Traders surprised by this year’s painful rise in bond yields are still looking to snap up US debt given their ongoing assumption the US economy will eventually slow in 2024.

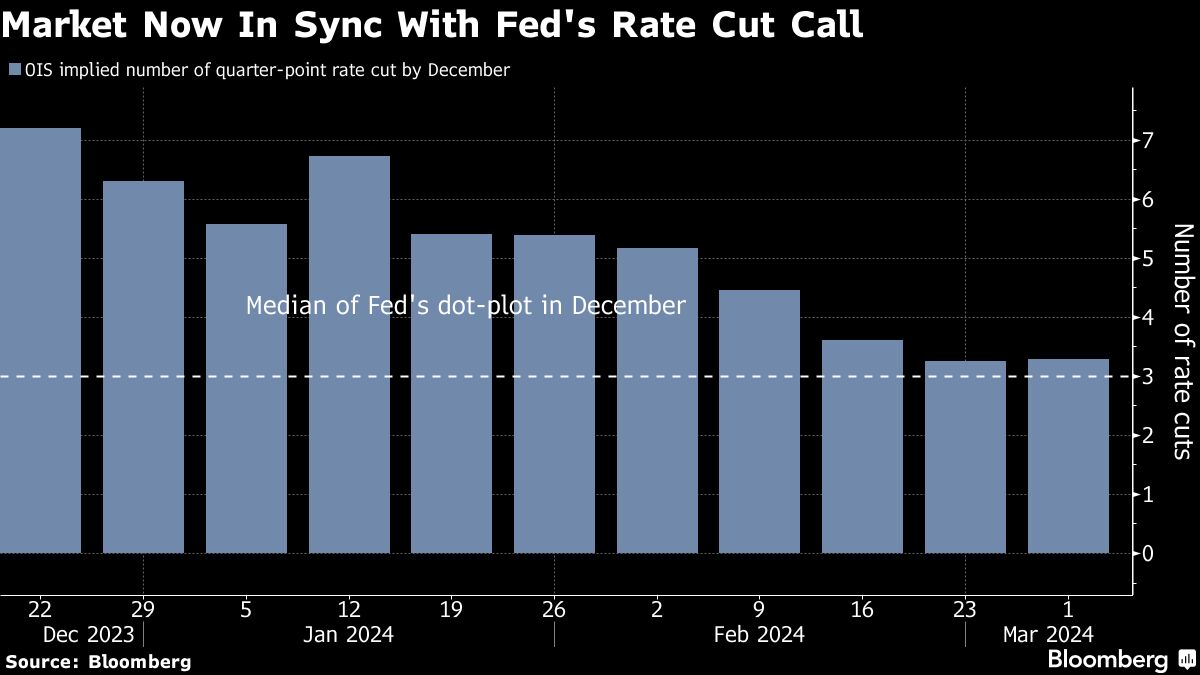

The economy has broadly outperformed forecasts at the start of 2024, prompting investors to drastically ratchet back wagers for Federal Reserve interest-rate cuts and imposing losses for the year on those who began the year favoring bonds.

It’s not the first time the economy’s resilience has caught traders wrong-footed. And for some, it’s a reason to surrender and accept the reality of higher-for-longer rates and the possibility of another run-up in yields — even to the highs of 5% reached last year.

But for those convinced the ultimate trajectory of rates is down, the time is getting ripe to dial up exposure to the world’s biggest bond market.

Managers at Pacific Investment Management Co., T.Rowe Price, DWS Investment Management Americas, and BNY Mellon Wealth Management are all in this camp. They see any further spikes in Treasury yields across the five- to 10-year sector toward 4.5% as a compelling purchasing opportunity.

With inflation having come down sharply from where it was when yields reached their peaks of last year, “4.5% is the new 5%” and a good place to buy, says Michael Cudzil, a portfolio manager at Pimco. “We are very much closer to adding back duration and getting overweight duration relative to our benchmarks.”

True, some investors have turned against the Treasury market amid firmer data releases of late. A Fidelity International money manager based in Singapore told Bloomberg News last month he had sold the vast majority of his holdings of US debt given expectations that the global economy keeps on ticking. A bond bear for much of last year, Katy Kaminski at AlphaSimplex Group was once again selling US government bonds after briefly turning bullish in January.

