Here’s a conversation starter ahead of Berkshire Hathaway Inc.’s annual meeting on Saturday: Warren Buffett should buy Boeing Co.

The idea may sound outlandish on the surface because it rubs against Berkshire’s conservative nature. There’s also the sticking point that Buffett doesn’t do turnarounds and that he wants companies with strong leadership. Then again, Buffett likes to bet on American manufacturing, and he favors industries with moats. Check and check. Also, the upside for Boeing, if the planemaker can get its house in order, is huge.

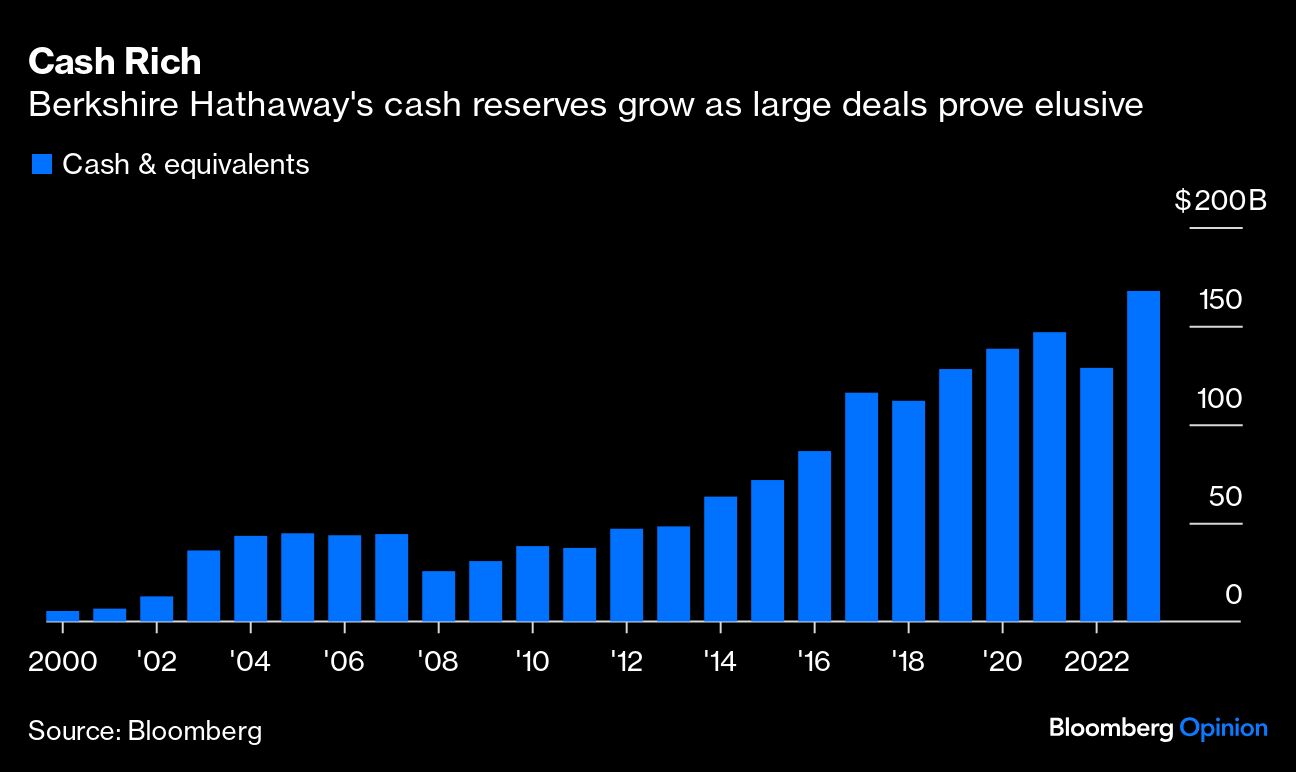

Investors who are gathering in Omaha, Nebraska, on Saturday for Berkshire’s annual meeting will inevitably turn their discussions to how the 93-year-old business legend should deploy the company’s $168 billion pile of cash, which continues to increase. Buffett dabbles in buybacks, but don’t expect that to be a solution.

