Treasury yields reached their highest levels of the year Monday — where they swiftly attracted buyers — as traders decided two Federal Reserve interest-rate cuts are likelier than three this year.

Loss of faith that the Fed will deliver on the three quarter-point rate cuts that policy makers last month said they expected began gathering pace on Friday in response to strong March employment data. Swap contracts that predict Fed rate changes on Monday priced in around 60 basis points of easing this year beginning in September, a view that assigns less than 50% odds to a third cut.

While the new view prompted investors to demand higher rates of return on Treasury notes and bonds — pushing the benchmark 10-year note’s above 4.45% for the first time since November — the enduring expectation even for a smaller amount of Fed easing continues to benefit the market. Among the buyers Monday was an apparent bargain-hunter in the futures market, where a large block trade targeting the 10-year part of the market was done near the cheapest levels of the day.

“Treasury yields are trading now closer to the upper end of our expected range and so it does create a pretty attractive entry point,” said Steven Oh, global head of credit and fixed income at Pinebridge Investments.

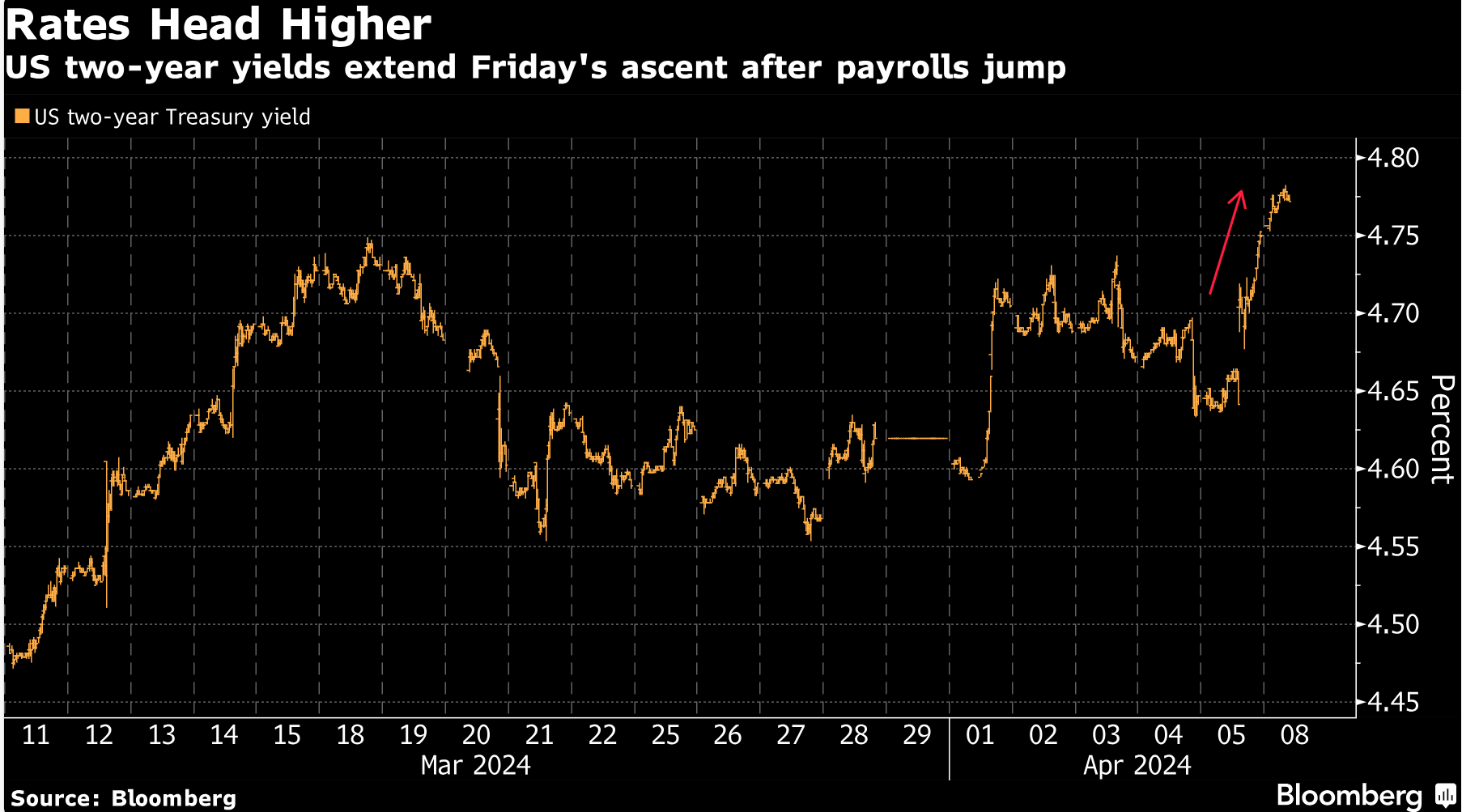

Strong demand for 10-year Treasuries is anticipated if the yield tops 4.5%, also for the first time since November. Yields across the maturity spectrum climbed to fresh 2024 highs, including the two-year for the first time since March.

More sensitive than longer-maturity debt to changes in the Fed’s rate, two-year Treasury yields rose to 4.79%, the highest level since Nov. 28. Among the shifts in expectations based on March employment data, economists at JPMorgan Chase & Co., while still expecting three cuts this year, predicted the first one in July rather than June.

Markets have been tempering bets on Fed cuts for days as US economic data remains resilient and Fed officials have pushed back against the need for easing, with some even stressing a risk of hikes should progress on inflation stall. US consumer price data is due on Wednesday is the next key hurdle for the market.

At the start of the year, expectations were widespread that the Fed’s 11 rate increases in the past two years would not only curb inflation but also cause economic stress, leading the market to bet on as many as six cuts this year. Instead, progress toward lower inflation has slowed, growth metrics have remained robust, and investors continue to shovel money into stocks and corporate bonds at a pace that suggests the economy doesn’t yet require lower rates.

That’s seen Treasuries sell off, upending the carefully calibrated portfolios of investors who bet that bonds would go on a tear. A Bloomberg gauge of US Treasuries has lost 2% this year.

“The risk is that you get higher Treasury yields from here,” said Nils Overdahl, a senior portfolio manager at New Century Advisors. “The recent robust data gives the Fed cover to be patient. There is also some question — given the strength of the data and that the Fed is likely cutting this year — what that means longer-term for inflation pricing.”

Overdahl said New Century isn’t jumping in to buy Treasuries at this time. “You have to be patient, especially with CPI coming out on Wednesday,” he said.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Greg Ritchie, Liz Capo McCormick