Wall Street Humbled as Fast-Reversing Markets Confound the Pros

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWith inflation up, economic growth down and two-year Treasury yields testing 5%, Bill Gross sensed the music in markets was fading, and said it was time to get over the likes of the Magnificent Seven.

“Stick to value stocks,” the Pacific Investment Management co-founder posted Thursday morning on X, formerly known as Twitter. “Avoid tech for now.”

Just a day later, the tech-heavy Nasdaq Composite Index notched its best session since February after Microsoft Corp. and Alphabet Inc. showed the AI earnings bonanza still has juice.

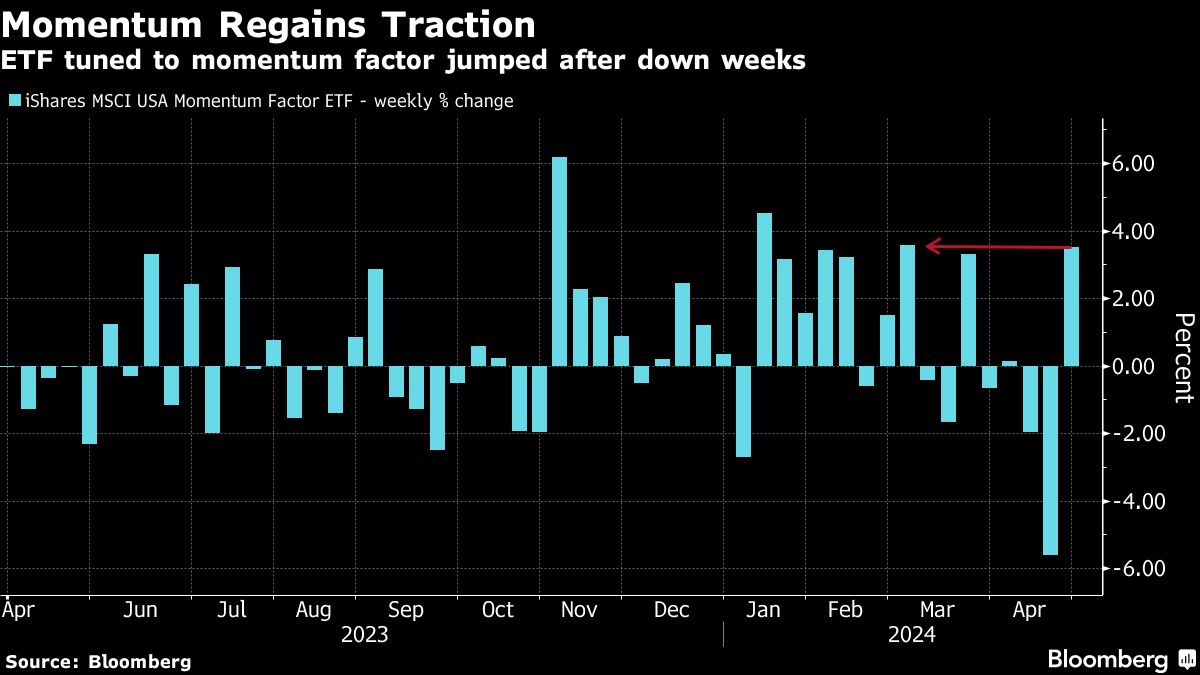

It’s the latest gut-check for anyone trying to get a handle on the short-term moves of markets, just as new questions emerge about the viability of an economic soft landing. An ETF riding the momentum trade shot up 3.5% this week, after plunging 5.6% in the previous week.

Macro signals continue to confound. Growth eased more than expected, a report showed Thursday, yet indicators of consumption and investment remain constructive. A day later strong personal-spending data was duly cheered by economic bulls, while raising the eyebrows of inflation hawks.

Undeterred, money managers just pushed the S&P 500 more than 2.5% higher on the week as they continue to pay through the nose for companies that promise to post profits in the years ahead.

“Tech/growth used to be affected by higher yields,” Gross wrote in an email to Bloomberg on Friday. “But not for now.”

With swings in stocks and Treasuries elevated, money managers sharing the bond king’s caution have been rushing to hedge richly priced equities via exchange-traded funds. Meta Platforms Inc. and International Business Machines Corp., for example, lost $150 billion in market value combined on Thursday alone.

Yet even as traders price out the Federal Reserve’s mid-year monetary pivot — pressuring yields higher — risky assets remain remarkably stable. And recent market moves along with mixed economic data are providing a lesson in humility for swaths on Wall Street. Thursday’s GDP report was especially jarring, showing growth a scant 1.6% and core inflation at 3.7%, both outside the predictions of all the estimates in Bloomberg surveys.

“The recent spate of hotter-than-expected inflation data is throwing a wrench in most people’s models. It’s always difficult to spot inflection points in markets,” said Chris Zaccarelli, chief investment officer at Independent Advisor Alliance. “It’s hard to be humble and admit that you don’t know which way things will go, so we have to talk about the importance of diversification and some tail risk hedges.”

A week after sliding 5.4%, the Nasdaq 100 bounced back to climb 4%, including a 3.3% gain in its seven mightiest stocks on Friday alone. Investors who had been bailing from equities and junk bonds found themselves diving back in this week, according to Bank of America citing EPFR Global.

Resilience was the theme of the week in every market except Treasuries, where yields hovered at multi-month highs. Interest-coverage ratios have improved for both investment-grade and junk bonds amid strong earnings and lingering bets on monetary easing, according to Torsten Slok, chief economist at Apollo Global Management. The ratio between companies’ earnings and their interest expense is starting to rise again, signaling they have more income to service their debt.

For William Hobbs, head of UK multi-asset wealth at Barclays Wealth Management, this was an opportunity to buy the dip and tilt the broader portfolio in favor of risk.

“In spite of the box office start to the year for many developed stock markets, our proprietary measures of investor sentiment and positioning are not close to flashing red,” Hobbs said.

Yet, signs of anxiety were brewing amid a week of uneven earnings results, with the drops in Meta and IBM more than offset by weekly gains of 12% in Google parent Alphabet and a 14% rally in Tesla Inc. The Cboe NDX Volatility Index — a gauge of option costs tied to the Nasdaq 100 — has been hovering around 20 after spiking to its highest level since October last week.

Consensus forecasts still put net margins for the tech sector at all-time highs by the end of 2024, according to Bloomberg Intelligence. This is one reason risk assets have continued to defy threats from rising bond yields even as their valuations and expected cash flows are influenced by interest-rate changes. The result this week: a trouncing of value stocks by their growth counterparts.

Yet all this threatens to set up fresh stock-bond clashes ahead, with Fed officials gathering next week against the backdrop of a red-hot Wall Street and stubborn price pressures.

“Tighter financial conditions are appropriate to cool a booming US economy,” said Tiffany Wilding, economist at Pimco. “Based on recent comments, the Fed appears poised to deliver, by remaining on hold for longer. In other words, the pivot party is over.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All