The timing and pace of Federal Reserve interest rate cuts will consume economists and market commentators for months to come. But an emerging story in 2024 is that lenders and borrowers are jumping the gun well in advance of any policy easing.

There’s been a noticeable bounce in transactions this quarter after a period of tightening credit and subdued lending that was brought on by 2023’s regional bank meltdown and concerns about new capital rules. There are a couple of implications to this reversal: First, unlike after the Global Financial Crisis, the rate-cutting cycle, which the Fed says should start this year, will probably pack an outsized economic punch. And second, an economic growth stumble shouldn’t be seen as increasing the risk of recession but rather as a catalyst to shift activity from hot industries such as artificial intelligence to more credit-sensitive ones such as housing.

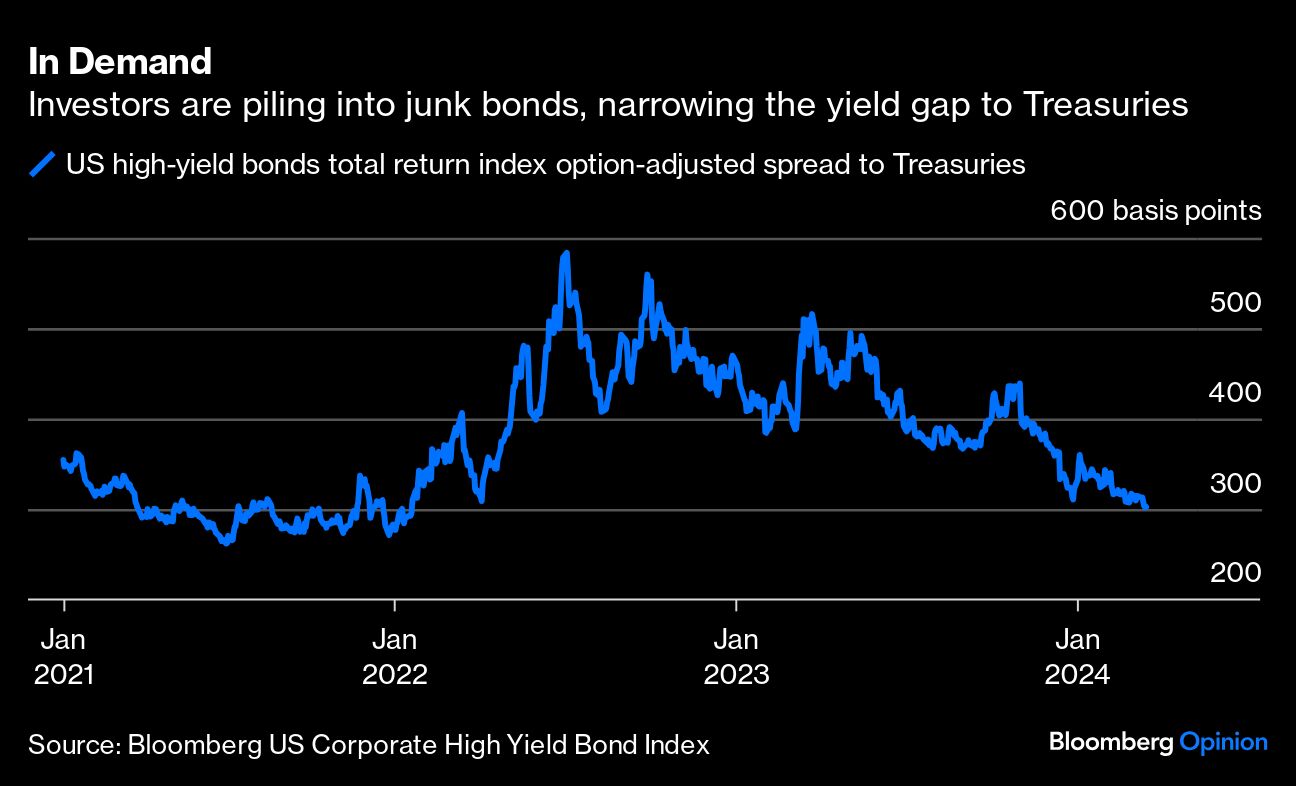

This bullish dynamic has been at work in corporate credit markets. Highly rated US companies are approaching a first-quarter record for debt sales, while the yield premium demanded from junk-rated issuers has narrowed sharply, reflecting a risk-on environment where investors worry less about recession and defaults and, instead, look forward to Fed easing.

