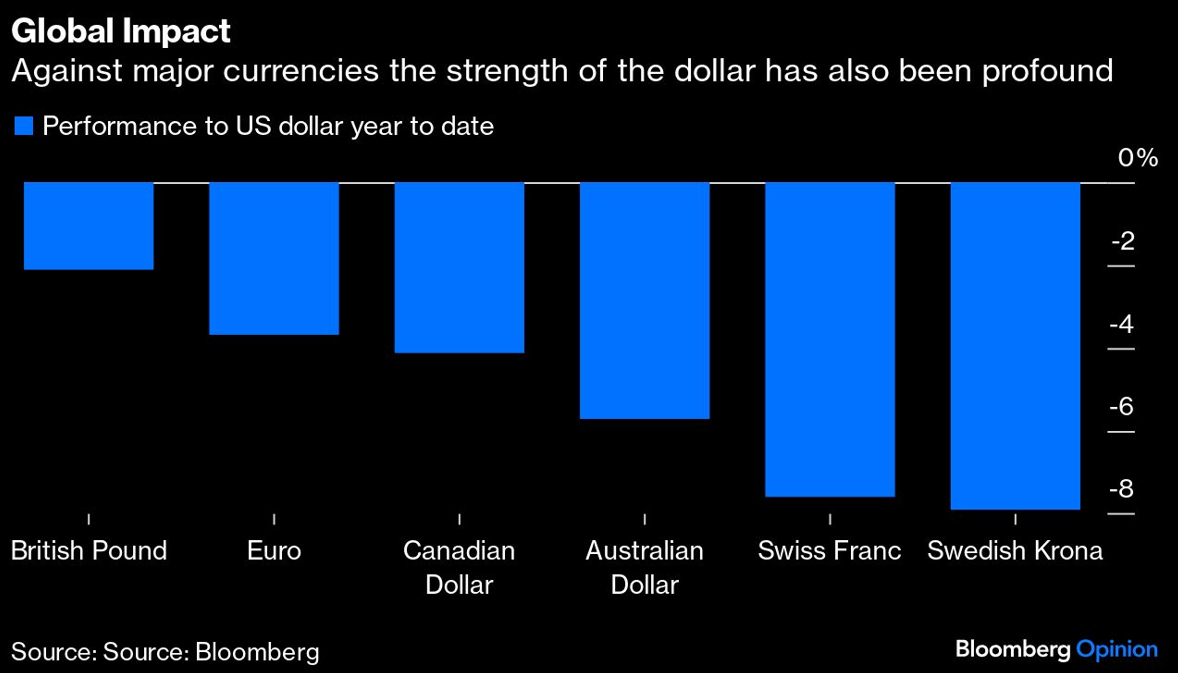

When does a strong dollar become too strong? “Right now” would be the cry of most emerging-market currencies, not to mention policymakers in Japan. Even the European Central Bank says it’s paying attention to the foreign exchange market.

The relentless rise of Treasury yields is translating directly into dollar strength, laying waste to the value of other currencies. It’s not a crisis yet; but trying to call a top is futile, and the risk of something breaking is increasing. As the US economy becomes ever more internally strong and self-obsessed, emerging-market economies are likely to suffer first and most.

All eyes are on the Federal Reserve as the omnipotence of its economy leaves the US central bank in an invidious position, as evidence of an economic slowdown and an accompanying slowdown in inflation proves hard to find. The dollar remains oddly impervious to the US government’s burgeoning debt load, widening deficits or potential political instability accompanying the upcoming presidential election. Amid increased geopolitical concerns it remains the preferred choice for investors to park cash safely at yields of more than 5%, and is also the avenue for speculating on the latest tech craze in US equities.

Fed Chair Jerome Powell has now acknowledged market concern that sticky inflation will stay the central bank’s hand from cutting interest rates. The world could just about handle higher for longer as long as there really is an eventual Fed Funds cut. But if the next move turns out being a hike — which, to be clear, the Fed is absolutely not currently signaling — it would be utterly gut-wrenching. With the BRICS-plus set of countries already diversifying away from the dollar as the default reserve currency, as gold surging to a record indicates, an overly strong dollar could accelerate this process.

It doesn't really help either that the dollar is also positively correlating with a rising oil price. It's too much of a stretch to label the greenback a petrocurrency; nonetheless, as US shale-oil explorers have the ability to scale up, crude prices being buoyed by geopolitical tensions will only add to the dollar's resilience.

The International Monetary Fund this week unveiled its predictions for the global economy, and the divide is stark — and widening. US gross domestic product is forecast to grow 2.7% this year, more than twice the rate of Canada, the second-best performer in the Group of Seven. But the staggering bit was the size of the 0.6 percentage point upgrade in the IMF’s estimate of US potential. Meanwhile, other parts of the world are increasingly becoming more dangerous, divided, indebted and unequal. It doesn’t help that excessive domestic US fiscal stimulus is proving toxic for industry everywhere else. It’s unusual for ECB President Christine Lagarde to voice concern about the euro’s value; on Tuesday, she warned that the Governing Council “must be very attentive to FX rate changes.”

