A curious thing has happened in the US market discourse: In the absence of major concerns about jobs and growth, commentators have started to worry that the economy is too good to keep inflation contained. The most salient recent example is Apollo Global Management Inc. Chief Economist Torsten Slok, who said last week that economic strength will prevent the Federal Reserve from cutting policy rates in 2024.

I, for one, am extremely skeptical.

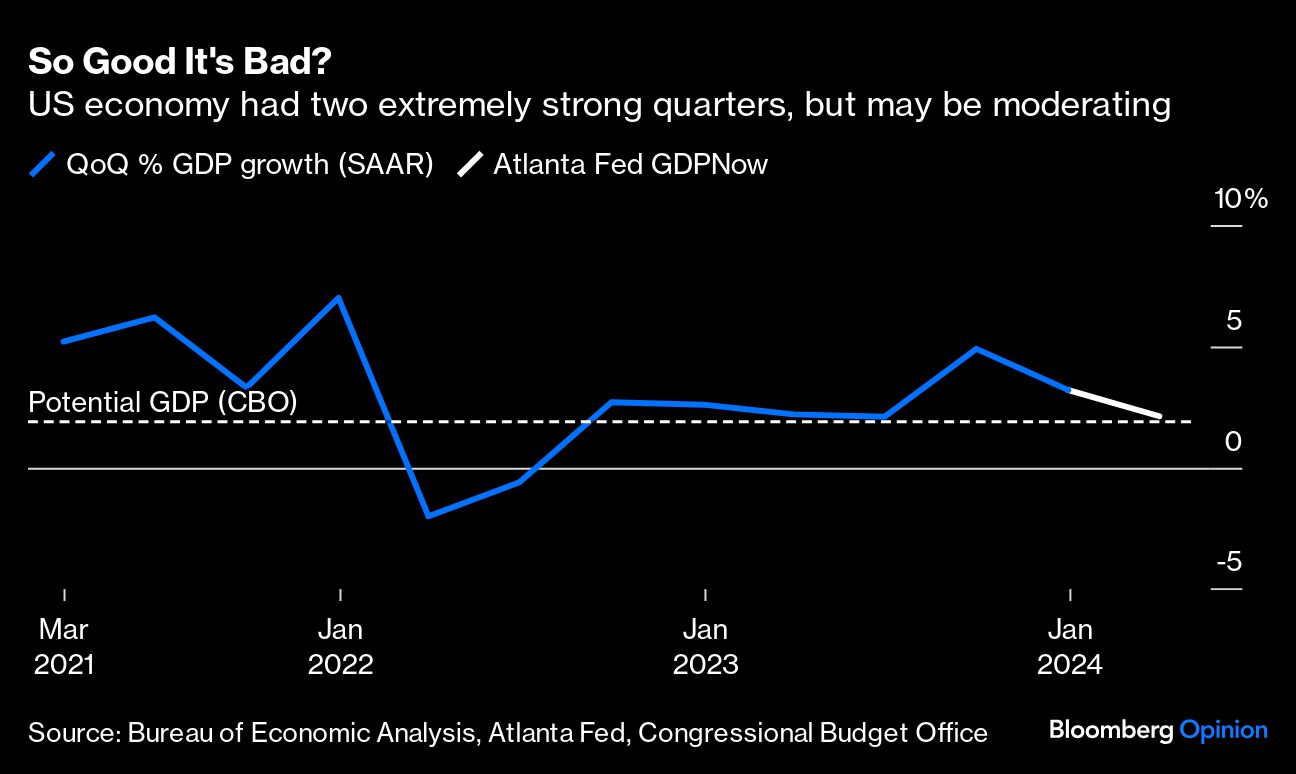

Consider recent trends. Although the US posted impressively strong growth in the second half of 2023, there are early signs of moderation in the first quarter of 2024. The Atlanta Fed’s GDPNow tracker has gross domestic product expanding at about 2.1% in the first quarter, close to the level that the Congressional Budget Office estimates as the economy’s potential (read: non-inflationary) growth rate. What’s more, there’s evidence from high-frequency retail sales data that real consumption may have weakened in February. Those data points serve to caution us against over-anchoring our views on the real economy to data that’s now several months old.

Second, there’s the inflation data itself, which is all that really matters for monetary policy so long as the labor market stays on track. The economy could be growing at 5% a year, but if it doesn’t cause inflation why should policymakers mess with success?

Much of the handwringing in markets came on the back of the surprise acceleration in the January core consumer price index, a development that I’ve written about at length (including here and here) in recent weeks. At the risk of sounding like a broken record, that data may well have been influenced by a “January effect” (firms sometimes use the start of a calendar year to raise prices to an extent that isn’t always captured in the seasonal adjustment process). Even more importantly, it was distorted by some extremely quirky housing data.

