Elon Musk is known to challenge the status quo — and that’s exactly what Tesla Inc.’s investors are worried about right now.

The company’s shares are weathering the longest rout since late 2022, tumbling nearly 19% over the past seven days, amid doubts about its business strategy as sales of electric vehicles slump.

The latest worry? That Musk, Tesla’s chief executive officer, will announce plans on Tuesday’s earnings call to nix the rollout of a cheaper model and focus on developing a fully self-driving vehicle — a project that would face considerable regulatory and commercial obstacles.

That would mark a major break with what analysts had been expecting and leave the company with no near-term catalyst for growth, just when it’s expected to report the first quarterly sales drop since the pandemic struck in 2020.

“Up until several weeks ago, the key focal point into the first-quarter result was Tesla’s vehicle sales fundamentals, with Tesla facing an extremely challenged set-up amid a sharp delivery miss, risk of no growth in volume in 2024, and further pressure to margins,” said Barclays Plc analyst Dan Levy, who has the equivalent of a neutral rating on the stock.

Levy said those issues have since taken a back seat to a bigger issue: “An investment thesis pivot.”

Such concerns have driven the stock down nearly 43% this year through Monday’s close to $142.05, a 15-month low. It’s the second-worst performer in the S&P 500 so far this year, lagging only Globe Life Inc., an insurance company targeted by short sellers. On Tuesday, the shares were down 0.5% at 9:41 a.m. in New York.

This year’s slide in the stock has raised the risk that any disappointment in Tuesday’s earnings report or Musk’s conference call could snowball, according to technical analysts who analyze moves in share prices to predict their future path. To them, the drop below $150 has already breached a key support level.

“The stock is now in no man’s land, with a massive air pocket between here and under $100,” said Todd Sohn, ETF and technical strategist at Strategas Securities.

Musk has already said that the company will be unveiling its so-called Robotaxi in August but hasn’t clarified the plans for the cheaper vehicle. It is possible that Tesla is only going to delay the production of the less-expensive car, rather than shelve it outright.

But the concerns about Tesla’s strategy are exacerbating investors’ nervousness at a time when the company is already contending with slowing growth, thinning margins and sales. Vehicle deliveries for the first quarter, which were announced early this month, lagged analysts’ forecasts by the most in at least seven years.

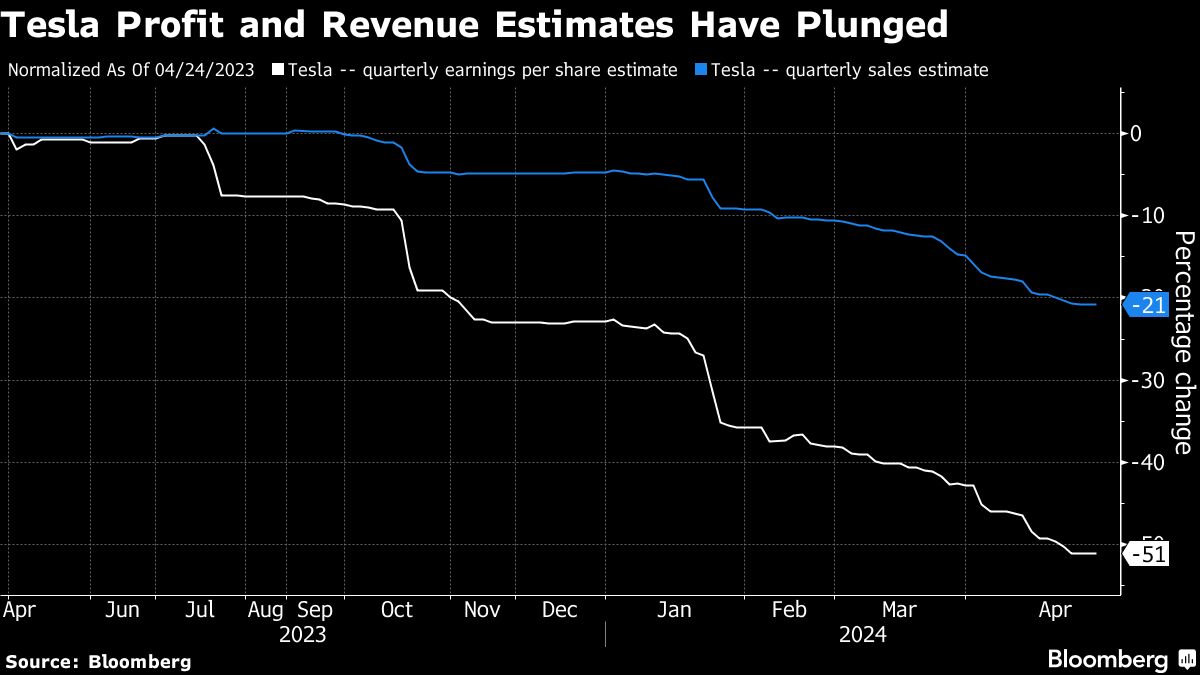

Over the past 12 months, expectations for first-quarter earnings have been dialed back to 52 cents a share, half of what was once anticipated. The revenue forecast — now about $22.3 billion — has been cut 22% over that time, according to data compiled by Bloomberg, while estimated free cash flow slid 70% to around $654 million.

