For a brief moment last week, the market and the Federal Reserve were on the same page about the pace of monetary easing. It didn’t last long, and Treasuries investors are paying the price.

After spending much of this year making bets that were much more dovish than those of Fed officials, investors have now flipped in the opposite direction. They’re forecasting about 65 basis points of rate reductions in 2024, compared to the 75 basis points signaled by the median estimate of projections released following the Fed’s March 19-20 meeting.

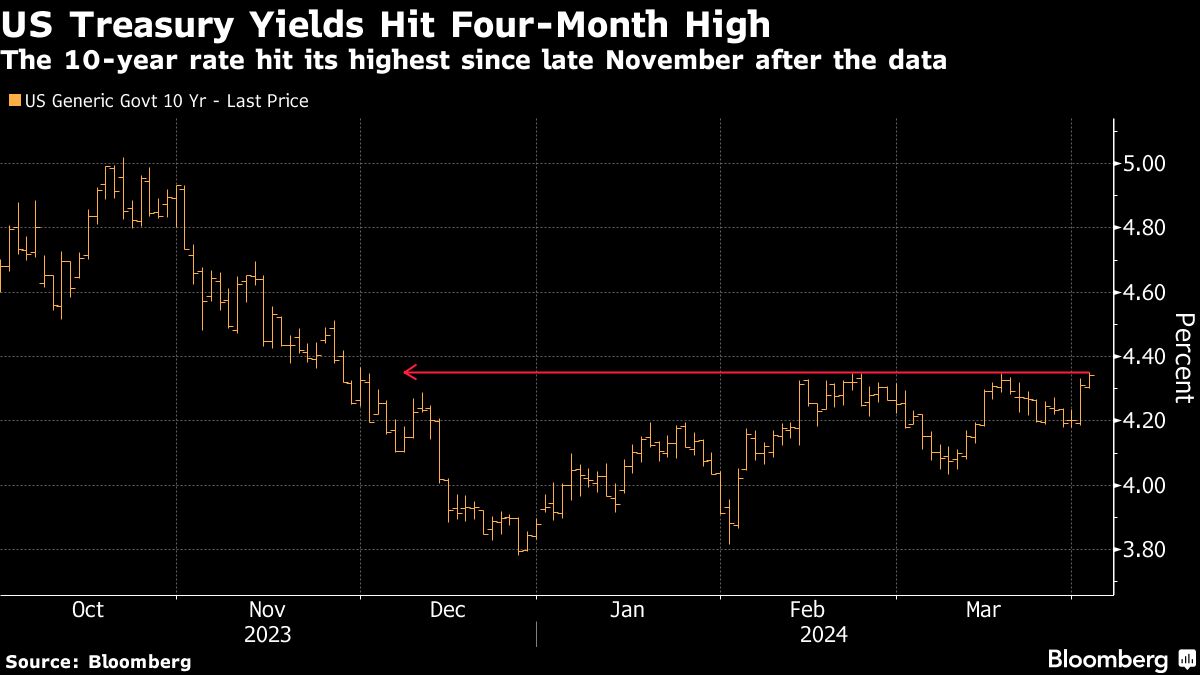

The reassessment is driving investors to demand higher rates of return on US government bonds. Yields on Treasury debt maturing in five to 30 years climbed to the highest levels this year Tuesday. The 30-year yield topped 4.5%, and the benchmark 10-year note is higher by nearly 20 basis points over the past two days, on pace for its biggest jump since early February.

“I thought it would be hard for the market to challenge the Fed on the hawkish side, but apparently it is willing to do so, in the face of some evidence,” said Benoit Gerard, a rates strategist at Natixis in Paris.

Traders are reacting to a couple of economic data points from the past few days that point to strength in the US economy, potentially reducing the need for rate cuts. Reports Tuesday on job openings and factory orders, though also stronger than anticipated, had little impact on already elevated yield levels. Key employment data for March are ahead Friday.

The impetus to higher yields began Friday, when US markets were closed. Income and spending data for February that showed consumption remains strong. Then, on Monday, a gauge of US manufacturing activity expanded for the first time since 2022, exceeding all estimates in a Bloomberg survey of economists.