuations Threaten $1.7 Trillion Private Credit Boom

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsColm Kelleher whipped up a storm at the end of last year when the UBS Group AG chairman warned of a dangerous bubble in private credit. As investors dive headfirst into this booming asset class, the more urgent question for regulators is how anybody could even know for sure what it’s really worth.

The meteoric rise of private credit funds has been powered by a simple pitch to the insurers and pensions who manage people’s money over decades: Invest in our loans and avoid the price gyrations of rival types of corporate finance. The loans will trade so rarely — in many cases, never — that their value will stay steady, letting backers enjoy bountiful and stress-free returns. This irresistible proposal has transformed a Wall Street backwater into a $1.7 trillion market.

Now, though, cracks in that edifice are starting to appear.

Central bankers’ rapid-fire rate hikes over the past two years have strained the finances of corporate borrowers, making it hard for many of them to keep up with interest payments. Suddenly, a prime virtue of private credit — letting these funds decide themselves what their loans are worth rather than exposing them to public markets — is looking like one of its greatest potential flaws.

Colm Kelleher, chairman of UBS Group AG, speaks at the company's annual general meeting of shareholders in Basel, Switzerland, on Wednesday, April 5, 2023. UBS's reported plan to lay off as many as 36,000 workers would make it the company with the largest job cuts globally in the past six months. Photographer: Stefan Wermuth/Bloomberg.

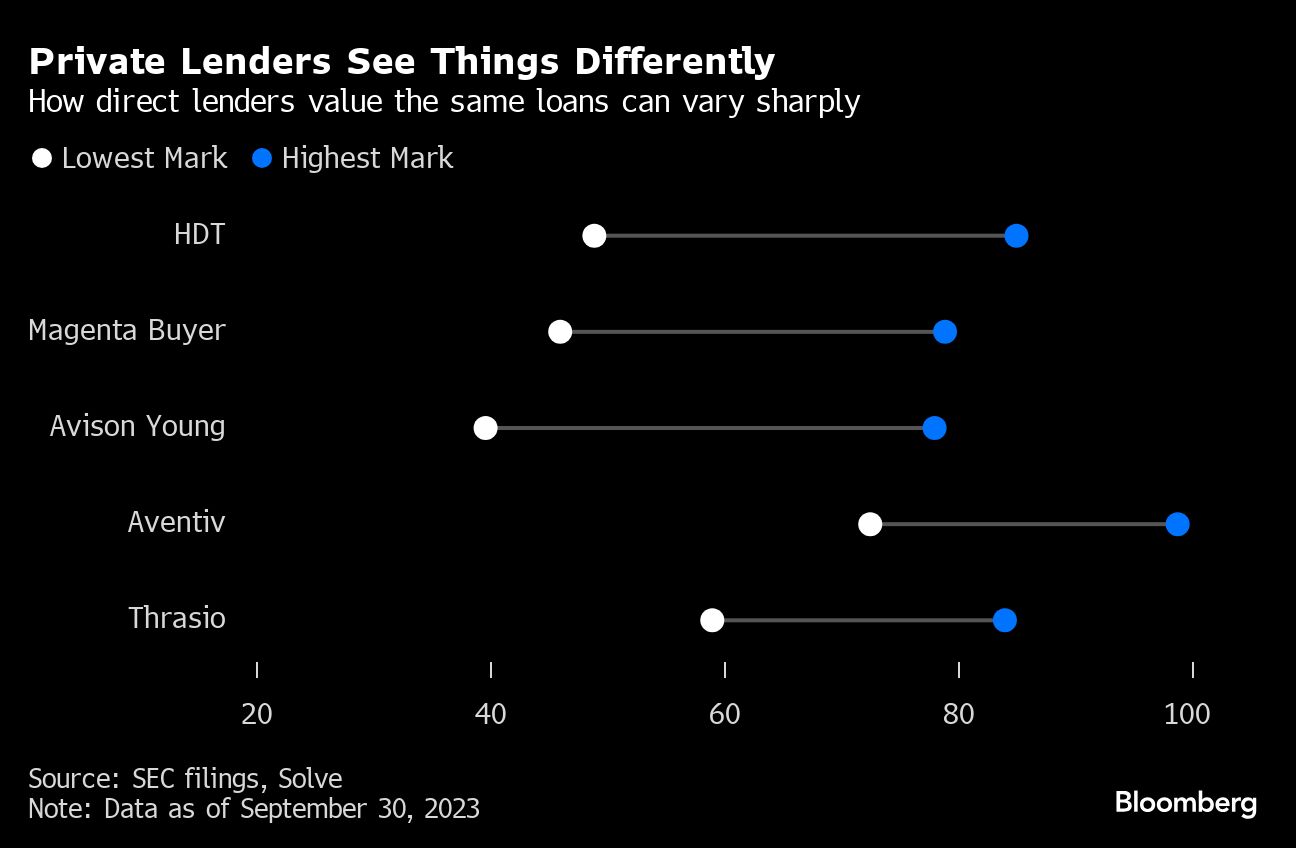

Data compiled by Bloomberg and fixed-income specialist Solve, as well as conversations with dozens of market participants, highlight how some private-fund managers have barely budged on where they “mark” certain loans even as rivals who own the same debt have slashed its value.

In one loan to Magenta Buyer, the issuing vehicle of a cybersecurity company, the highest mark from a private lender at the end of September was 79 cents, showing how much it would expect to recoup for each dollar lent. The lowest mark was 46 cents, deep in distressed territory. HDT, an aerospace supplier, was valued on the same date between 85 cents and 49 cents.

This lack of clarity on what an asset’s worth is a regular complaint in private markets, and that’s spooking regulators. While nobody cared too much when central bank interest rates were close to zero, today financial watchdogs are fretting that the absence of consensus may be hiding more loans in trouble.

“In private markets, because no one knows the true valuation there’s a tendency to leak information into prices slowly,” says Peter Hecht, managing director at US investment firm AQR Capital Management. “It dampens volatility, giving this false perception of low risk.”

The private-lending funds and companies mentioned in this story all declined to comment, or didn’t respond to requests for a comment.

Code of Silence?

Private credit was embraced at first for shifting risky company loans away from systemically important Wall Street banks and into specialist firms, but the ardor’s cooling in some quarters. Regulators are doubly nervous because of the economy’s febrile state. These funds charge interest pegged to base rates, which has handed them bumper profits — and made their borrowers vulnerable.

“As interest rates have risen, so has the riskiness of borrowers,” Lee Foulger, the Bank of England’s director of financial stability, strategy and risk, said in a recent speech. “Lagged or opaque valuations could increase the chance of an abrupt reassessment of risks or to sharp and correlated falls in value, particularly if further shocks materialize.”

Values are especially cloudy outside the US, because of poor transparency. And it’s the same for loans made by funds that don’t publish quarterly updates or where there’s a single lender with no one to judge them against.

Tyler Gellasch, head of the Healthy Markets Association, a trade group that includes pension funds and other asset managers, says policymakers have been caught napping. “This is simply a regulatory failure,” says Gellasch, who helped draft part of the Dodd-Frank Wall Street reforms after the financial crisis. “If private funds had to comply with the same fair value rules as mutual funds, investors could have a lot more confidence.”

The Securities and Exchange Commission has nevertheless begun to pay closer attention, rushing in rules to force private-fund advisers to allow external audits as an “important check” on asset values.

The SEC headquarters in Washington, DC. Photographer: Graeme Sloan/Bloomberg

Some market participants wonder, however, whether the fog around pricing suits investors just fine. Several fund managers, who requested anonymity when speaking for fear of endangering client relationships, say rather than wanting more disclosure, many backers share the desire to keep marks steady — prompting concerns about a code of silence between lenders and the insurers, sovereign wealth funds and pensions who’ve piled into the asset class.

One executive at a top European insurer says investors could face a nasty reckoning at the end of a loan’s term, when they can’t avoid booking any value shortfall. A fund manager who worked at one of the world’s biggest pension schemes, and who also wanted to remain anonymous, says valuations of private loan investments were tied to his team’s bonuses, and outside evaluators were given inconsistent access to information.

Red Flags

The thinly traded nature of this market may make it nigh-on impossible for most outsiders to get a clear picture of what these assets are worth, but red flags are easier to spot. Take the recent spike in so-called “payment in kind” (or PIK) deals, where a company chooses to defer interest payments to its direct lender and promises to make up for it in its final loan settlement.

This option of kicking the can down the road is often used by lower-rated borrowers and while it doesn’t necessarily signal distress, it does cause anxiety about what it might be obscuring. “People underestimate how dangerous PIK products are,” says Benoit Soler, a senior portfolio manager at Keren Finance in Paris, pointing out the sometimes enormous cost of deferring interest: “It can embed a huge forward risk for the company.”

And yet the value of loans even after these deals is strikingly generous. According to Solve, about three-quarters of PIK loans were valued at more than 95 cents on the dollar at the end of September. “This raises questions about how portfolio companies struggling with interest servicing are valued so high,” says Eugene Grinberg, the fintech’s cofounder.

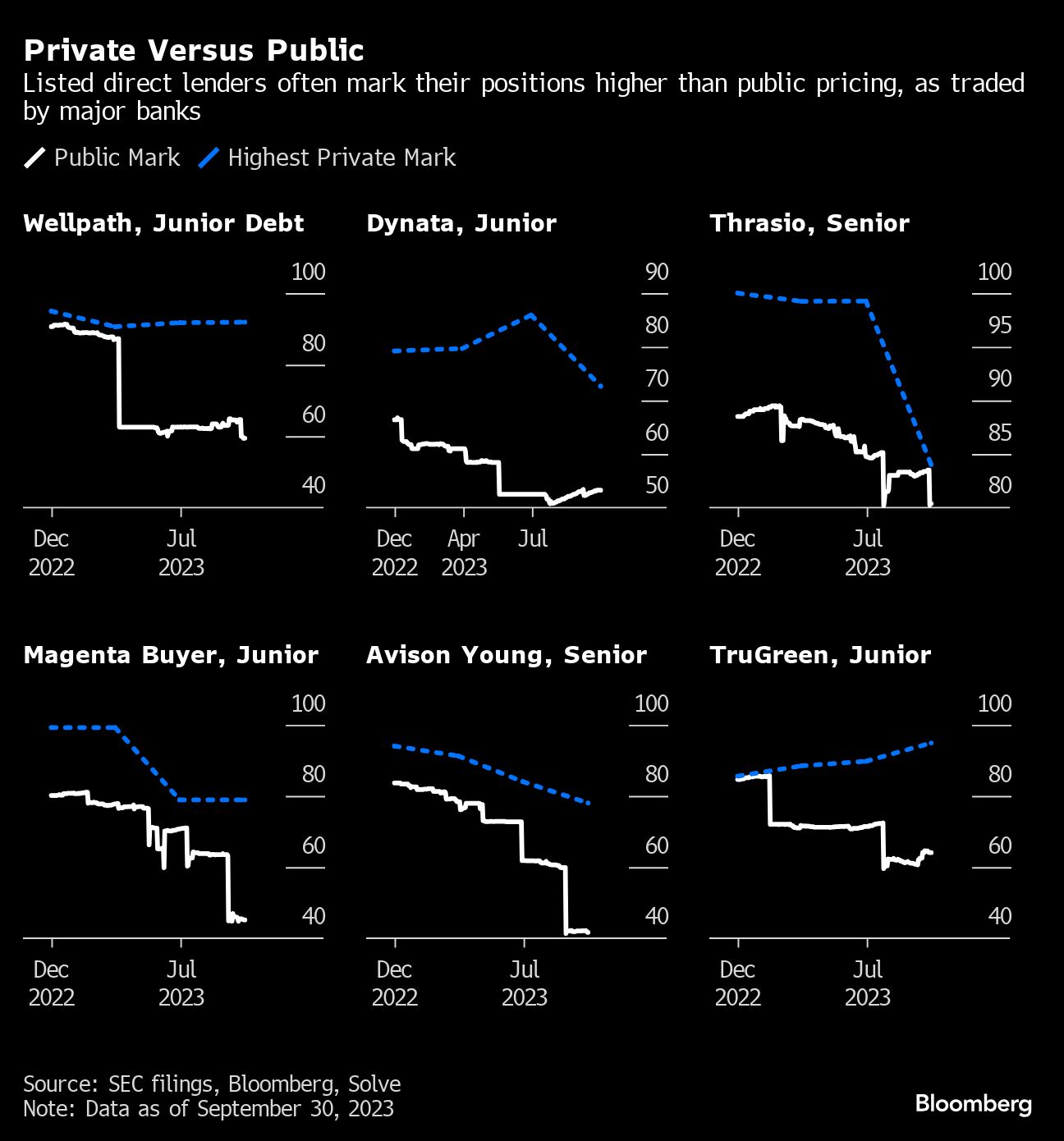

An equally perplexing sign is the number of private funds who own publicly traded loans, and still value them much more highly than where the same loan is quoted in the public market.

In a recent example, Carlyle Group Inc.’s direct-lending arm helped provide a “second lien” junior loan to a US lawn-treatment specialist, TruGreen, marking the debt at 95 cents on the dollar in its filing at the end of September. The debt, which is publicly traded, was priced at about 70 cents by a mutual fund at the time. Most private credit portfolios “remain above their public market peers,” the BoE’s Foulger noted in his speech on “nonbank” lenders.

And it’s not just the comparison with public prices that is sometimes out of whack. As with Magenta Buyer and HDT there are eye-catching cases of separate private credit firms seeing the same debt very differently. Thrasio is an e-commerce business whose loan valuations have been almost as varied as the panoply of product brands that it sells on Amazon, which runs from insect traps and pillows to cocktail shakers and radio-controlled monster trucks.

As the company has struggled lately, its lenders have been divided on its prospects. Bain Capital and Oaktree Capital Management priced its loans at 65 cents and 79 cents respectively at the close of September. Two BlackRock Inc. funds didn’t even agree: One valuing its loan at 71 cents, the other at 75 cents. Monroe Capital was chief optimist, marking the debt at 84 cents. Goldman Sachs Group Inc.’s asset management arm had it at 59 cents.

The Wall Street bank seems to have made the shrewder call. Thrasio filed for Chapter 11 on Wednesday as part of a debt restructuring deal and one of its public loans is quoted well below 50 cents, according to market participants. Oaktree lowered its mark to 60 cents in December.

“Dispersions widen when a company is falling into distress as well as when a lot of funds are marking the same asset,” says Bloomberg Intelligence analyst Ethan Kaye. “When a company is either stressed or distressed, it becomes less certain as to what future cash flows might look like.”

In an analysis of Pitchbook data from the end of September, Kaye found that in one in 10 cases where the same debt was held by two or more funds, the price gap was at least 3%. When three of four funds own the same loan, something that’s common in this industry, the differences get starker still.

Distressed companies do throw up some especially surprising values. Progrexion, a credit-services provider, filed for bankruptcy in June after losing a long-running lawsuit against the US Consumer Financial Protection Bureau. Its bankruptcy court filing estimated that creditors at the front of the queue would get back 89% of their money. Later that month its New York-based lender Prospect Capital Corp. marked the senior debt at 100 cents.

In data pulled together by Solve on the widest gaps between how a lender marks its loans versus other parties’ valuations, Prospect’s name appears more regularly than most. BI finds that smaller firms in general appear to mark their loans more aggressively.

“There are big differences in how managers approach valuations, and a lack of transparency and comparability between them,” says Florian Hofer, director for private debt at Golding Capital Partners, an alternative investment firm.

Private Fans

For private credit’s many champions, the criticism’s overblown. Fund managers argue that they don’t need to be as brutal on marking down prices because direct loans usually involve only one or a handful of lenders, giving them much more control during tough times. In their eyes, the beauty of this asset class is that they don’t have to jump every time there’s a bump in the road.

Some investors point as well to the shortcomings of the leveraged-loan market, private credit’s biggest rival as a source of corporate finance, where Wall Street banks gather large syndicates of mainstream lenders to fund companies.

“There are a lot of technicals that influence the broadly syndicated loan market, like sales encouraged by ratings downgrades or investors getting out of certain sectors,” says Karen Simeone, managing director at private markets investor HarbourVest Partners. “You don't get this in private credit and so I do think it makes sense that these valuations are less volatile.”

Direct lenders also use far less borrowed money than bank rivals, giving regulators some comfort that any market blowup could be contained. They typically lock in cash they get from investors for much longer periods than banks, and they don’t tap customer deposits to pay for their risky lending. They tend to have better creditor protections, too.

Third-party advisers such as Houlihan Lokey and Lincoln International are increasingly assessing loan marks, adding scrutiny, though it’s paid for by the funds and is no panacea. “We don't always get unfettered access to credits,” says Timothy Kang, co-lead of Houlihan’s private credit valuation practice. “Some managers have access to more information than others.”

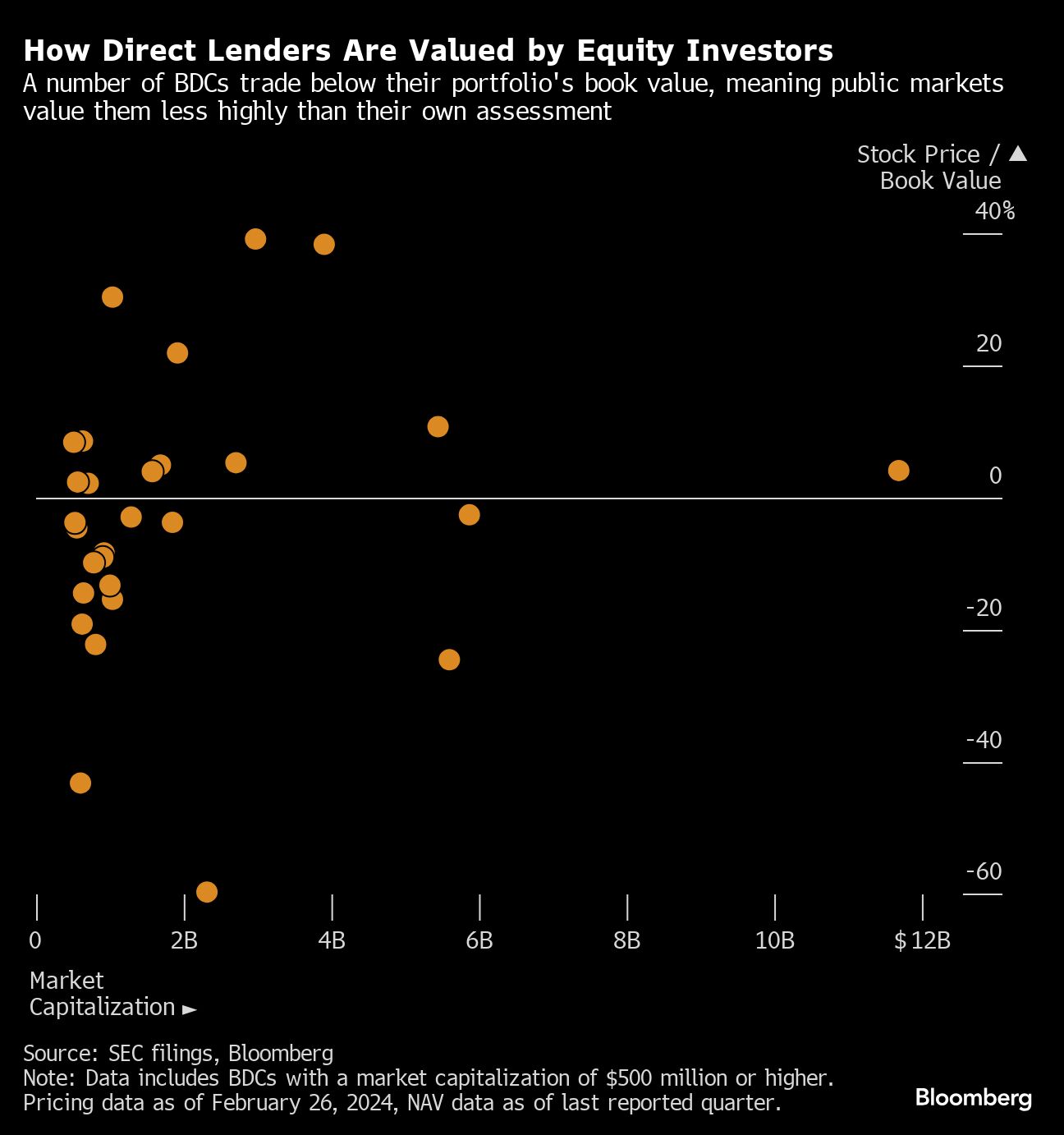

In the US, direct lenders often set up as publicly listed “business development companies,” requiring them to update their investors every quarter. BDCs do give better visibility on their loan prices but their fund managers are paid according to the portfolio’s worth so there’s an incentive to mark debt high.

“Part of the problem stems from the decision makers for portfolio marks, which include the third-party valuation firms and the BDC boards, who have a lot to lose if they decide not to play along,” says Finian O’Shea of Wells Fargo Securities, a BDC analyst.

For Hecht at AQR the real fear isn’t so much the wilder cases of value gaps, more that the very purpose of private credit is lending to risky businesses and that isn’t shown in overall asset values, echoing the UBS chairman’s lament.

“The part I’m also worried about is for normal credit risk environments where they mark nearly all assets at 100,” he says. “Most of the time, people are looking at these asset valuations and thinking they have no risk.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Read more articles by Silas Brown, Laura Benitez, John Sage, Kat Hidalgo, Ellen Schneider

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All