Buffett has noted that Berkshire is a victim of its own success because the company’s size makes it difficult to make deals and investments to move the needle on growth. For its size — market value of about $860 billion — deals have been modest. Several of the marquee acquisitions, such as Kraft Heinz and Precision Castparts, have underperformed.

One could argue that the pain around the purchase of Precision Castparts, a maker of specialized components for aircraft, would make Buffett shy away from ever investing again in the aerospace industry. Berkshire paid $32 billion for the company in 2016 and ended up writing down $11 billion after the pandemic disrupted commercial flights, throwing the industry into a tailspin. Buffett even conceded in his annual letter in 2021 that he overpaid for the company. To compound matters, Buffett announced in May 2020 that he had sold his stakes in the four largest US airlines at a significant loss.

Precision Castparts has begun to rebound along with demand for aircraft and posted pretax earnings of $1.5 billion last year, a 30% increase from the year earlier. Berkshire has other investments linked to aerospace that do just fine, including the private-jet operator Netjets and Flight Safety, which trains pilots.

Boeing, though, brings an extra dose of risk. The company has caught the eye of Congress after a door plug blew out on a new Boeing 737 during an Alaska Airlines flight in January. That resulted in hearings in April and the promise of more public floggings to come. The Department of Justice is considering nullifying a deferred prosecution agreement from January 2021 that resolved charges of Boeing conspiring to defraud the Federal Aviation Administration during the certification of the 737 Max. The $2.5 billion penalty included payments to the families of the 346 passengers who died in two 737 Max crashes in 2018 and 2019.

The FAA has limited Boeing to producing a maximum of 38 of its workhorse 737 Max jets each month while the company addresses deficiencies in safety culture and production quality. In reality, Boeing isn’t even close to being able to produce that many 737s as it seeks to fix its factory problems and to shore up suppliers. The company burned through $3.9 billion of cash in the first quarter and will spend more to sort out those problems. Boeing’s debt has swelled to about $48 billion after it endured the pandemic and the grounding of its 737 Max and 787 Dreamliner aircraft.

Chief Executive Officer Dave Calhoun was forced to step down at the end of this year after the executives of the main airlines — Boeing’s biggest customers — met with the company’s board to express that they had lost confidence in management. Boeing will likely have to pay up for not meeting contract obligations on aircraft deliveries. On top of that, Boeing’s defense business is struggling because of fixed-cost contracts that have gone over budget. The only bright spot is the global services unit.

So, why in the world would Buffett want to buy this hot mess?

For one, the demand for aircraft is huge. Boeing has a $448 billion backlog to produce more than 5,600 commercial aircraft. There’s only one other large manufacturer of commercial airlines, Airbus SE, and it’s also struggling to keep up with orders. That’s the moat that Buffett likes.

Boeing is also cheap considering the potential cash generation if and when it regains its footing. The shares traded at an average of about $280 in 2017 and 2018 (before the fallout from the 737 Max crashes hit) and have sunk to $178, giving the company a market value of $109 billion. Fixed-income investors are eager to invest in the company. Boeing attracted $77 billion of offers for a $10 billion bond sale last month even though Moody’s Ratings had cut the company’s credit rating to one step above junk less than a week earlier. Even with paying a premium, Berkshire has the cash, and there’s precedent for Buffett raising funds by paring his other equity holdings.

Finally, Boeing would be a bet not only on American manufacturing but on global growth. As countries increase wealth, people fly more. That long-term trend won’t change.

Of course, Greg Abel would have to embrace the idea because he would be tasked with finding a superstar CEO to clean up Boeing. Shareholders, who are attracted to Berkshire’s steadiness, would be shocked at such a bold move. Charlie Munger, Buffett’s longtime vice chairman who died in November at age 99, isn’t around to object.

In the end, the idea of Buffett buying Boeing may be too outlandish, but it’s certainly entertaining to ponder.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Thomas Black