Bond traders are cautiously reloading wagers that burned them just weeks ago as the Federal Reserve and key global peers finally appear set to begin reducing interest rates as soon as June.

Previous bets that central banks would be swift to loosen monetary policy in 2024 backfired after authorities maintained their focus on above-target inflation and resilient demand. But last week’s surprise cut in Switzerland and dovish outlooks from Fed Chair Jerome Powell and his counterparts at the Bank of England and the European Central Bank leave investors with reason to once again position for easing.

Among money managers such as Pimco and BlackRock Inc., and one-time bond king Bill Gross, the prospect of lower rates is boosting the allure of shorter-dated obligations due in around five years or less, which stand to gain the most as rate-cut speculation builds.

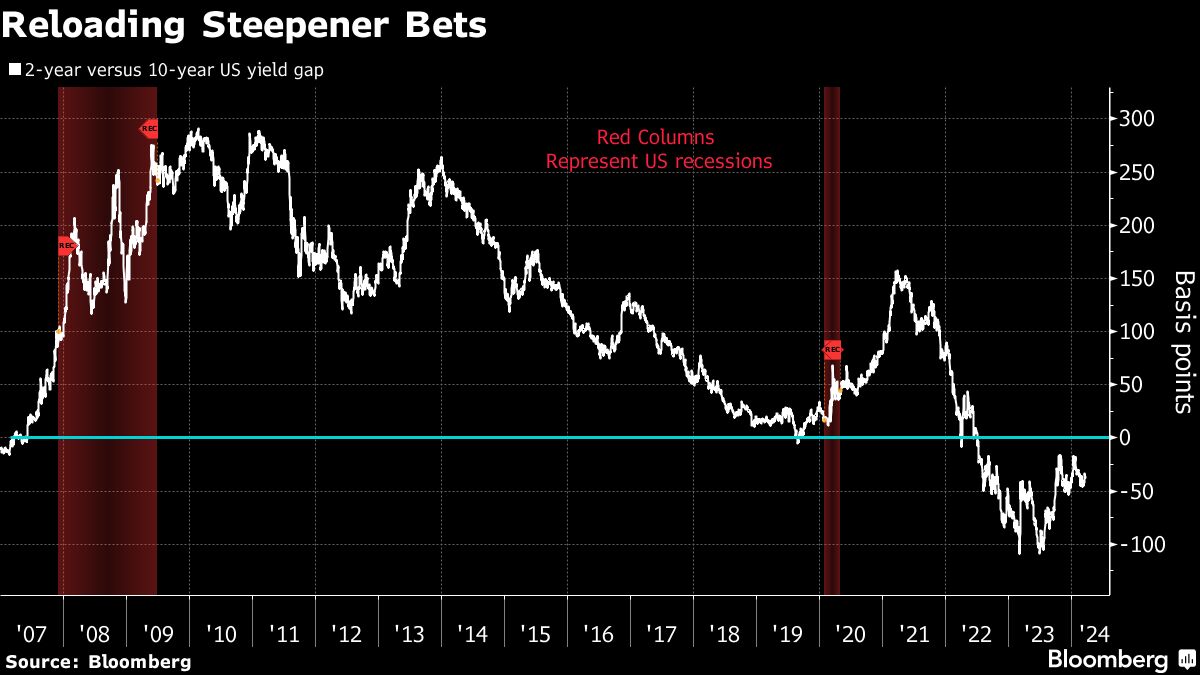

That sort of outperformance relative to longer maturities is a recipe for so-called steepener bets, where the yield curve returns to a traditional upward slope. Of course, there’s still the risk that central banks again fail to vindicate the bullishness around shorter tenors given inflation remains sticky and labor markets continue to hold up.

“Whether we actually get what is priced in is a moot point, but for the current direction of travel, the promise is all that matters for now,” said Jim Reid, Deutsche Bank AG’s global head of economics and thematic research. While markets are focused on a “dovish narrative, it’s worth bearing in mind that sentiment on rates has switched back and forth over 2024,” he said.