That’s why Tesla’s stock-price still looks high, by some measures, despite the recent drop: At nearly 47 times forward earnings, it’s significantly more expensive than every other member of the so-called Magnificent Seven tech stocks.

On the flip side, the negative sentiment has set a relatively low bar, creating the potential for a relief rebound.

“The news flow and psychology surrounding Tesla have become so negative that a modest miss may already be getting priced in,” said Steve Sosnick, chief strategist at Interactive Brokers LLC.

But that hasn’t tended to be the case. Tesla shares dropped at least 9% the day after the past four quarterly reports, and options trading implies expectations of an 8% move in either direction following Tuesday’s numbers.

Demand for short-term puts paying off on a 10% slide has jumped to its highest premium over equivalent calls since November. All told, that signals that investors are paying more for protection in case the stock slips, as opposed to options that position for gains.

“The earnings are so crucial,” said Sosnick. “If we get a profound disappointment, then $100 is a likely next stop.”

Tech Chart of the Day

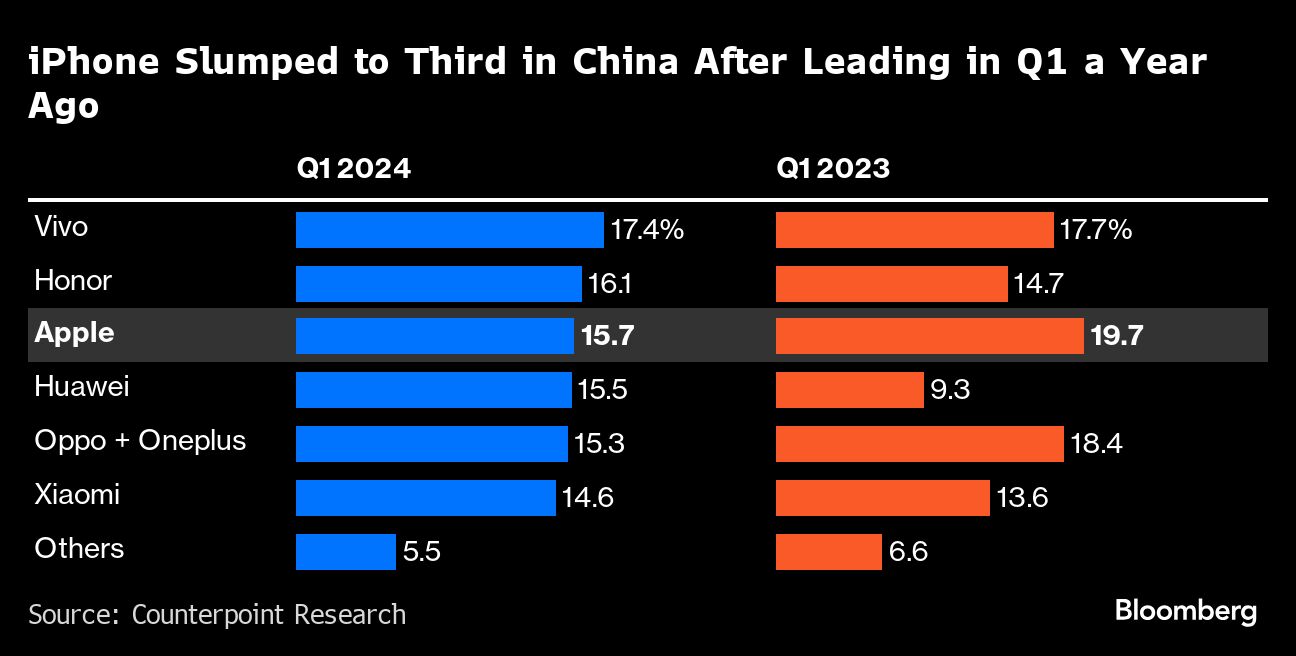

Apple Inc.’s iPhone sales in China fell 19% during the March quarter, according to data from Counterpoint Research that marked the device’s worst performance there since Covid struck around 2020. The US firm dropped to third in the market, roughly on par with Huawei Technologies Co.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.