Reasonable people can disagree about whether US disinflation is actually stalling and what it might mean for Federal Reserve monetary policy. But it’s getting much harder to deny the underlying strength of the economy, suggesting central bankers can afford to wait before reducing benchmark interest rates.

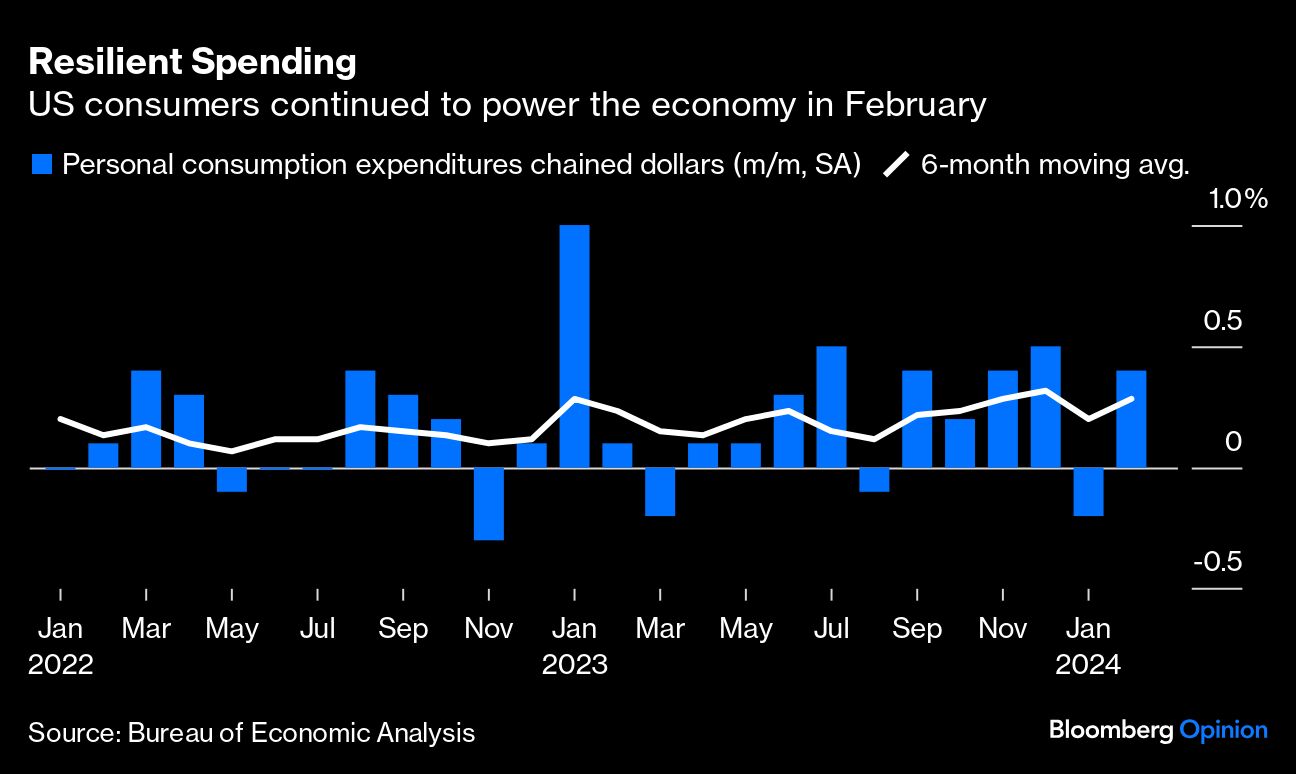

New data Friday from the Bureau of Economic Analysis showed that even after adjusting for inflation, personal spending climbed 0.4% in February, comfortably exceeding the median estimate of economists surveyed by Bloomberg for a 0.1% increase. A day earlier, separate reports showed that consumer sentiment increased to the highest since July 2021, weekly initial jobless claims fell and pending home sales bounced back in February from a decline in January. In an economy that has consistently outperformed and is constantly being scoured for cracks, it’s hard to find any faults in the latest data.

The developments come amid subtle signs of disagreement on the Fed’s rate-setting Federal Open Market Committee when it comes to the interpretation of recent inflation reports. Friday’s data also showed that the Fed’s preferred inflation gauge — the personal consumption expenditures price index — rose 0.3% in February after a 0.4% increase a month earlier. Worries this month that the trend toward slower inflation was being interrupted had unsettled parts of the financial markets, countering the streak of encouraging inflation reports in the second half of 2023. Some observers brushed all this off as noise, while others warned that it could be a sign of sputtering disinflation that merits a rethink of just how many times the Fed may cut rates this year.

In the optimistic camp, Fed Chair Jerome Powell has taken the data in stride. At a press conference on March 20 after the Fed held its target for the federal funds rate in a range of 5.25% to 5.5%, he told reporters that the January inflation data may have been affected by a statistical quirk known as excess seasonality, and that the February data was actually not “terribly high.” At the time, he estimated core PCE inflation would come in at “well below 30 basis points,” and the official numbers released Friday vindicated his framing: taken out to two decimal points, it increased 0.26% — hardly a catastrophe for a central bank that’s hoping for readings at or below 0.2%. Taking the two together, he said that the numbers hadn’t “really changed the overall story which is that of inflation moving down gradually on a sometimes bumpy road.”

Sounding slightly more concerned, Fed Governor Christopher Waller said Wednesday that it may now be necessary to hold the policy rate “at its current restrictive stance perhaps for longer than previously thought” to keep inflation heading toward the central bank’s 2% goal. He also suggested that the 275,000 jobs added to US payrolls in February may be “a sign that demand is not moderating as much as is needed to support continued progress on inflation.”

Powell’s remarks initially sent bond yields lower and Waller’s remarks sent them higher, underscoring the perception of discord. But both men basically agreed on the notion that they couldn’t say for sure where prices were heading, and the economy seemed strong enough to withstand higher rates in the meantime. Neither had made up his mind about anything except to wait. Even Waller noted that he could be convinced to start cutting rates after as few as a “couple” of better inflation reports, suggesting that June and July remain very much in play in terms of timing for a rate cut. This week’s data seemed to validate all that.

I’m still an avowed inflation optimist, so I tend to fall in line with Powell’s interpretation of the data. In addition to excess seasonality, the January numbers were marred by obvious statistical noise in the owners’ equivalent rent category — a large component that’s meant to proxy the inflation experienced by homeowners — and the February data was pressured by notoriously volatile airfares. I suspect the data will be back on track in a month or two.

But there’s no need to jump to premature conclusions. Policy choices will only get hairy if Powell and I are proved wrong and the inflation remains stubbornly elevated for months more, extending the rate-cut waiting game into autumn or beyond. And while the macro data is strong today, there are plenty of areas of vulnerability across the interconnected global economy. China is wobbling and European growth is anemic, and many central banks are loath to lower policy rates ahead of the Fed, raising the risk of an economic accident that starts elsewhere but ultimately lands back in North America. The Fed’s mandate only concerns prices and unemployment at home, but policymakers can’t ignore the global implications either.

Fortunately, for now, the data suggest that policymakers have time to see how the situation develops. In that respect, there doesn’t appear to be very much daylight between Powell and Waller.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.