Investors who just booked profits from one of the strongest first quarters for the S&P 500 Index in decades are preparing for what comes next — whether that’s stocks climbing higher or crashing back to earth.

With the stock market sitting at an all-time high as the second quarter begins, the tells for what traders are thinking lie in the options market. Demand for put options that pay off if there’s a minor correction is around the lowest in years. Meanwhile, traders are quietly picking up tail-risk hedges: instruments that do little if there’s a slight downdraft but offer protection if stocks swing wildly.

Taken together, it seems Wall Street isn’t particularly worried about a little slump. But there is growing concern that an unpriced risk could knock the bull market off its feet.

“There are a number of tail risks that you can point to, and the market has moved a lot, so I’m not surprised to see demand for tail hedges,” said Rocky Fishman, founder of derivatives analytical firm Asym 500. “I’m more surprised to see the lack of demand for basic hedges.”

As inflation continues to trend downward and the Federal Reserve signals its willingness to cut interest rates this year, rates volatility dropped to the lowest level since February 2022, creating a broadly favorable environment for stocks. The S&P 500 gained 10% in the first quarter — its strongest start to the year since 2019 — and posted 22 new all-time highs in the first three months of 2024.

With the gains so concentrated among a few key stocks, investors are starting to seek value in less-loved corners of the market. Small-cap stocks appear to be on the cusp of a recovery, and the tech-heavy Nasdaq 100 Index got trounced by the broader S&P 500 in the first quarter after beating it in every period last year. To get a sense of the improving breadth, roughly 70% or more of S&P 500 firms held above their 200-day moving averages in each session — its most extended period since 2021.

“The market is showing more and more confidence in a genuine soft landing or even no landing scenario where overall economic growth in the US continues to stay solid,” said Lisa Shalett, Morgan Stanley Wealth Management CIO. “It makes sense that a broader group of companies, even those that are more cyclical in areas like industrials, materials and energy can do well.”

A reawakening meme mania helped, as day traders poured into stocks and equity derivatives to capitalize on the initial public offering of Reddit Inc. and the rally in Trump Media & Technology Group Corp. Retail investors are showing their longest stretch of bullish options market positioning since 2021’s meme stock craze, according to data from Citadel Securities institutional options desk.

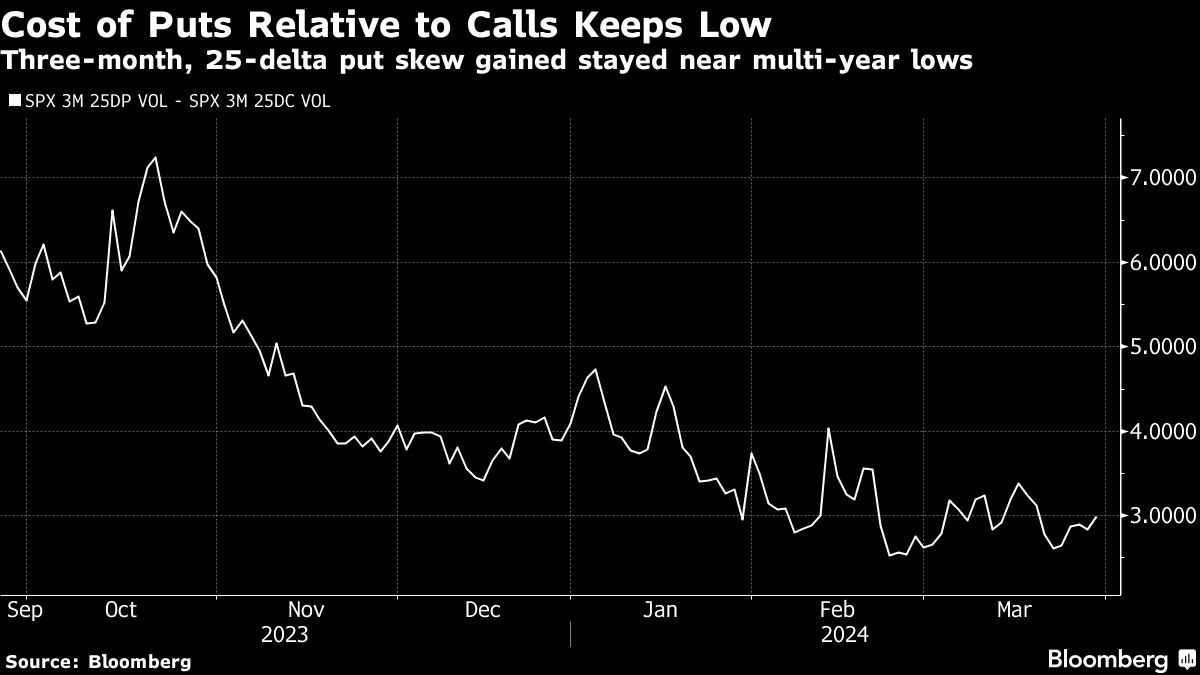

That confidence has investors shedding defenses against a minor correction. The cost of S&P 500 bullish call options expiring in one year with a 25% chance of coming in the money — known as having a 25-delta — is up, while the cost of equivalent bearish puts is down. Meaning investors are ready for continued broad market advances and aren’t particularly worried about a slight pullback.

They are, however, concerned about a disaster, as positioning for a volatility spike increases. Average daily call volume on the Cboe Volatility Index, or the VIX, was higher in the first quarter than the two prior quarters. And its two-month skew — measuring the cost of 25-delta calls against equivalent puts — is around its highest level in five years, according to data compiled by Bloomberg.

Investors are “not so concerned with valuations, earnings, or any of the other run of the mill catalysts that could drive a correction,” said Cboe Global Markets Inc.’s Mandy Xu. “Still, there’s a lot of concern of potential black swan events that could send volatility spiking significantly higher.”

A chief risk is the timing and magnitude of interest rate cuts from the Fed this year. Chair Jerome Powell reiterated on Friday that the central bank isn’t rushing to ease policy after the latest inflation data came in line with expectations. Talk of higher-for-longer rates could dent sentiment in the quarter to come.

There’s also the issue of how broad markets fair should the artificial intelligence darlings that have been driving the indexes stall out. “Stretched positioning and technicals” could prompt tech shares to lead the first leg of a potential selloff, Barclays strategists warned in a recent note.

For now, however, those fears are somewhat contained, and hopes for another solid earnings season could drive valuations further into nose-bleed territory. It’s one reason why protective puts are out, and rally-chasing is in.

“Options traders seem much more inclined to buy ‘FOMO insurance,’” said Steve Sosnick, Interactive Brokers chief strategist — calling out the lack of hedging at the broad market level. “But there’s a lot of room between a correction and true tail risk.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.