Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Ongoing planning in retirement involves periodically assessing whether spending may be increased or must be decreased to remain on track. In his recent Kitces.com article, How Communicating Guardrails Withdrawal Strategies Can Improve Client Experience and Decrease Stress, Dr. Derek Tharpe said:

“However, the results of [Monte Carlo] simulations generally don't account for potential adjustments that could be made along the way (e.g., decreasing withdrawals if market returns are weak and the probability of success falls, or vice versa), making them somewhat less useful for ongoing planning engagements where an advisor could recommend spending changes if they become necessary.”

and

“Nonetheless, while these thresholds and the dollar amount of potential spending changes might be clear in the advisor's mind, they often go unspoken to the client. Which can lead to tremendous stress for clients, as they might see their Monte Carlo probability of success gradually decline but not know what level of downward spending adjustment would be necessary to bring the probability of success back to an acceptable level.”

If you do not currently employ spending guardrails, or your spending guardrails are “uncommunicated” to your clients, you may wish to add the Actuarial Approach to your consulting toolkit to improve:

- your consulting skills

- the ongoing planning experience for your clients

- your revenue

In this article, I will:

- briefly describe the Actuarial Approach

- outline why I believe it is a more robust approach for ongoing planning than Monte Carlo modeling approaches (with or without guardrails) or strategic withdrawal approaches (with or without guardrails)

- describe how guardrails can be easily developed and used within the Actuarial Approach

- provide an example

The Actuarial Approach

The Actuarial Approach has two main components:

- A deterministic actuarial financial planner (AFP) model that compares total household assets with total spending liabilities in retirement to determine the household’s funded status as of a snapshot valuation date

- an actuarial process, which involves remeasuring the household funded status periodically (generally annually) to monitor it over time and, if necessary, to make adjustments in assets or liabilities to restore the desired funded status

The Actuarial Approach, which is similar to the approach used for Social Security funding and pension plan funding, is not a stochastic approach designed to estimate the probability of “success” for a given annual level of spending during retirement or of a proposed investment mix. It is designed to alert users to changes in the household balance sheet that may be required to maintain the household’s desired funded status on an ongoing basis. To facilitate household spending decisions, the financial advisor can establish and communicate “spend less” (or, in theory increase assets) or “spend more” guardrails.

As noted above, the household funded status under the AFP model is equal to the ratio of total household assets to total household spending liabilities. The AFP is a “two-bucket” model that separates essential and discretionary expense liabilities and anticipates separately funding them in a manner consistent with liability-driven investing (LDI). It also distinguishes between recurring and nonrecurring household expenses and expenses with different expected rates of future increases.

Under the AFP, the funded status as of the valuation date is represented by the following equation:

Funded Status = (PV of Risky Assets + PV Nonrisky Assets) / (PV Discretionary Exp. + PV Essential Exp.)

“PV” stands for present value as of the valuation date, which is determined using different discount rates for the assets and liabilities in the two different risk-related buckets.

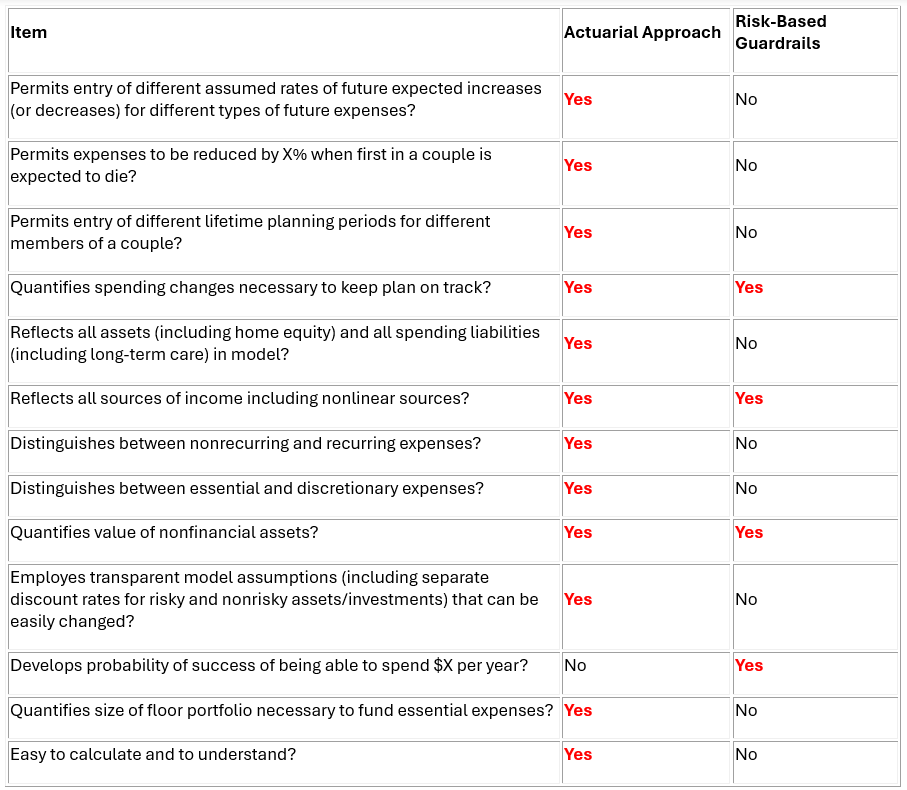

What makes the Actuarial Approach more robust for ongoing planning?