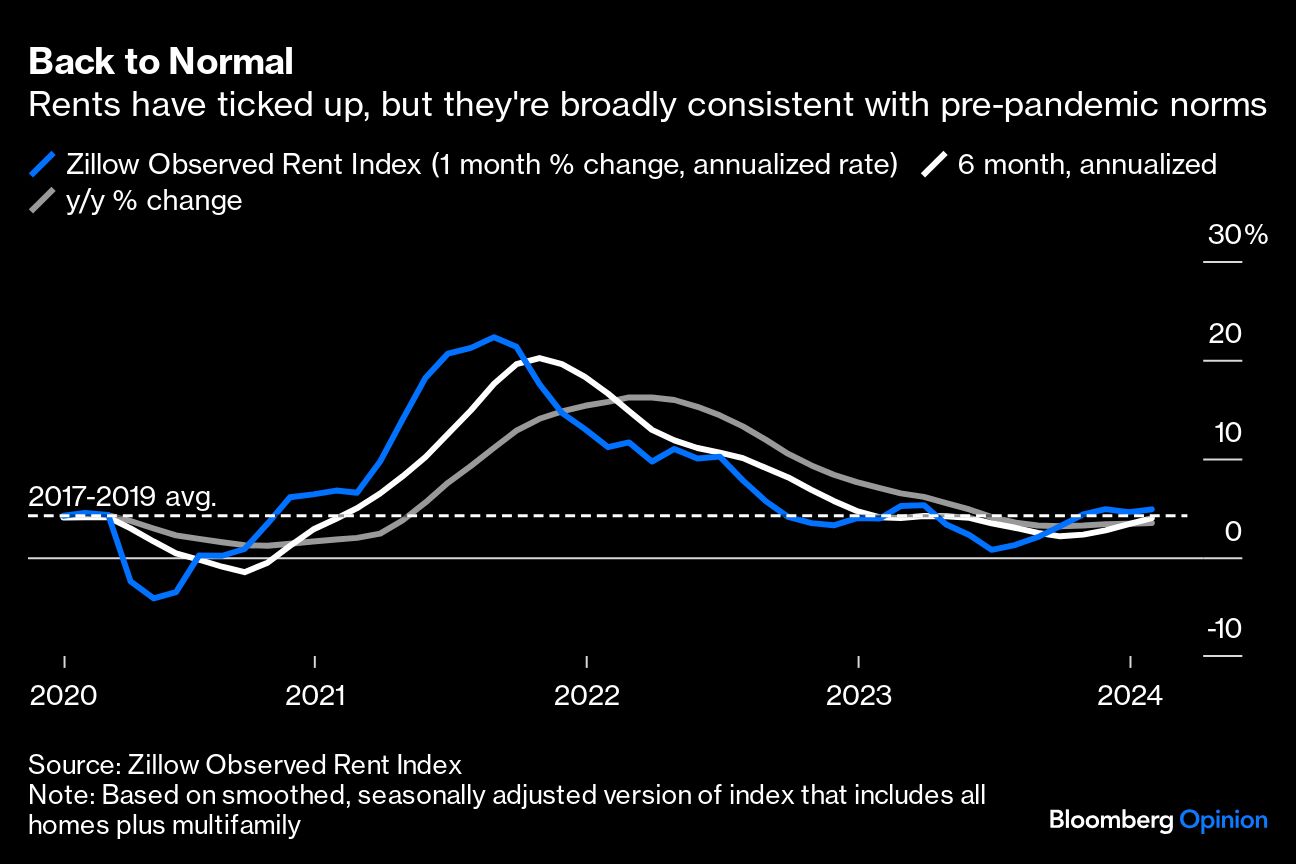

That brings me to the last point: rent. Market rents, which feed into reported housing inflation with a long lag, have shown some signs of ticking up at the start of the year1. Since housing has an outsize weighting in the CPI and personal consumption expenditures, or PCE, inflation baskets, this behavior has fueled concern that it may prove difficult to get the measure back to a level consistent with the Fed’s inflation target. I doubt it. As a general rule, rents in the US have been consistently decelerating for years (and even falling outright in some data sources), presaging more modest CPI housing inflation in the quarters ahead. These averages have been volatile in the post-pandemic era amid shifts in geographic and housing-type preferences, and a few month-to-month wiggles in the data are nothing to fear.

