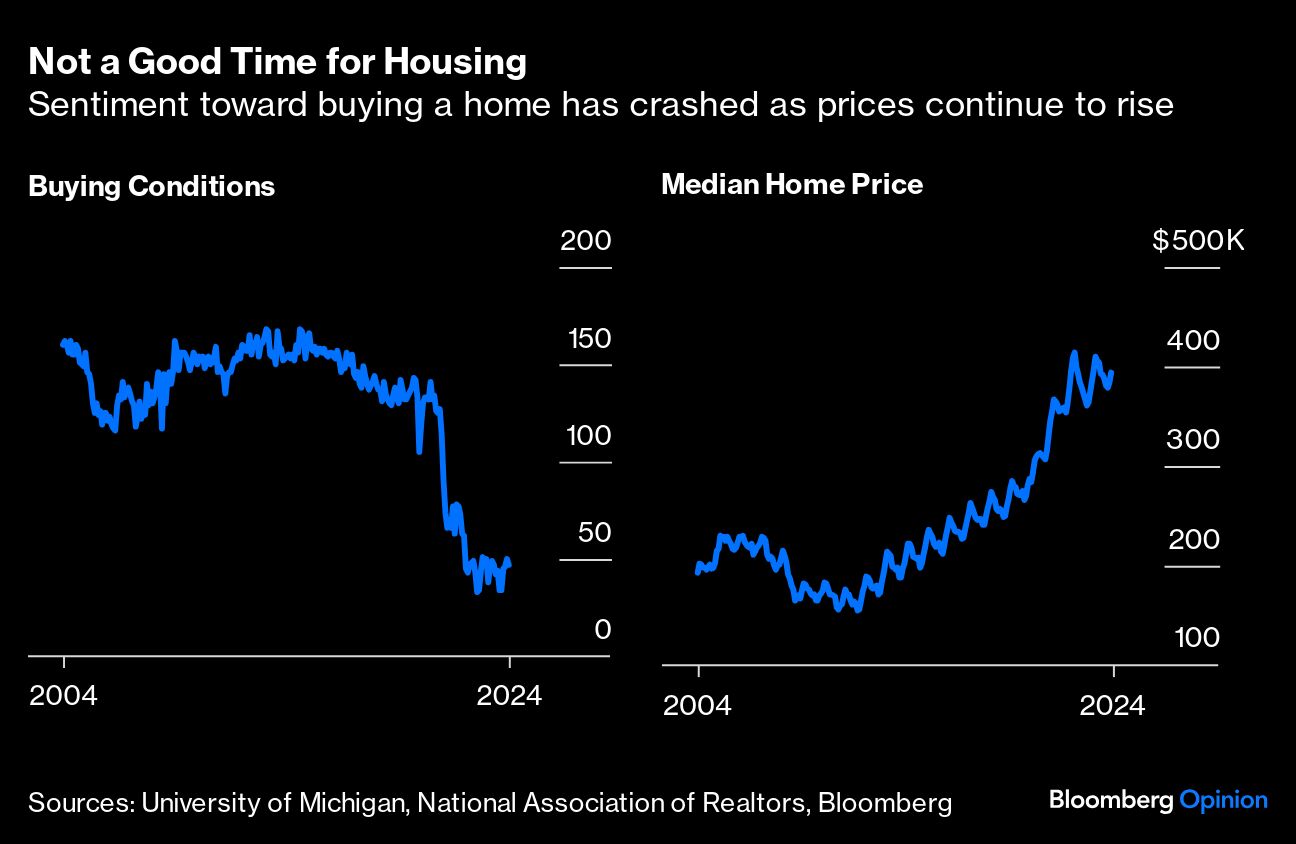

The housing market is a big worry for Democrats as we move closer to US elections in November. It’s one of the primary reasons measures of consumer confidence remain depressed as a combination of high prices and high mortgage rates keep homes out of reach for many. You have to go back to the dark days of the early 1980s to find the last time Americans in the University of Michigan’s monthly sentiment survey were so downbeat when asked whether it was a good time to buy a home.

