Lagging Real Estate Stocks Have Dropped Too Far, Analysts Say

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWall Street analysts see a double-digit upside potential for the S&P 500’s biggest losers this year: real estate stocks.

All that may be needed to turn the group’s fortunes around, say investors and analysts, is firmer conviction that long-term borrowing costs have plateaued and will head lower. That notion got a boost on Friday after a weaker-than-forecast report on the US labor market caused Treasury yields to tumble.

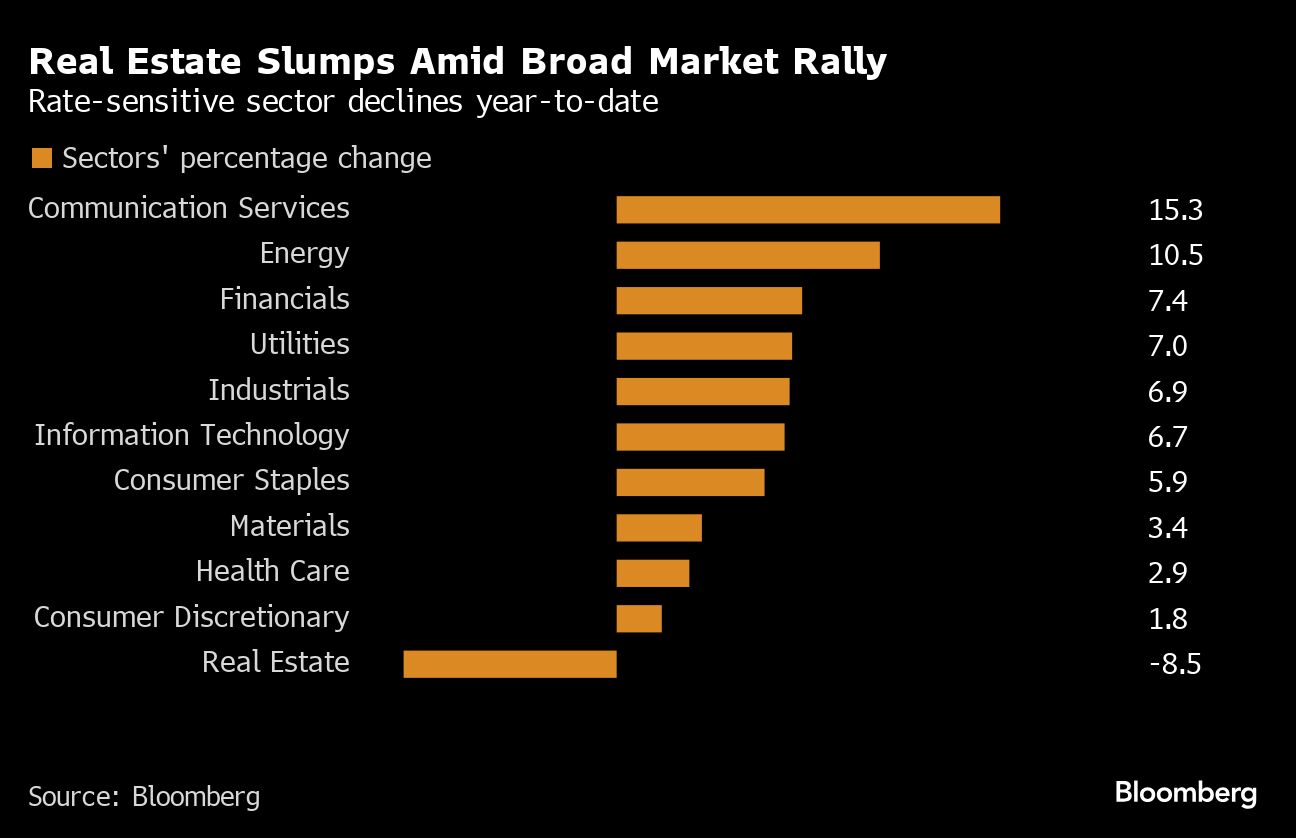

Analysts covering the industry’s stocks expect a 16% rally in the group in the next 12 months, based on Thursday’s closing levels, according to data compiled by Bloomberg. And for the sector’s most troubled names — real estate investment trusts — analysts see 15% upside potential during that time.

