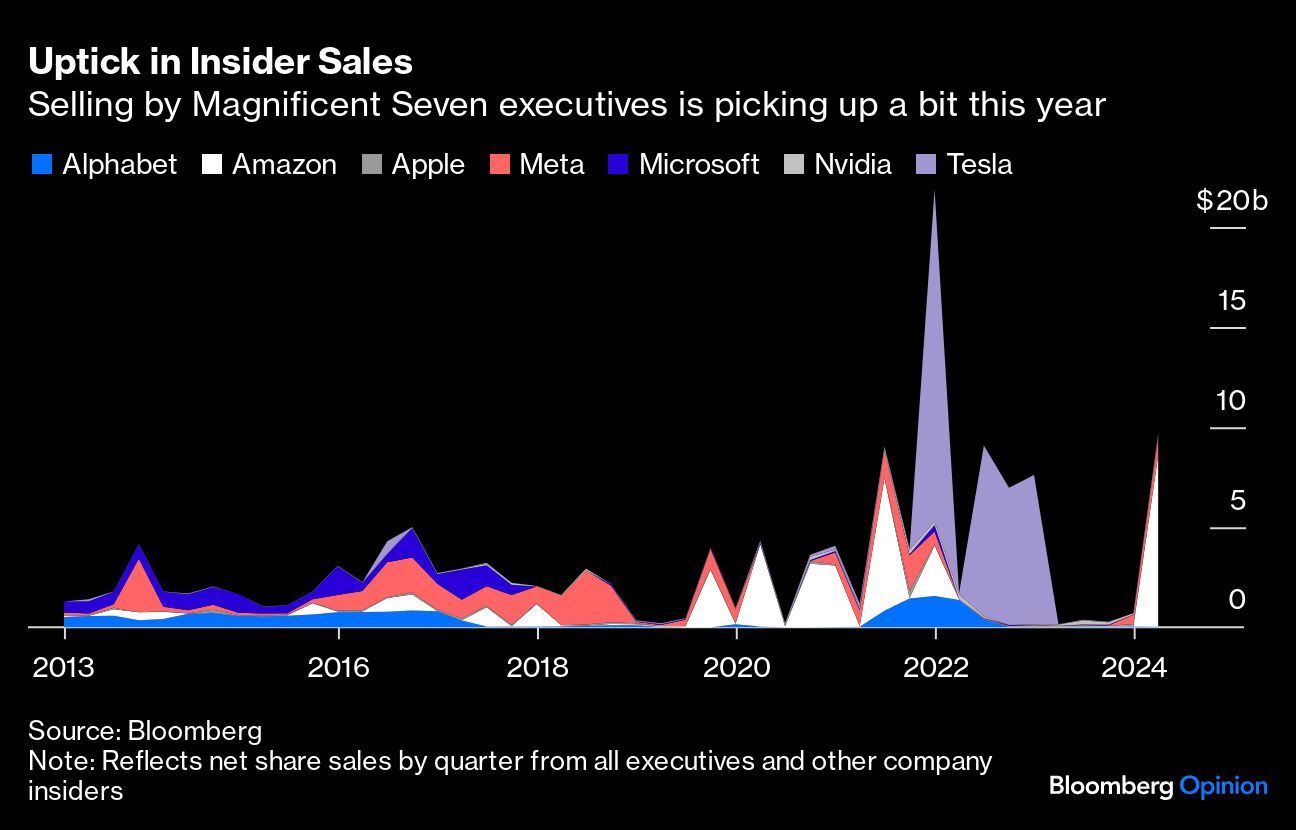

With the S&P 500 near all-time highs, insider share sales have picked up at top-performing companies. This quarter alone, Jeff Bezos sold about $9 billion in Amazon.com Inc. stock and Mark Zuckerberg’s net sales of Meta Platforms Inc. amounted to around $850 million. While some observers view these developments ominously, I see them as a sign of a healthy mid-cycle market with some room to run.

Let’s start with the big picture. Among the closely watched Magnificent Seven growth stocks, net sales by insiders are at their highest since late 2021. But many insiders stopped selling entirely from mid-2022 through late 2023, and it’s natural to expect some catch-up to address executives’ desire for liquidity and portfolio diversification.

Traders have tried to extract signals from insider transactions for decades. In theory, insiders know more about their businesses than the general investing public, and academics have found ample evidence that their unique insights help insiders to consistently beat the market.

While criminal insider trading looms largest in our collective imaginations (i.e. share sales by Enron Corp.’s Chief Executive Officer Jeffrey K. Skilling), insiders can also trade on squishier, not-quite-prosecutable foreknowledge (“business seems to be going pretty well and markets are assigning a low multiple to my stock, so I’ll opportunistically buy some more of it”). University of Michigan finance professor H. Nejat Seyhun has even made the case that regular investors can sometimes exploit the transactions for their own benefit.