Dr. Tharp and Justin Fitzpatrick of Income Lab have done a good job of describing some of the communication problems associated with probability-of-success Monte Carlo modeling typically employed by financial advisors and the weaknesses of structured withdrawal programs (with and without guardrails). I agree with these gentlemen but believe that financial advisors can do even better with the Actuarial Approach. Below is a is a functionality comparison I prepared for the two approaches.

Functionality Comparison of Actuarial Approach vs. Risk-Based Guardrails

Developing and using guardrails under the Actuarial Approach

I recommend starting with funded status guardrails of 95% and 125%. The increase-spending guardrail of 125% will likely involve more discussion with clients. Some clients with lower risk tolerance and/or relatively larger upside portfolios may prefer a higher than 125% increase-spending guardrail. In developing the exact guardrail percentages, it may be helpful to estimate what the client’s funded status would be and whether the decrease-spending guardrail would be triggered (and by how much) if their risky assets (upside portfolio) suffered a 50%, or greater, loss in the near future.

It should be noted that if the decrease-spending guardrail is triggered, the client household would be informed that their discretionary spending should be reduced to such a level that their funded status increases to 95%. The AFP model can be used for this purpose. Alternatively, the client may find additional assets (such as renting a room, part-time employment, etc.) to increase the household funded status to 95%. Those clients who do not particularly relish the thought of reducing discretionary expenses in the future may wish to be more conservative in developing their funded status calculation or in their risky-asset investments.

Example

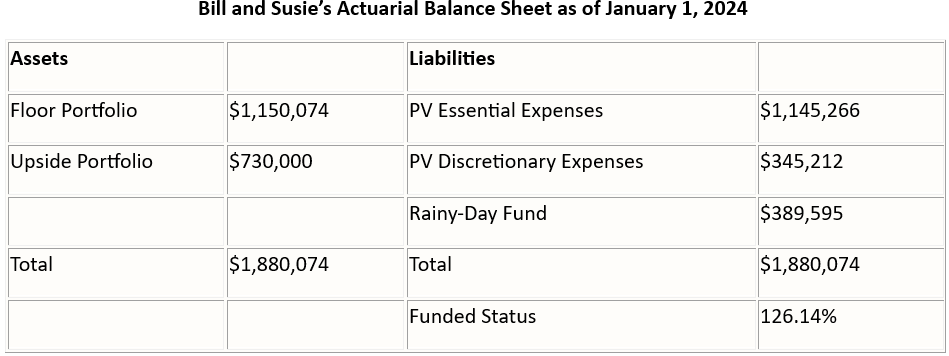

Let’s assume that Bill and Susie’s actuarial balance sheet looks like this as of the beginning of the year:

Bill and Susie’s funded status is determined by dividing the present value of their assets by the present value of their spending liabilities (ignoring the rainy-day fund), or

($1,150,074 + $730,000) / ($1,145,266 + $345,212) = 1.2614

We use a little algebra to estimate how much their upside portfolio would need to drop to trigger a reduction in their discretionary spending, assuming they use 95% as the spend-less guardrail.

($1,150,074 + X ($730,000) / ($1,145,266 + $345,212) = .95

Solving for X, we get .364, or a 63.6% drop in their upside portfolio would reduce the couple’s current 126.14% funded status to the “spend-less” guardrail of 95%.

If they wanted to increase their discretionary spending, what percentage could they increase discretionary spending by to reduce their funded status to 125%?

Again, using a little algebra and solving for Y, we get 1.039, or a 3.9% increase in their discretionary spending to reduce the couple’s funded status of 126.14% to the spend-more guardrail of 125%.

($1,150,074 + 730,000) / ($1,145,266 + Y (345,212) = 1.25

Finally, Bill and Susie would like to know what their funded status would decrease to if their upside portfolio suffered a 50% loss and their spending didn’t change.

(1,150,074 + $730,000 (.5)) / ($1,145,266 + 345,212) = 1.02

Bill and Susie determine that even though their risky assets have increased since the beginning of this year, they are happy with their current spending plan at this time. They will continue to monitor their funded status from year to year to see if future spending changes may be appropriate.

Conclusion

In his article, ‘Probability of Success’ Doesn’t Mean What Your Clients Think it Means, Justin Fitzpatrick argues for a better framework for financial advisors that would enable them to help clients find the appropriate balance between risk and reward. He said,

“The solution is to jettison probability of success from retirement planning and adopt a more accurate and effective vocabulary and set of tools.”

I agree. I just believe that the Actuarial Approach, based on its proven actuarial principles, is a better tool for facilitating ongoing retired client spending decisions.

I encourage financial advisors to check out the Actuarial Approach on my website and consider it, or a modified version of it, for inclusion in your consulting toolkit. The AFP is a simple Excel spreadsheet, but it is quite robust. If you still want to keep Monte Carlo modeling in your toolkit, that’s fine. But I suggest that you sync the two models to make them consistent, to the extent possible, and use the tool that best addresses your clients’ specific needs for the assignment purpose.

Ken Steiner is a retired actuary with a website titled "How Much Can I Afford to Spend in Retirement?"

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.