Ever since the Federal Reserve began its policy-tightening campaign, Jerome Powell has been happy to ignore one form of inflation: Rising asset prices.

Now as the Fed chair gears up for his congressional testimony on Capitol Hill, Wall Street is starting to wonder just how long Powell’s hands-off approach can last against the backdrop of sizzling markets.

With tech stocks hitting relentless records of late, a Goldman Sachs Group Inc. measure of financial conditions has eased at one of the fastest clips in four decades. Ever-volatile Bitcoin touched new heights at one point Tuesday as the meme-coin crowd roars back to life. On economic growth, even Nouriel “Dr. Doom” Roubini is sounding, well, bullish.

All that has a cohort of market participants on the lookout for signs that the cross-asset rally is making life harder for the Fed chief who’s on a legacy-defining mission to ease monetary policy in the months ahead — without undermining progress on inflation.

“The Fed has to watch financial conditions closely and it is a delicate dance for Powell,” said Priya Misra, portfolio manager at JPMorgan Asset Management. “Too much easing — because the market expects the Fed to cut too aggressively — and then the Fed will push back since they want to make sure that inflation is under control.”

An uneasy truce has prevailed between the Fed chair and markets, with Powell staying mum as more than $8 trillion was added to the S&P 500 since the end of October. It all worked, the thinking goes, to the central bank’s advantage, preserving wealth among affluent consumers that helped cushion the impact of 11 interest-rate hikes on mortgages and other debt-servicing obligations.

“Equities are at all-time highs and credit spreads remain tight, not to mention the fact that we just saw record investment-grade bond issuance to start the year,” said Adam Phillips, managing director of portfolio strategy at EP Wealth Advisors. “These conditions suggest financial conditions remain accommodative enough to buy the Fed some time as policymakers consider eventual easing.”

Add inflation-adjusted interest rates rising to elevated levels just as bank-lending standards have tightened, and a case can be made — one that Powell has previously nurtured — that market conditions are, in fact, consistent with the Fed’s goal of ease excessing in the business cycle.

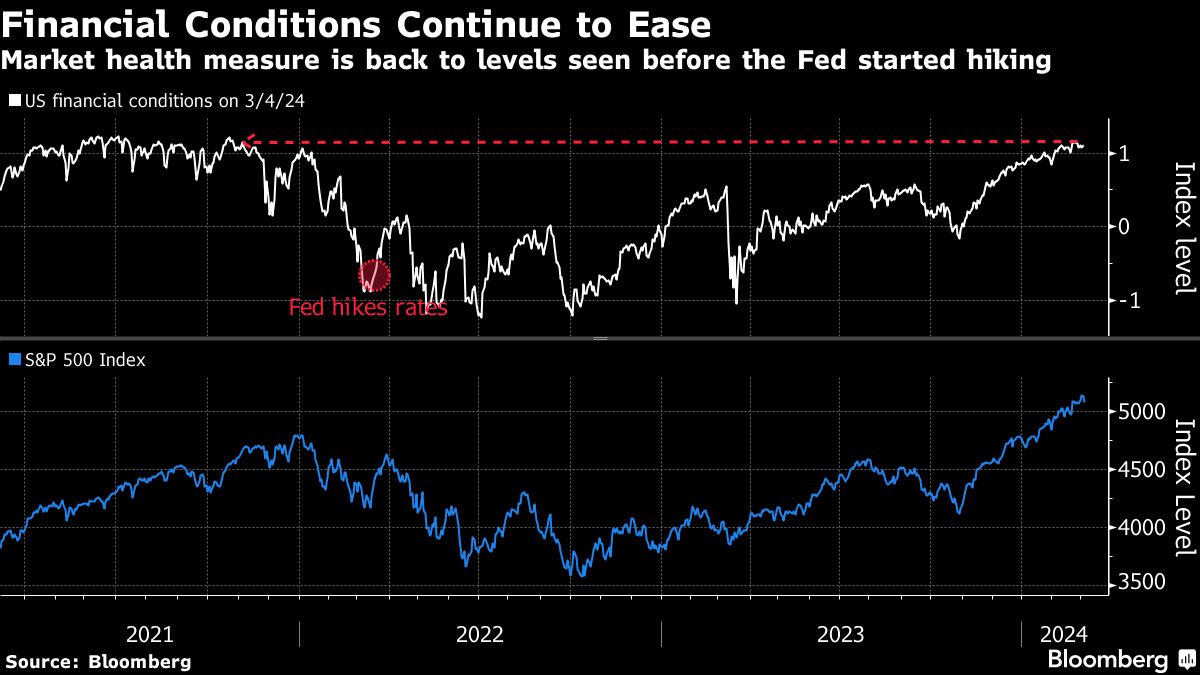

Yet some Wall Street worrywarts see signs of trouble brewing ahead. A Bloomberg measure of US financial conditions has already returned to accommodative levels seen before the Fed started raising rates. A similar Goldman metric shows that the cumulative easing across assets over the past four months is one of the biggest since at least 1982, according to Bespoke Investment Group LLC.

Against this backdrop, Federal Reserve Bank of Atlanta President Raphael Bostic this week warned that “pent-up exuberance” — with businesses dialing up spending and investment — complicates the outlook for monetary easing ahead.

“If we see equity markets continue to rise and approach valuations last seen in late 2021, on the margin you would think the Fed has fewer reasons to ease,” said Michael Bailey, director of research at FBB Capital Partners. “The Fed is evaluating these easing factors in the context of tightening elsewhere in the economy.”

At the January gathering before the latest advance in markets, Fed officials remained more worried about the risk of cutting rates too soon than keeping them high for too long, while noting a scenario where easy financial conditions contribute to the inflation outlook. Still policymakers were broadly sanguine, citing large-cap tech companies as the proximate cause for the rally in broad equity indexes, while overall market valuations “were more subdued.”

Of course, it may not matter much just how the central bank frames the run-up in risky assets against its monetary agenda. The economy remains strong and corporate earnings have marched higher, extending rallies that began when all manner of interest rates were appreciably higher. Money has flowed to stocks and crypto almost without regard to central bank policy, sucked in as the threat of a recession eased.

And many on Wall Street dismiss any argument that the Fed cares about market exuberance — as long as it doesn’t whip up inflation pressure. Historical evidence that rate cuts cause bubbles is notably mixed. While some see the easy policies of the early 2000s as setting the stage for the financial crisis, the late-1990s dot-com bubble coincided with a period when rates were higher than they are currently.

“If you have financial exuberance, but both the unemployment rate and inflation is low, then the Fed will act in the way it sees best to maintain full employment and price stability,” said Jim Caron, co-chief investment officer at Morgan Stanley Investment Management. “Asset prices reflect feedback to their policy decisions. But it does not govern it.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More Large Cap Growth Topics >