In reality, public disclosures about insider activity are hardly a straightforward tell, and sales volumes are only foreboding if they’re extreme. In addition to not wanting to go to jail, most executives want to avoid even the perception of mistreating minority shareholders by selling their stock at market tops. Doing so can incur reputational damage that hurts their net wealth more in the long term.

Insider purchases may occasionally signal management confidence at times of weak market sentiment, but the informational value from insider sales is frequently confounded by other factors, including executives’ near-term needs for liquidity and portfolio diversification. Call me naive, but I tend to assume that normal insiders try to sell when their stocks are fairly valued — not overvalued.

Undoubtedly, there are always counterexamples that feed the belief that insider sales portend bubbles that are about to pop. In late 2021, Elon Musk started unloading Tesla Inc. shares at blatantly elevated prices (they had recently hit about $410, or 154 times forward earnings) to fund his acquisition of Twitter Inc. (now X). From the time Musk started selling to the market bottom a year later, the shares would see a maximum drawdown of about 74%. Of course, what’s often left out of the story is that Musk kept selling even as shares fell, leaving his weighted-average sales price from 2021-2022 at about $276 a share (still above current market prices, but not obnoxiously so.)

These days, it’s Bezos and Zuckerberg driving the insider sales volumes. I’m not here to convince you that Bezos and Zuck have better moral compasses than Musk — by all means, debate amongst yourselves! — but most of us can at least agree that they take a more conventional approach to their roles as founder-shareholders, which means they’re strongly disinclined to pick the top for their stock sales.

Bezos, 60, has been buying up real estate in his new home of South Florida, which conveniently has no state capital gains tax. Zuckerberg, 39, has been selling Meta stock to fund philanthropy. They don’t want to sell too low, but they probably don’t want to be perceived as pulling a Musk-like move.