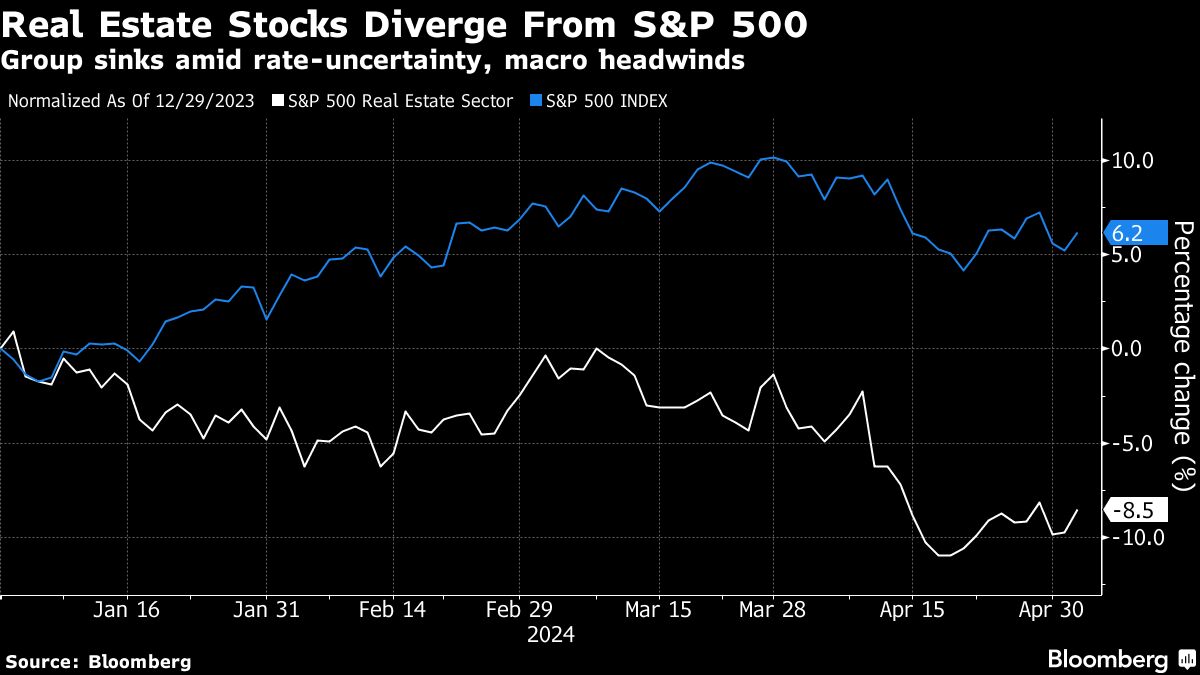

Real estate stocks are coming off of their worst monthly pullback in nearly two years, a slump that came as Treasury yields rose to the year’s highest levels. The group breached its most oversold signal in nearly six months in mid-April, before paring some of the declines.

Federal Reserve Chair Jerome Powell on Wednesday essentially ruled out an interest-rate cut in the near term, a move that would’ve helped a rate-sensitive sector that depends on debt for business.

To Janus Henderson Investors’ Gregory Kuhl, the latest interest-rate meeting may have been an upside catalyst for the group. Policymakers left interest rates unchanged on Wednesday and indicated a willingness to keep borrowing costs elevated for longer rather than raising them again, easing concerns of investors in the beaten-down real estate sector.

“From where listed REITs are currently priced, I don’t believe the market needs to expect rate cuts for REITs to deliver solid performance. If the market reaches a solid consensus that rate hikes are off the table, that may be enough to get REITs going,” Kuhl, a portfolio manager at Janus Henderson, said by email. “It did seem like Powell took rate hikes off the table, which I think is a positive for REITs.”

Historically, REITs haven’t fared well when Treasury yields rise, generally underperforming the S&P after a 100-basis point jump in the 10-year Treasury rate over roughly a median of 170 days. But after yields stabilized, REITs generally rebounded as much as 9% in the next 90 to 180 days, according RBC Capital Markets analyst Michael Carroll.

“The jury’s still out on what happens in this type of environment,” he noted. “But if rates stabilize, REITs could do well and you can start to value them on fundamentals again.” Carroll sees opportunity in industrial, senior housing, single family rentals and data centers REITs.

Still, there are plenty of challenges ahead, including depressed levels of merger-and-acquisition activity.

For now, real estate stocks are being held hostage by the Fed, but for those with a long horizon, the sector’s valuation discount could offer an attractive buying opportunity, said Kuhl. The S&P 500 Real Estate Index is trading at 33 times projected 12-month earnings, an 18% discount to its 10-year average.

If rates go down, multiple expansion coupled with dividend yield growth could be a tailwind for the sector, Kuhl said, similar to the fourth quarter of last year. He expects an 8 to 9% total return for REITs this year, in line with historical averages. He sees forward strength in self-storage, data centers and cell tower landlords.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All