How bad is 2024 going so far for Tesla Inc.? Well, its stock is down more than Boeing Co., making it the worst performer in the S&P 500 Index. We are two weeks or so from the end of the first quarter and while the doors aren’t popping off Tesla vehicles, there is a distinct wobble in the (metaphorical) wheels.

Electric vehicle sales, while still growing at a healthy clip, are slowing both in the US and worldwide. In China, the largest EV market in the world, Tesla’s sales were up across the first two months of the year — but in a cutthroat market where homegrown rival BYD Co. Ltd. now sells a model priced for less than $10,000. Moreover, sales from Tesla’s Shanghai factory overall, including exports, were down 6%, year over year, suggesting sluggish demand in other overseas markets. A temporary shutdown of Tesla’s factory near Berlin due to a possibly arson-related power cut hasn’t helped either. Meanwhile, keeping up with Chief Executive Elon Musk’s outrageous posts on his social media platform, X, has emerged as the world’s worst full-time job; a growing distraction for him and a potential deterrent to customers.

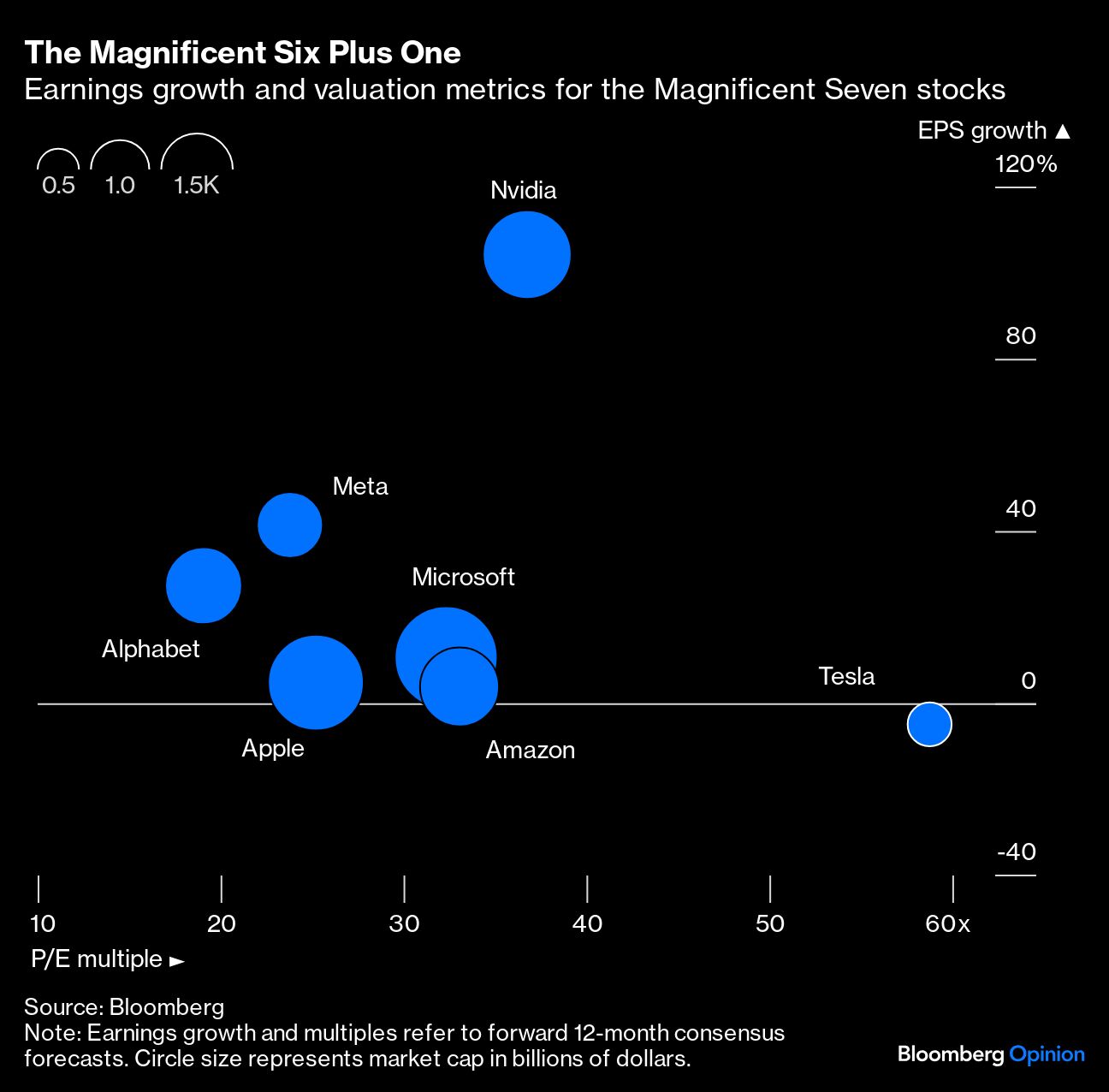

Tesla ditched its annual growth target of 50% in January, which is problematic when the bull case centers on the company taking over the world. Having been touted as a member of the so-called Magnificent Seven, a handful of stocks responsible for leading the S&P 500 to record highs, the carmaker is now clearly an outlier in the worst way. Despite being the worst performer this year, and the only one forecast to see earnings shrink over the next 12 months, it is the most expensive of the bunch by far.