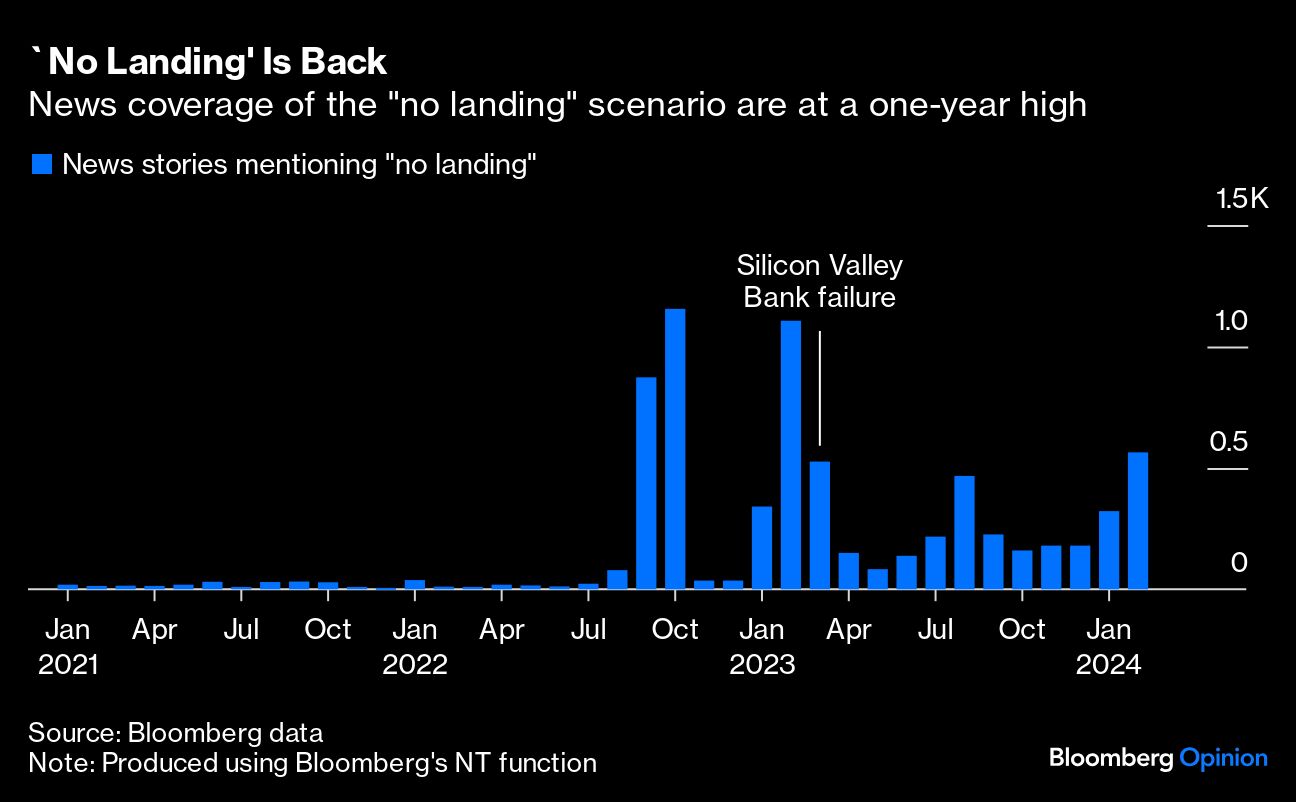

This isn’t the first time that a version of the “no landing” thesis has captured the imagination of Wall Street. The last time it garnered this much attention was in early 2023, but those concerns were promptly extinguished by the Silicon Valley Bank fiasco that March. The pattern would suggest that “no landing” tends to emerge from time to time to fill the narrative void left by a lack of recession concerns.

Of course, it’s foolhardy to ignore this tail risk entirely. Even if the odds of a true no landing remain low, market narratives can occasionally become so pervasive that they have a material impact on asset prices, even if nothing ultimately changes.

Evidence of that was on display in August and September, when investor Bill Ackman promoted the thesis that rising global conflict could mean the end of globalization as we know it and, ultimately, lead to structurally higher inflation. There’s no empirical evidence that take was right, but he still made money betting yields would go up. In the short-run, the market is a momentum-driven animal, and sometimes a good story is all it takes to trigger a big move.

In reality, the economic outlook feels somewhat benign, as many Fed policymakers have been anticipating. Back in December, the median participant in the central bank’s Summary of Economic Projections forecast three rate cuts in 2024, and markets priced in twice that many. Now, as talk of no landing picks up steam again, futures markets have moved to price in exactly three rate cuts, and the consensus feels like it’s on the money.

Growth is strong (not too strong); inflation is moderating; and recent comments from Fed leadership suggest that the data-dependent central bank will have enough evidence to start lowering policy rates by mid-summer. Some folks are likely to keep pushing the no-landing scenario for a while longer — at least until the inflation data gives us incontrovertible evidence to the contrary, or we find a new tail risk to worry about.

1Here, I'm using Zillow data, and the evidence varies a bit from provider to provider.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.