Indeed, Reid and his colleagues reckon markets have pivoted towards dovish policy seven times in this cycle and on the last six occasions the outcomes were actually hawkish.

2023 Flicker

For now, investors are feeling a flicker of what unfolded in late-2023. At the time, the Treasury market seemed set for a third straight annual loss, but it rallied into year-end as expectations swept global markets that policymakers would reduce rates early in 2024.

While they seem to be in sync now, central banks could still end up moving at different speeds, which may present money-making openings.

“It’s likely the big central banks such as the ECB, Fed and BOE all get started cutting rates in the middle of this year, and that’s where the similarities stop,” Michael Cudzil, portfolio manager at Pacific Investment Management Co., told Bloomberg Television. “The speed and destination will vary across the globe and that’s great for fixed-income opportunities.”

Rates traders are leaning toward June as the start of the Fed easing cycle, after entering the year banking on a March kickoff. For all of 2024, they see a bit more than Fed officials’ median forecast of 75 basis points of reductions. June is also when markets expect the ECB and the BOE to start cutting, with at least several moves priced in from both.

Among the major central banks, the Bank of Japan stands apart, with economists projecting it will lift rates again later this year, after scrapping its easing program last week.

What Bloomberg Strategists Say...

“If central banks have it their way, we could have first rate cuts from the Fed, ECB, BOC and the BOE all done and dusted by the end of the first half. That means that front-end yields in the major economies will continue to trend lower as there is no point in fighting the central banks.”

— Ven Ram, strategist

Election Twist

For Kellie Wood at Schroders Plc in Sydney, the dovish pivot from most of the key central banks “sets up the bond market to be probably one of the best-performing markets this year.”

Still, she sees room for divergence, especially with the US presidential election looming in November.

“There’s a small window for the Fed to be cutting maybe 50 basis points before the election, but we think that’s as good as it gets,” said the firm’s deputy head of fixed income. Her portfolio is neutral on the US front end, while bullishly positioned in short-dated bonds in Europe and UK gilts.

The US Treasury curve briefly steepened after the Fed met, but two-year yields remain roughly 40 basis points above 10-year rates. The curve has been upside-down like that, or inverted in traders’ parlance, since around mid-2022.

Complicating investors’ calculus around the extent of the steepening ahead, Fed officials revised their inflation and growth outlooks higher last week, and trimmed the number of cuts they anticipate over the next two years.

The revisions for 2025 and 2026 “show that we’re going to have a shallow easing cycle,” said David Rogal, a portfolio manager in the fundamental fixed-income group at BlackRock.

That suggests “some curve steepening,” he said, and for that reason, the group is “underweight intermediate and long-end rates - seven to 30 years — in our portfolios.”

What to Watch

Economic data:

March 25: Chicago Fed national activity index; Bloomberg US economic survey; new homes sales; Dallas Fed manufacturing activity

March 26: Philadelphia Fed non-manufacturing activity; durable goods; capital goods; FHFA house price index; S&P CoreLogic; Conference Board consumer confidence; Richmond Fed manufacturing index and business conditions; Dallas Fed services activity

March 27: MBA mortgage applications; wholesale inventories (revisions)

March 28: GDP (Q4); personal consumption; GDP price index; initial jobless claims; pending home sales; MNI Chicago PMI; U. of Michigan sentiment and inflation expectations; Kansas City Fed manufacturing activity

March 29: Personal income and spending; PCE deflator; advance goods trade balance; retail and wholesale inventories; Kansas City Fed services activity

March 29: Good Friday. Trading in US markets closed

Fed calendar:

March 25: Atlanta Fed President Raphael Bostic; Governor Lisa Cook

March 27: Governor Christopher Waller

March 29: San Francisco Fed President Mary Daly; Powell

Auction calendar:

March 25: 13-, 26-week bills; 2-year notes

March 26: 42-day cash management bills; 5-year notes

March 27: 17-week bills; 2-year floating-rate notes; 7-year notes

March 28: 4-, 8-week bills

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.