Today’s Tips:

- Liquidity will help keep risk markets afloat, at least until the US election;

- Yes, first-quarter earnings beat expectations;

- That’s largely because of wider profit margins; are they sustainable?

- AND: It’s 70 years since someone first ran a mile in 4 minutes — it’s all about teamwork.

Earnings Breeze

The breeze of this earnings season has been near perfect. First-quarter earnings, now published by 80% plus of the S&P 500’s members, put the index’s profits on course for their strongest growth since the second quarter of 2022, when higher inflation and higher rates began to bite. Nvidia Corp., the artificial intelligence poster child, is still to be announced but all the other members of the so-called Magnificent Seven — Alphabet Inc., Amazon.com Inc., Apple Inc., Meta Platforms Inc., Microsoft Corp., and Tesla Inc. — have published.

The Seven’s performance propelled the index despite setbacks from Tesla and Meta Platforms. Their earnings, including estimates for Nvidia, are expected to top 49% growth, far outstripping the nearly 14% in the same period last year. Yet another resolute showing brings to sharp focus the degree of corporate concentration, which is not unique to the US market.

How did they do this? Companies’ margins in the US and other markets, excluding China, defied the high-interest rate environment. As Societe Generale’s Andrew Lapthorne argues, investors don’t seem concerned about higher interest rates’ impact on balance sheets, in large part:

This is because large cap balance sheets don’t have much leverage in the first place and debt rolls over slowly given a lot of it is fixed, meaning it takes a while to incorporate higher interest rates into the system. One notable exception is small businesses: more floating debt and higher leverage mean strong balance sheet stocks are outperforming the weak.

As seen in the following chart from Deutsche Bank AG, the strong margins ring through nearly all global markets:

It’s possible to put a negative political spin on this. Growing profitability on this scale might provoke a populist reaction. But the Magnificents’ strong showing does, however, appear to be running out of steam — or at least the “other 493” companies are strengthening. In the future, Bank of America Corp.’s analysts expect Mag Seven earnings to slow, while everyone else’s profits should accelerate. Given the high correlation between tech’s outperformance in stocks and earnings, the narrowing growth differential is expected to help the market to broaden out:

Earnings tend to come in ahead of expectations, thanks to the dark arts of investor relations departments. In the last 10 years, an average of 74% of companies reported EPS above estimates — and this season it’s 77%. While this quarter is on track to show a strong EPS beat, cracks in the economy’s durability have investors questioning earnings’ stability. Should they cut their EPS forecast for Q2? Probably not. Instead, FactSet’s John Butters points out analysts are expecting higher earnings for the current quarter, which is very unusual:

In a typical quarter, analysts usually reduce earnings estimates during the first month. During the past five years, the average decline in the bottom-up EPS estimate during the first month of a quarter has been 1.9%. During the past ten years, the average decline in the bottom-up EPS estimate during the first month of a quarter has been 1.8%.

As this SocGen chart shows, EPS growth for 2025 across all sectors globally is expected to build on this year’s strong performance:

Meanwhile, revenue growth has been in line with expectations, although the share of companies that beat estimates, 61%, is below the 10-year average of 64%. Regardless, the S&P 500’s 4.1% actual revenue growth rate makes it the index’s 14th consecutive quarter of growth:

With about 100 companies yet to announce results, Nvidia’s announcement, due on May 22, is by far the most anticipated, as it will offer a proxy to gauge the path toward widespread adoption of artificial intelligence. Barring major surprises there, however, the S&P 500 has delivered what shareholders wanted, which is continuing buoyant growth in profits.