All of which explains why President Joe Biden floated the idea in his State of the Union speech in March of providing tax credits to potential homebuyers to help offset the highest mortgage rates in a generation. And also why the New York Times reported last week that some Democrats are urging Biden to take a page from Donald Trump’s playbook and attempt to bully the Federal Reserve into lowering interest rates.

In theory, these ideas sound great — they would presumably put homes within reach of more households and boost transactions. In practice, they would be a disaster. It’s even likely that the unintended effect would be making housing less affordable by pushing up mortgage rates and home prices.

Most all the data show that the problems with the housing market these days have little to do with demand. Sure, measures of housing affordability are near record lows, but the median price of existing homes has risen 8.2% to $393,500 since the Fed started raising policy rates in February 2022. Not only that, but at around 30, the number of days a home sits on the market before being sold is the same as it was in 2019 when mortgage rates were around 4%, instead of the current 7.50%, according to the National Association of Realtors. The percentage of first-time buyers is also similar at about 30%. But perhaps what is most remarkable is that the realtors group says 29% of homes sold above asking price in March!

As for Biden’s proposal to provide tax credits in the amount of $5,000 a year for two years to first-time middle-class buyers and $10,000 to “middle-class families who sell their starter homes,” the amounts are really too small to incite buyers to pull the trigger or potential sellers to list, let alone move the needle on affordability. Plus, it would only underpin house prices at a time when many potential buyers say prices are too high anyway.

Still, tax credits are more pragmatic than browbeating the Fed into cutting rates, which shows a fundamental misunderstanding in how rates work. The only rate that the central bank has direct control over is the target federal funds rate, which is the rate banks charge each other for overnight loans. This rose from 0.25% in February 2022 to 5.5% in July 2023, where it has remained as part of the Fed’s effort to tighten credit conditions enough to slow inflation.

Although the fed funds rate does influence what happens with other rates, there is no direct one-for-one effect. Mortgage rates are tied to those on US Treasury notes and bonds and debt securities backed by home loans. Those rates are mostly determined by investors’ outlook for economic growth and inflation rather than where the fed funds rate is (which partly explains why the yield on the benchmark 10-year Treasury note is currently around one percentage point lower than the fed funds rate).

Therein lies the problem with attempting to bully the Fed into lowering the fed funds rate. If by some remote chance that were to happen before inflation was brought under control, Treasury yields would likely rise on speculation that the Fed’s looser monetary policy would spark even faster inflation.1 As a result, mortgage rates would rise in tandem, exacerbating the perceived lack of affordability. Even if mortgage rates did fall, pent-up demand would likely end up pushing prices higher. So, that idea should be shelved.

The real issue with housing is the lack of supply. Many homeowners don’t want to sell — a record 39% of homes have no mortgage and more than 60% of owners with loans have locked in rates below 4%. The number of homes actively listed for sale has plummeted from a peak of around 4 million in 2007 to some 1 million currently. This is despite the number of households in the US having risen by more than 10 million, according to the US Census Bureau. And, as the data for days on the market before being sold show, quality houses that do come up for sale are quickly purchased.

There’s really only two ways to fix the housing crisis, and neither is a solution that can be achieved quickly, let alone before the elections. The first is to spark new housing supply with some combination of tax credits or similar incentives for builders and sellers of developable land, and changes to zoning laws. By some estimates, the US needs an extra 3.2 million homes to meet demand.