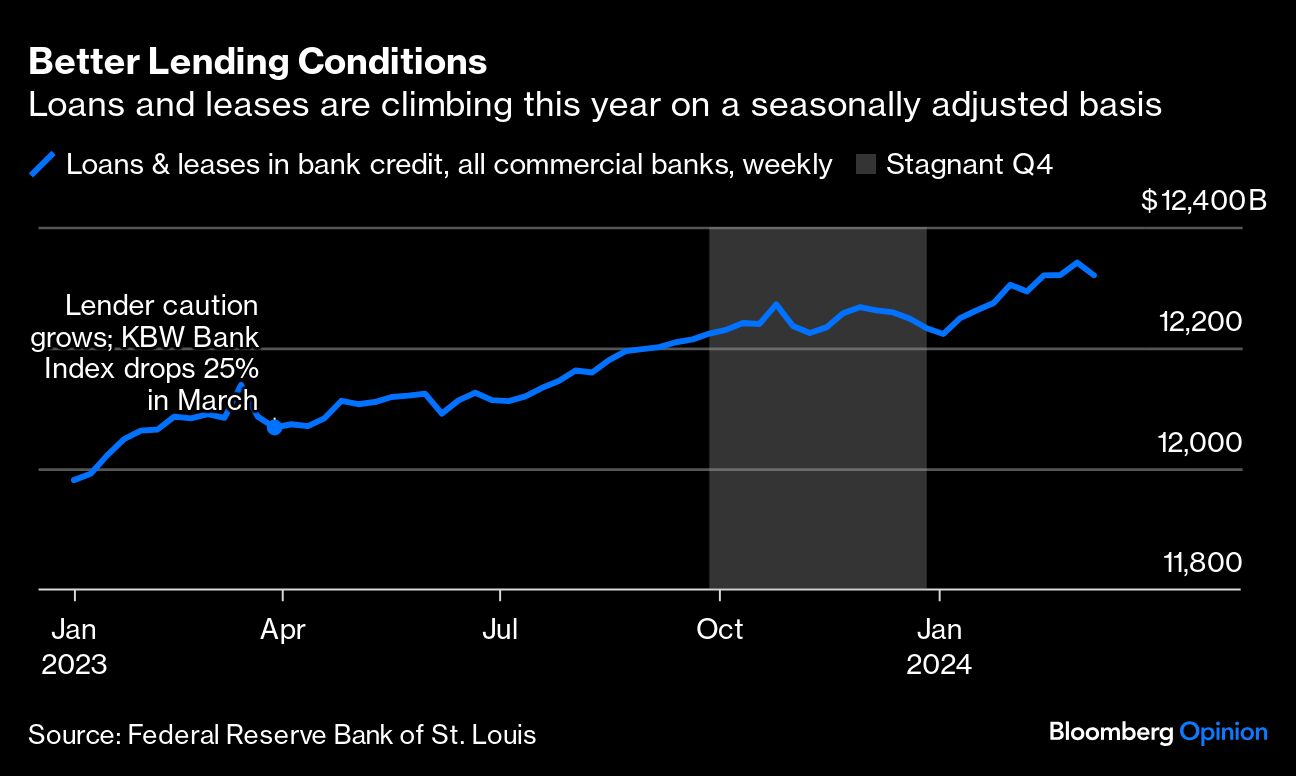

Weekly commercial banking data show loans and leases growing at a 4.7% annualized rate so far this year following a fourth quarter where uptake was essentially flat.