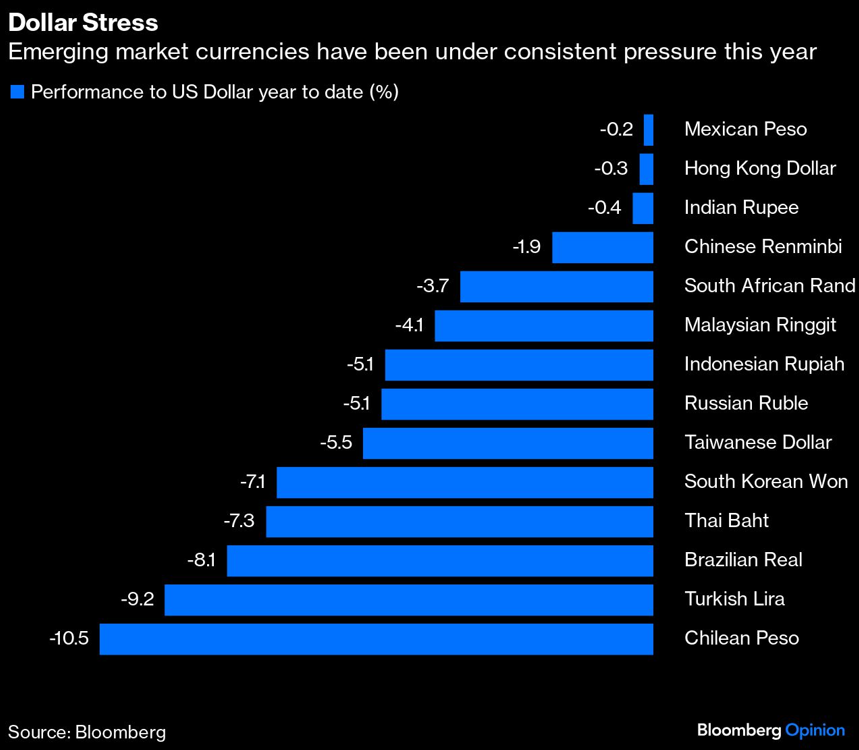

The long and sorry list of flailing Asian currencies is perhaps the most concerning consequence of the moves in the foreign exchange market. The Japanese yen can look after itself, as the relative strength of its stock market in recent months attests. There's plenty of firepower available to the Bank of Japan should it become confident that any prospective Fed change-of-mind on the direction of monetary policy won't destroy the effect of any intervention. Japan is resource poor, so a weak currency seriously damages its balance of payments; but that’s more than compensated by the concomitant boost to its exports. Nonetheless, the credibility of the Bank of Japan is being tested as the yen approaches 155 to the dollar.

China is also in an invidious position. On Tuesday, it surprisingly lowered its key daily reference rate, which weakened the yuan further to a five-month low to the dollar. South Korea has the worst-performing currency this year, as it's so highly sensitive to its fellow major Asian competitors; the won is at its weakest since late 2022. It’s prompted some verbal intervention from Finance Minister Choi Sang-mok, who expressed “serious concern.” Governor Rhee Chang-yong said the Bank of Korea is “ready to deploy stabilizing measures.”

China, Japan and Korea are also trapped in a competitive triangle among themselves that exacerbates the repercussions of the rising dollar. As my Bloomberg Opinion colleague John Authers points out, the yen is at its weakest to the yuan for more than 30 years. That elastic can only stretch so far; but the downside risks of a failed support operation are correspondingly larger. If one moves aggressively to bolster its currency then the others will likely be forced to respond accordingly.

The rest of Asia is unavoidably caught in the downdraft, though their relative performance during the pandemic illustrates how much the region has improved its economic management following repeated crises in previous decades. Foreign exchange reserves have been built up, and interest rates raised earlier and higher to keep one step ahead.

The Indonesian rupiah has fallen to the cheapest for four years, forcing the central bank to intervene. The Taiwan dollar is the lowest in eight years, the Malaysian ringgit for 26 years (the central bank has pledged its support) and the Indian rupee is at a record low to the dollar. Considering the Indian economy is expected to grow by 6.8% this year, according to the IMF's estimates, it illustrates quite how powerful the greenback’s surge is.

The MSCI gauge of emerging-market currencies has hit a new low for the year, but it's clear Asia is where the most damage is. It's reassuring that Powell made clear that "we are very, very aware" of the impact of dollar strength, but talk is cheap; being the custodian of the world’s reserve currency comes with a responsibility not to use it to bully your global trading partners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Marcus Ashworth