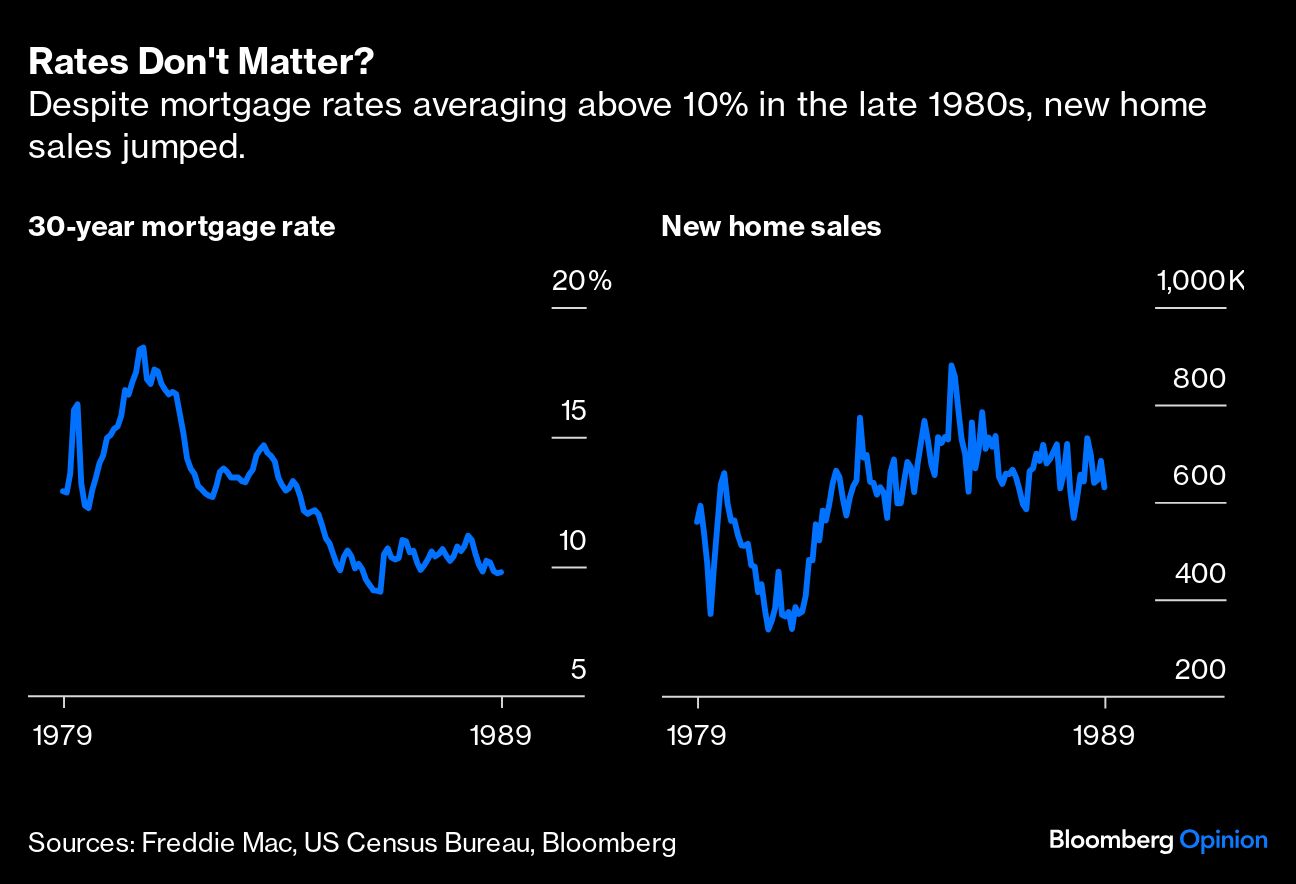

The second is to find a way to bolster consumer confidence. The late Bob Toll, the founder of homebuilder Toll Brothers Inc., was often asked how his business would respond to rising borrowing costs. His standard response was to point to the late 1980s, a period when the housing market was booming even though mortgage rates were consistently above 10%. And he was right. New home sales reached a record in 1986. His explanation was that when it came to buying a home, confidence among consumers was more important than the level of rates.

The solution to the US housing crisis lies not in demand but in supply, and any solution that attempts to stimulate buyers via additional financial incentives risks ruining the dream of owning a home for millions of Americans.

1 Longer-maturity debt tends to get hit the worst when inflation accelerates because rising consumer prices erode the value of a bond’s fixed payments over time. That’s why investors demand higher yields at the first sign of inflation, causing the yield curve to widen.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Robert Burgess