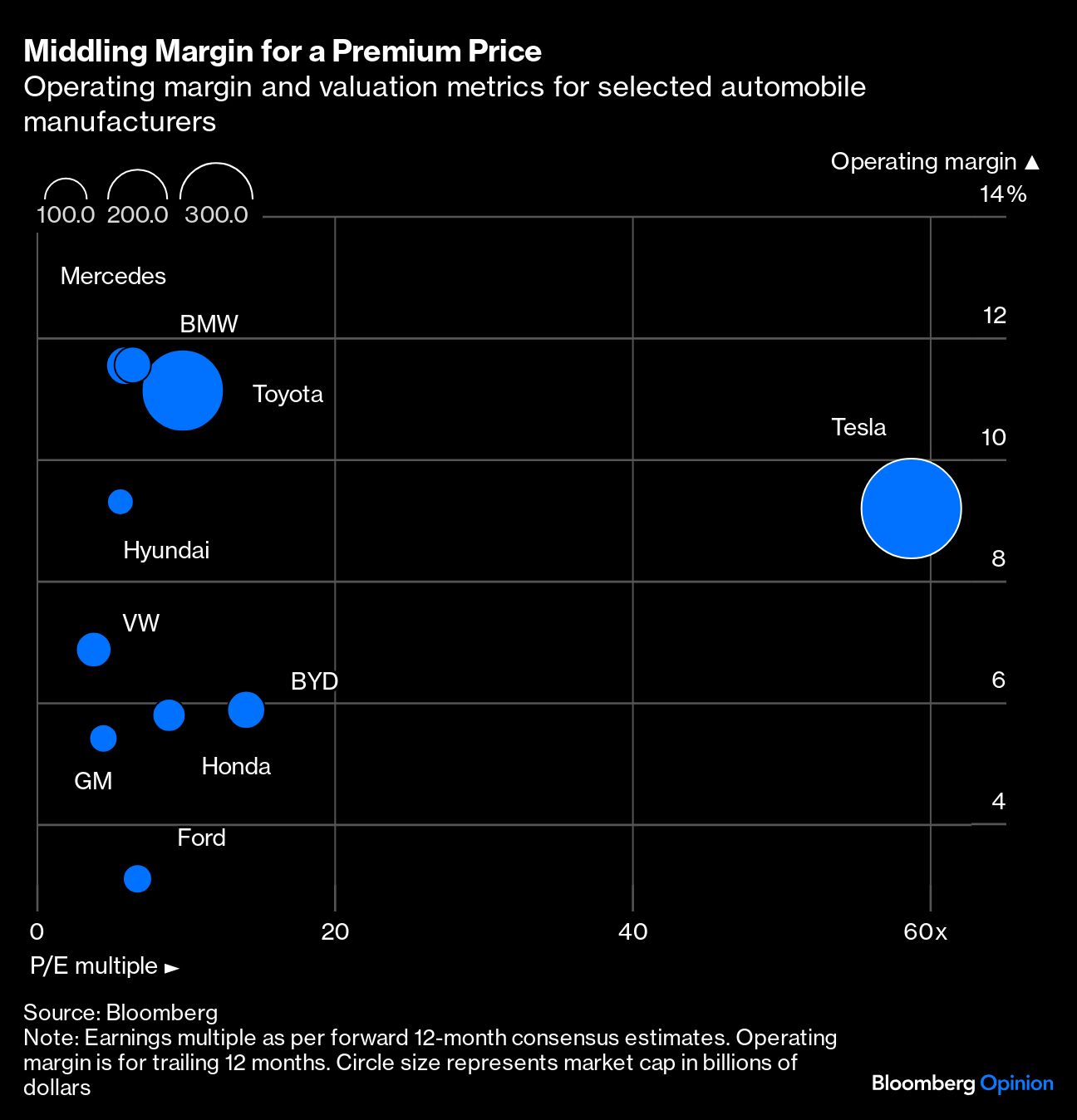

Making the likes of Nvidia Corp. look cheap is a perverse sort of achievement, I suppose. Doing so with legacy automakers is, in contrast, a doddle. Despite dropping, Tesla’s market cap is still roughly the same as that of Toyota Motor Corp., Mercedes-Benz Group AG and BMW AG combined. Besides its growth potential — now somewhat clouded — Tesla’s high profit margins were touted as justification for this. After a year or so of an EV price war, though, these also look middle-of-the-road.