Capital Group also doesn’t rule out a test of 5% this year for Treasury yields should a hot economy erase market expectations of rate cuts, while Apollo Management Chief Economist Torsten Slok predicted on Friday that a re-accelerating US economy, coupled with a rise in underlying inflation, will keep Fed rate cuts off the table for all of 2024.

Last week, Treasury bonds ended on a positive note following softer-than-expected data on factory activity and a decline in consumer sentiment, which bolstered market expectations for three rate cuts this year, starting in June. The 10-year yield sank to 4.18%, the lowest in almost three weeks, though still well above where it started the year at 3.88%.

Coming up, a heavy week of data releases — capped by the monthly US employment report — will test the market, potentially giving traders new entry points. Also ahead, Fed chair Jerome Powell will deliver his semi-annual testimony to Congress on Wednesday and Thursday.

“If Powell says something to the effect that rate cuts will come in the second half of the year, then that can catalyze a move to pricing in two cuts,” said Steve Bartolini, portfolio manager at T. Rowe Price. “And if that is also met with continued employment strength, then that’s your scenario to get to 4.5% in the belly of the curve,” referring to five- and 10-year yields.

The array of employment and inflation figures set to land before the central bank’s policy meeting later this month may give bond investors plenty of opportunity to take advantage of any yield spikes.

Even at current levels, the Treasury market is “more fairly valued the further you go out on the curve,” as it’s now “closer to the Fed’s policy outlook for this year,” said George Catrambone, head of fixed income at DWS.

Catrambone favors intermediate Treasury maturities, particularly as the latest rise in five- and 10-year yields has left them comfortably above the long term market estimate of 3.5% — flagged by forward rates — for the end destination of the Fed’s next easing cycle.

While the Fed’s preferred gauge of inflation slowed to an expected 2.4% in January as reported last week, central bank officials want to see this measure get back to an average of 2%, and have indicated a reluctance to move on rate cuts until they are sure inflation is under control.

At present, T. Rowe Price’s Bartolini is content to play a “waiting game” and remain “patient with adding to duration.” A rise beyond 4.4% in the belly would prompt them to buy and shift from their current underweight position. “The 4.4% area in the belly is more interesting as that will mean two cuts are priced in,” said Bartolini.

What Bloomberg Intelligence Says ...

“Rate-market pricing for year-end 2024 outcomes may shift further toward no cuts if incoming data continues to come in strong. Though our base case scenario remains three nonconsecutive cuts starting before midyear, we’re less certain about such an outcome given recent data.”

— Ira F. Jersey and Will Hoffman, BI strategists

Such a shift would likely chip away at investors who are still sitting on some $6 trillion of money-market cash, giving them incentive to move into bonds.

“Fewer rate cuts are in our view a fresh opportunity for clients holding cash to get into bonds,” said Sinead Colton Grant, chief investment officer at BNY Mellon. “You’ll see volatility, but in and around this area is attractive, so yes, you might see yields a little bit higher than here, but they’re still pretty attractive at this level relative to where they’ve been over the previous 10 years.”

What to Watch

- Economic data:

- Mar. 5: S&P Global US Services and composite PMI; factory orders; ISM services index; durable goods orders; capital good orders

- Mar. 6: MBA mortgage applications; ADP employment; JOLTS job openings; wholesale inventories; Federal Reserve Beige Book;

- Mar. 7: Initial jobless claims; Challenger job cuts; trade balance; nonfarm productivity; unit labor costs; consumer credit; household change in net worth

- Mar. 8: US employment report including unemployment rate, average hourly earnings

- Fed calendar:

- Mar. 4: Philadelphia Fed President Patrick Harker

- Mar. 6: Fed chair Jerome Powell testifies before the House Financial Services Committee; San Francisco Fed President Mary Daly; Minneapolis Fed President Neel Kashkari

- Mar. 7: Powell testifies before the Senate Banking Committee; Cleveland Fed President Loretta Mester

- Mar. 8: New York Fed President John Williams

- Auction calendar:

- Mar. 4: 13-, 26-week bills

- Mar. 6: 17-week bills

- Mar. 7: 4-, 8-week bills

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Michael Mackenzie