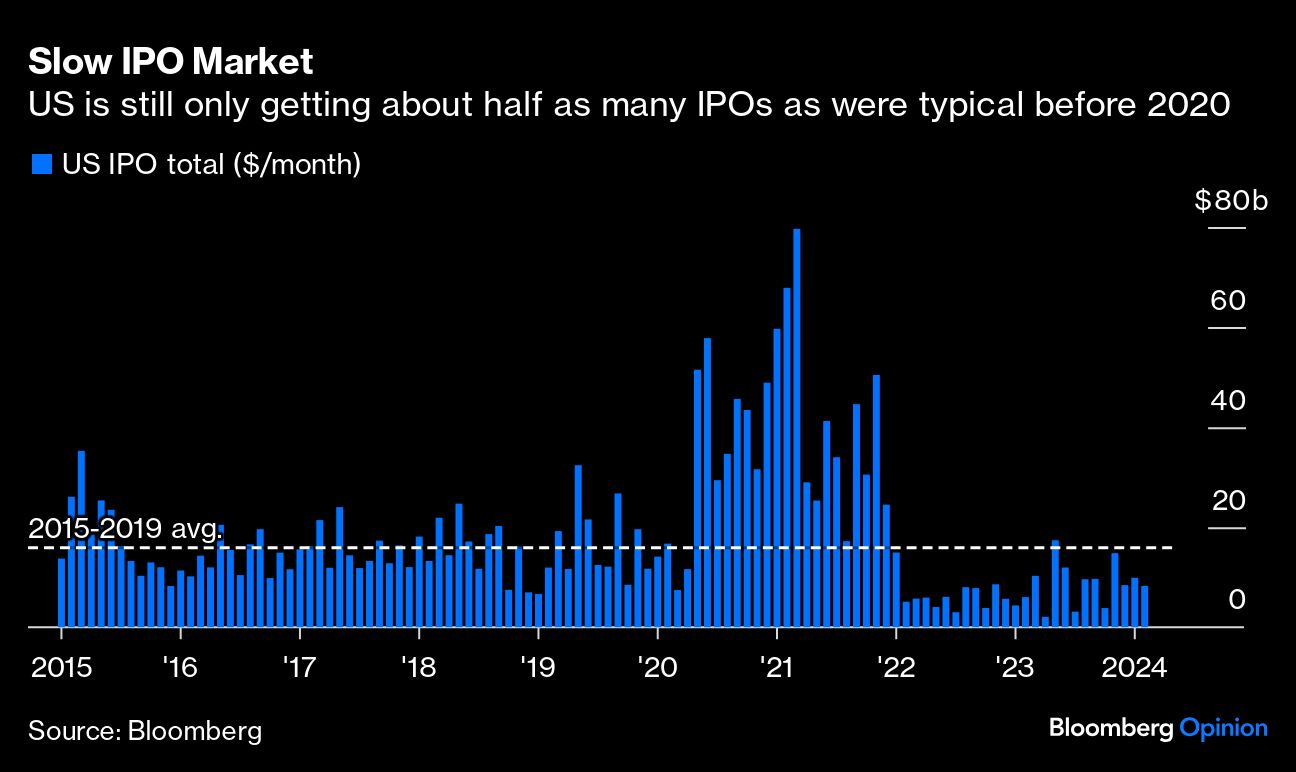

Today, there’s another notable difference from the 2021 market (and the Tesla episode): the lack of initial public offerings. When a market is truly getting overheated, you often know it because the supply of IPOs surges, as was the case in the late 1990s and in 2021. But by deal value, the US is still only pricing about $8 billion a month in IPOs, around half of what was typical in the pre-pandemic period. There may be some reasons for the inactivity — including the hangover from all the offerings three years ago — but the anemic state of the IPO market generally hints that markets haven’t reached a full-scale speculative frenzy.

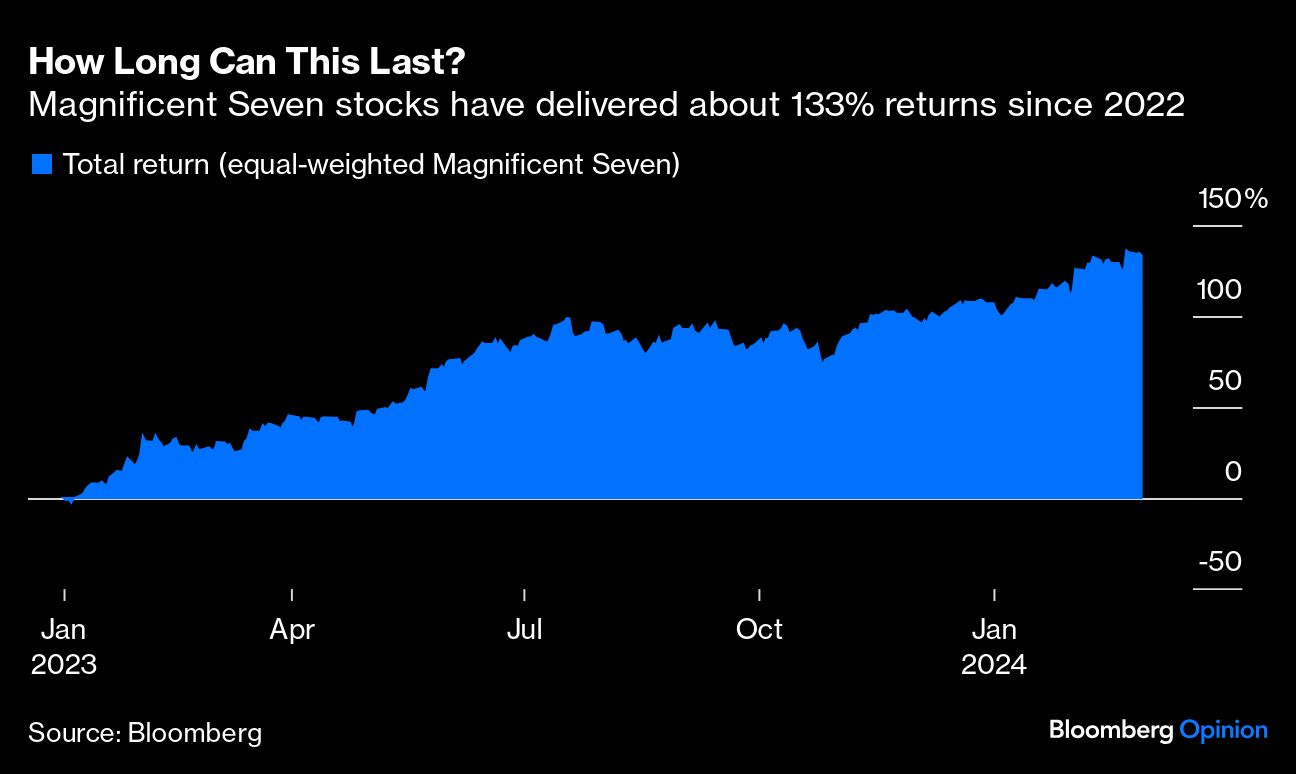

Clearly, I understand why market participants scrutinize insiders’ share sales with an extra measure of suspicion. The Magnificent Seven stocks have returned 133% since the end of 2022, and cautious investors may conclude that it’s time to follow Bezos and Zuck’s lead and take a few chips off the table. Fair enough. But stocks continue to benefit from the extraordinary resilience of US consumers; a rebound in companies’ spending on digital advertising; and investors’ desires to hold a call option on the extraordinary (but highly uncertain) potential of artificial intelligence. In that sense, the return of insider trading activity feels perfectly consistent with a market that still has something left in the tank — at least, it’s not the inherently scary omen that some doomers suspect it is.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin