All the fearmongering in Washington over the $1.5 trillion federal budget deficit hides a truth few politicians would admit — that hefty headline number you hear so much about is an unreliable measure of US fiscal health.

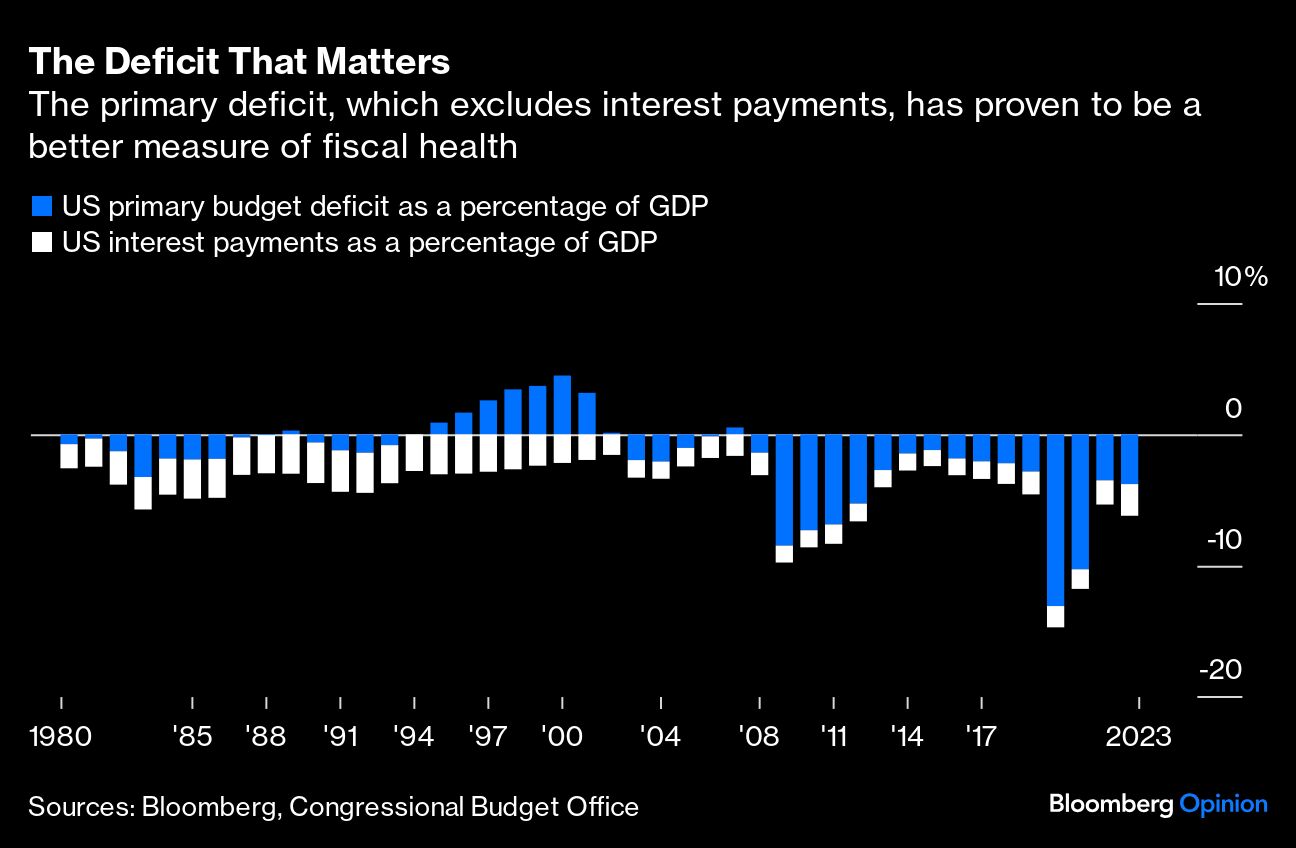

Savvy economists prefer what’s known as the primary deficit, which is the overall shortfall minus what the government spends each year on interest payments. At $637 billion, this measure is smaller, less frightening, in line with recent history and — more importantly — shrinking, having narrowed from $1 trillion in 2023.

It’s a shame that lawmakers don’t focus their attention on the primary deficit, using that measure to help bridge the political divide and forging bipartisan solutions that will put the government on a fiscally sound and sustainable path. Instead, they bicker over less-than-meaningful numbers that threaten the US’s “ exorbitant privilege” in the global financial system by way of government shutdowns and reckless talk of not raising America’s borrowing capacity — a move that would risk a catastrophic default.

Why does it make economic sense to focus on the primary deficit, which ignores federal interest payments? The answer is because tax revenue and interest rates can diverge - often with unexpected results. For example, a booming economy will increase tax revenue but also push up borrowing costs; a slowing economy would have the opposite effect on rates.

Think back to the early 1980s, when the budget and primary deficits were a similar percentage of gross domestic product as today and concern about the nation’s fiscal situation was also elevated. In 1983, the primary and headline deficits were 3.3% and 5.7% of GDP, compared with 3.8% and 5.4% currently. And like now, the US was also emerging from a painful recession, during which GDP contracted faster and deeper than any time since the Great Depression only to begin a strong recovery that lasted six years, increasing government revenue. As a result, that primary deficit of 3.3% in 1983 became a primary surplus of 0.3% by 1989.

Total debt as a percentage of GDP was little changed, however, going from 38.9% of GDP to 38.5% as the rapidly growing economy kept interest rates relatively high. Federal interest payments grew as a percentage of the economy from 2.5% of GDP in 1983 to 3% in 1989. As a result, the headline deficit in 1989 was 2.7% of GDP, much higher than the post-war average of 1.2% of GDP at the time. If you had judged the country’s fiscal health based on the headline deficit alone, you would have thought the US went from the worst shape since WWII in 1983 to merely bad shape in 1989. In fact, America’s fiscal health had stabilized, debt was no longer growing as a percentage of GDP and the stage had been set for the massive surpluses of the 1990s.

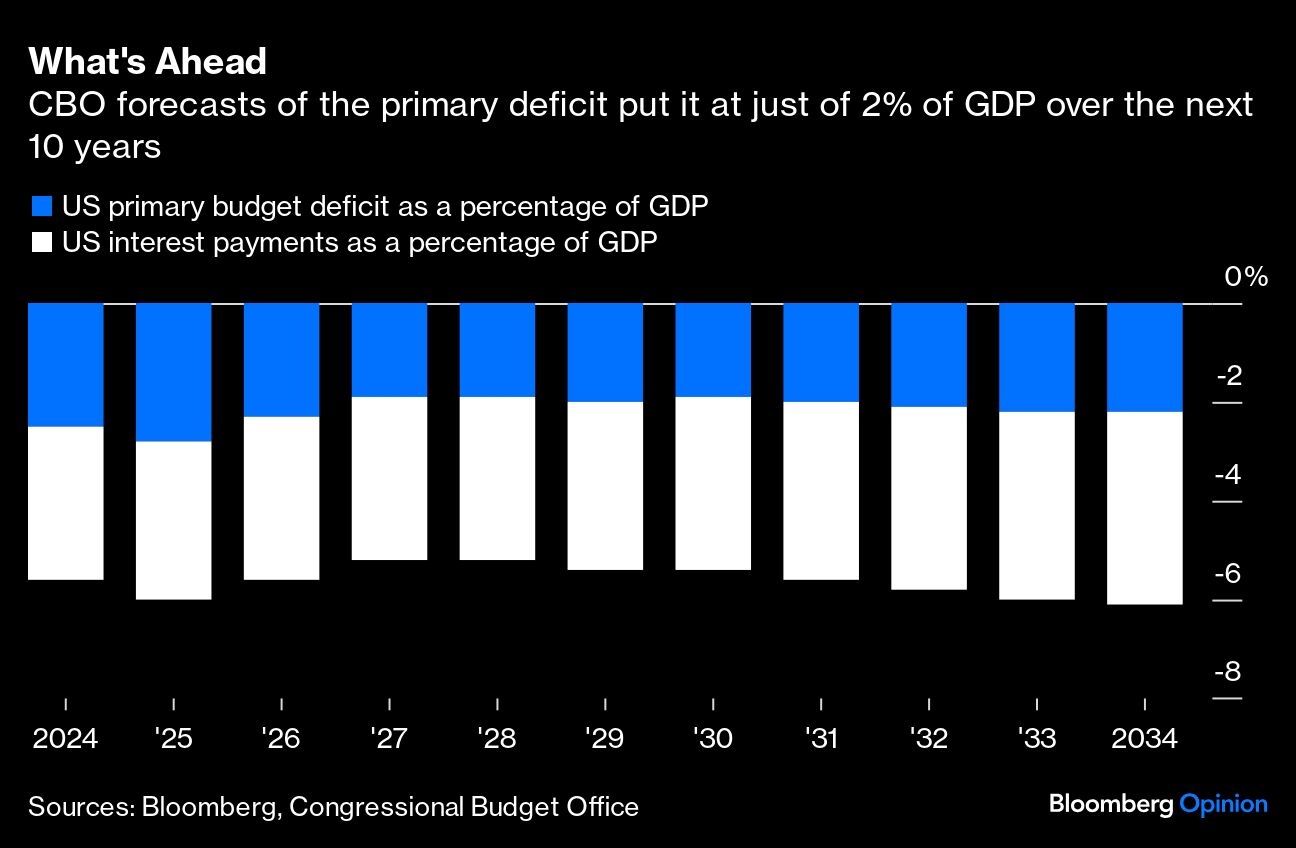

Just as the primary deficit -- or more accurately surplus -- would have been a much more accurate indicator of America’s fiscal health in 1989, so too is it likely a more accurate measure of US fiscal health today. The bipartisan Congressional Budget Office projects that the primary deficit will come in at 2.3% of GDP this year and shrink to 2.1% by 2034 – which is a very manageable figure from a debt management perspective. As for the headline deficit, the CBO projects that to be 5.3% of GDP this year, expanding to 6.2% by 2034.

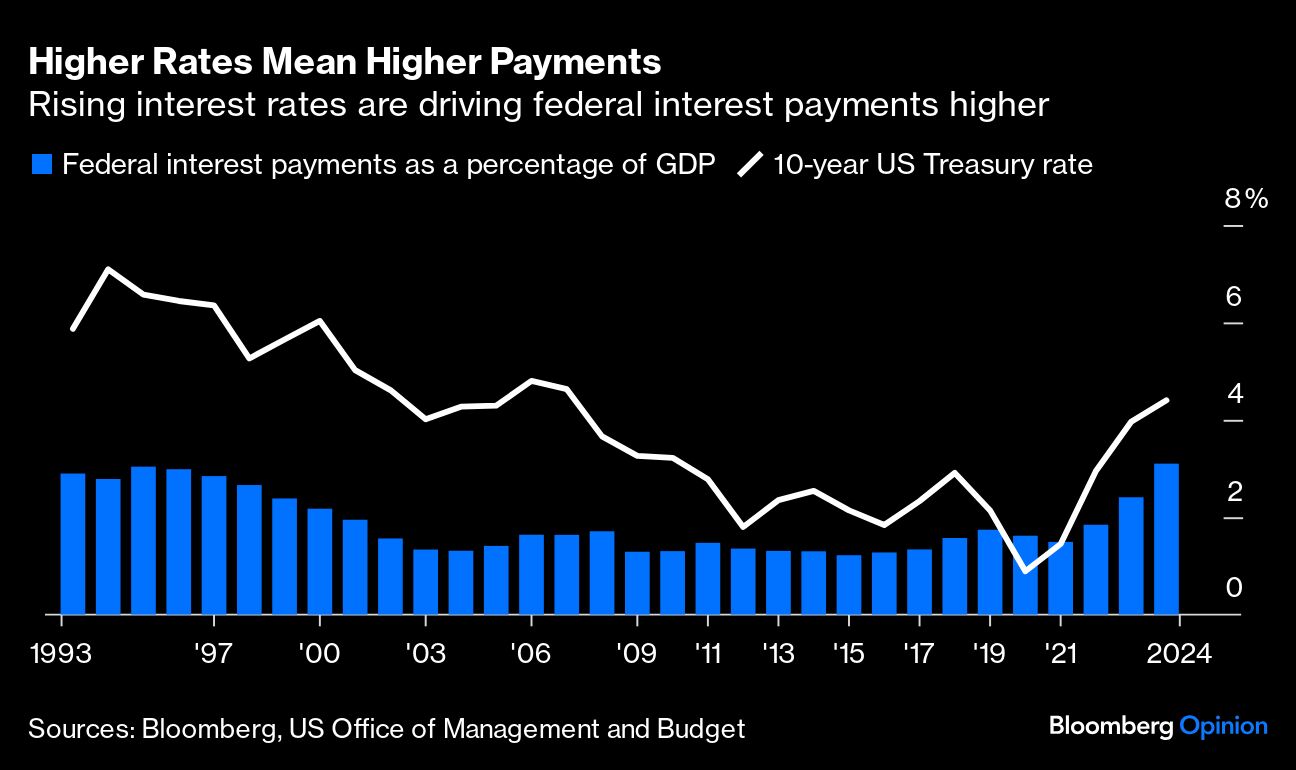

Just like in the 1980s, the headline deficit may prove to be an unreliable indicator. The economy has rebounded strongly following the early days of the pandemic, driving up borrowing costs and federal interest payments. Rising interest expenses rather than increases in government spending are mostly why the headline deficit is wider today than in 2019.

This is not to say that rising federal interest payments aren’t a burden on government finances, and at 2.8% of GDP they are closing in on their peak of 3% in 1995. The upside is that indicators of the US’s ability to pay its $34 trillion of debt debts, such as robust demand for Treasury securities by foreign investors and a strong and stable dollar, suggest that America’s creditors are not worried. Moreover, the CBO is bad at forecasting interest rates. Over the last 40 years, interest payments have been half of what it forecasted on average. That suggests their current projection of interest payments is likely overly pessimistic.

Lawmakers should look to the primary deficit to gauge the nation’s fiscal health. This measure indicates that while not perfect, the US’s fiscal health is better than before the pandemic. What’s more the economy has grown faster than most forecasts. If the trend continues, then even the modest primary deficits the CBO is forecasting may be an overstatement. The US could be on the cusp of a repeat of the 1980s when rapidly growing revenues brought the primary deficit swiftly into balance.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.