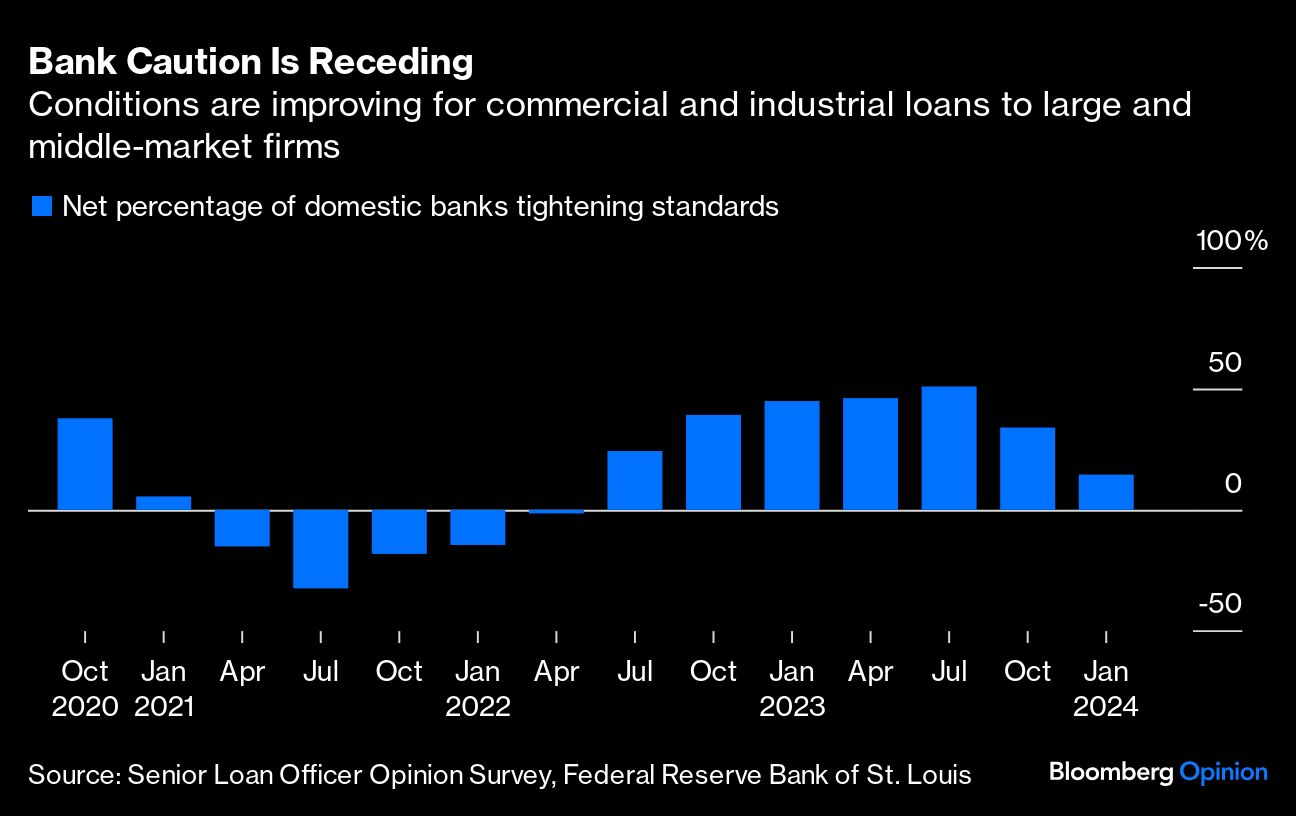

The Fed’s quarterly Senior Loan Officer Opinion Survey released last month was also less concerning than before. While domestic banks, on balance, still reported tightening standards for commercial and industrial loans, far fewer banks are tightening than in the aftermath of last year’s regional banking stress. If the trend continues, we could be looking at a net loosening of lending standards by the second half of this year with or without a move from the Fed.

One thing that caused banks to build capital rather than deploy it was regulatory uncertainty surrounding proposed capital requirements under Basel III rules (as I wrote last November). Banks have criticized the plan as being overly punitive and warned about the harm to home and business lending. In this context, it was notable that Fed Chair Jerome Powell said in recent testimony to Congress that there would likely be “broad and material changes to the proposal,” and regulators could even scrap it entirely and start over. It’s reasonable to think that some bankers will take this as a sign that they no longer have to be in capital-building mode.

One marker of the more buoyant sentiment is how well the industry weathered the struggles at New York Community Bancorp. There was no repeat of last year’s flight to the safety of JPMorgan Chase & Co with much of the rest of the sector selling off. In fact, the KBW Bank Index was mostly unmoved even as NYCB’s stock plummeted through January and February.

The immediate implications of all this for the economy are that companies and industries can worry less about their ability to refinance debt taken out when interest rates were a lot lower; lenders aren’t battening down the hatches like they were last year. That’s not to say that debt on aging office buildings will suddenly be in high demand, but the commercial real estate industry’s mantra of "Survive until 2025" no longer applies to everyone — a lot more borrowers should be able to refinance loans that were a worry even several months ago. That, in turn, reduces the risk of a cascading wave of defaults that could pressure banks and credit markets more broadly.

It also says something about how much the Fed needs to cut interest rates as they weigh both the upside risks to inflation and the downside risks to economic growth. Lending markets are somewhere between recovering and healthy based on tightening credit spreads, the surge in corporate bond issuance, loan-growth recovery at commercial banks, and a potential shift from tightening to loosening lending standards. Market expectations and Fed guidance for modest policy easing starting toward the summer look like an appropriate dialing back of monetary restraint.

At the same time, the Fed has the firepower for aggressive rate cuts should there be an unexpected stumble in the labor market or broader economy. That would likely turbo-charge credit-sensitive sectors including housing, which has stabilized even with high borrowing costs and where there’s obvious pent-up demand waiting and hoping for lower rates. The economic growth outlook from here looks pretty good, with the only question being whether it’s driven more by investments in tech and artificial intelligence, like we’re seeing now, or by credit-sensitive parts of the economy if the Fed feels the expansion is at risk.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.