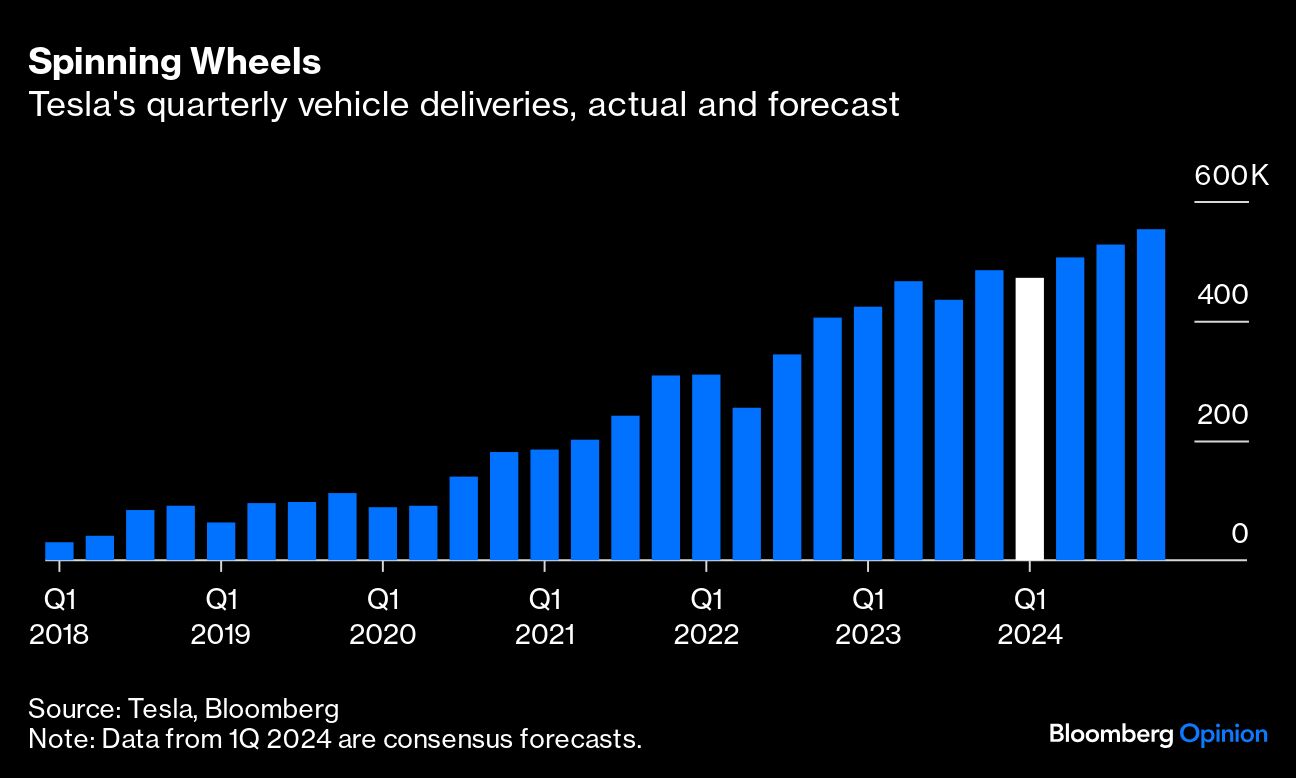

Tesla’s growth has slowed despite more than a year of successive price cuts. Analysts forecast vehicle deliveries to have fallen this quarter compared with the prior one and to have risen only 11% compared with a year ago. While they do expect quarterly deliveries to crack the half-a-million level from the second quarter on, this would still imply annual growth of just 14%. On Wednesday, Wells Fargo analyst Colin Langan was more bearish, predicting no growth in sales volumes this year and a drop in 2025.

The message from Tesla’s two big markets, China and the US, is that cheaper EVs are needed to unlock a wider pool of buyers. Tesla is expected to launch a sub-$30,000 car, dubbed the Model 2, sometime in the next couple of years. This is no small challenge: The average manufacturing cost of the vehicles Tesla sold in 2023, excluding leases and emissions credits, was almost $38,000.

Yet Tesla chose to first launch the Cybertruck, which certainly has plenty of mass but, starting this year at about $80,000 and seemingly targeted at cubism-loving survivalists, less market. Rival Rivian Automotive Inc. this month revealed its R2 SUV — expected to start at about $45,000 — as well as teasing an even cheaper prototype R3 crossover. To be clear, Rivian lost more than $100,000 at the operating line on each vehicle it sold last year, so I am by no means declaring it to be Musk’s nemesis. Rather, it underlines the time that Tesla has lost. If quarterly sales figures due in early April indicate a slow pick-up in Cybertruck sales, this would compound the pressure on Tesla’s growth and margins.

Against all this, Tesla avers that it is merely between two waves of growth, with the arrival of a cheaper model inevitably spurring the next upswing. History is on the company’s side to a degree, since Tesla launches have tended to spur an expansion in the EV market overall, in the US at least. Yet times have changed. Tesla faces increasing competition in the US now and already intense competition elsewhere, especially in China.

A Tesla bull might say that once the near-term weakness dissipates, the longer-term thesis of Tesla dominating EVs (and artificial intelligence etc.) will reassert itself. But that would ignore the glaring message of the two charts above comparing Tesla to the Magnificent Six and its fellow automakers: The longer-term thesis never truly went away. At almost 60 times forward earnings, Tesla is still priced for that halcyon future where it outdoes both the AI giants and the global autos industry. An un-magnificent quarter, as this one is shaping up to be, might yet force a rethink.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.