-- Richard Abbey

Liquidity, Liquidity Everywhere, But Never a Drop to Drink…

If money is anywhere, it has to go somewhere. That’s the intuition behind the phalanx of investors who watch liquidity — changes in the amount of money in circulation that could swiftly be deployed. As money is fungible and can easily cross most international boundaries these days, it’s also global. The subject is counterintuitive, maddeningly technical, and hard to define, but it matters. The last few weeks have seen flow and counter-flow. Here is a summary of what you need to know:

-

Taxation Flows

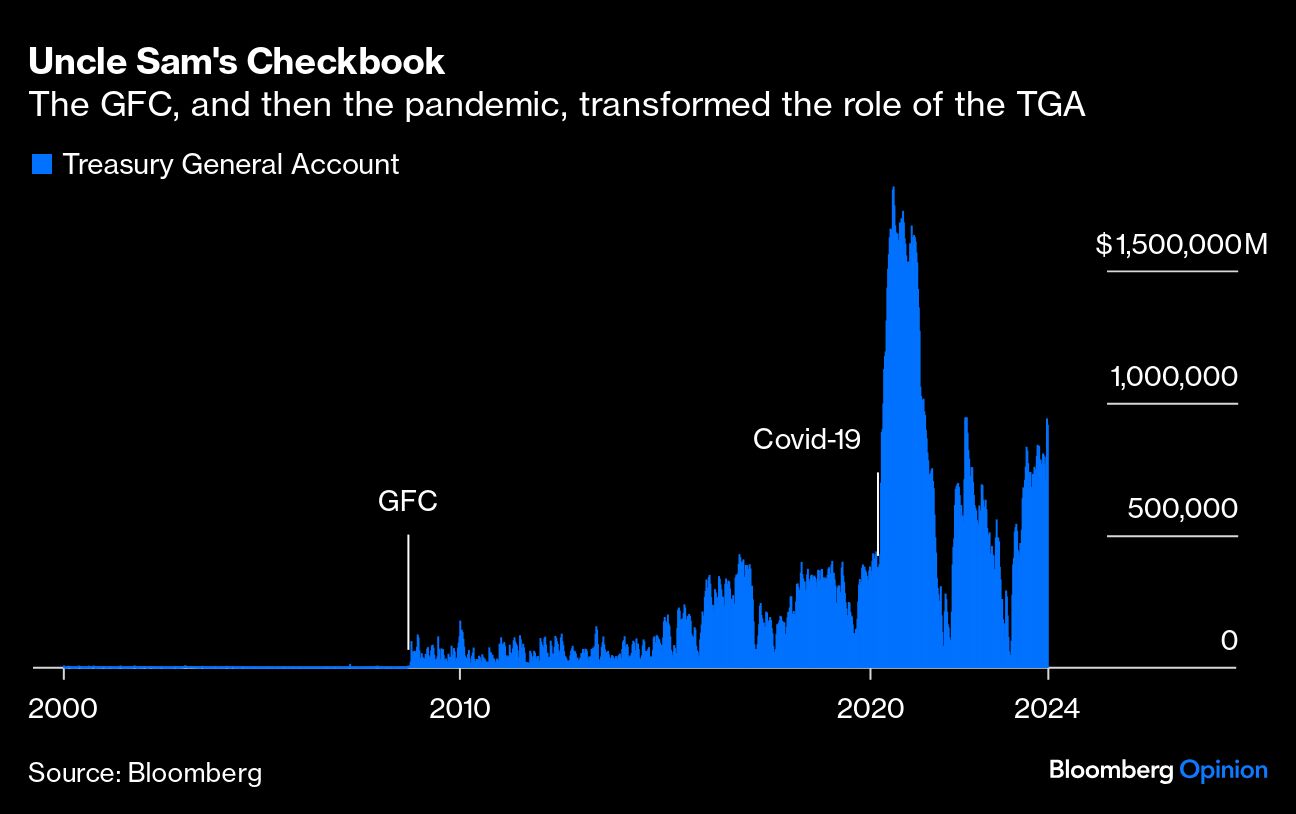

Tax payments in the US tend to be bunched ahead of the Tax Day in the middle of April. Paying taxes makes consumers and their bank accounts less liquid (to put it technically), and the money transfers to Treasury Department’s general account (known as the TGA). One reason the US stock market hit an air pocket last month was, almost certainly, the need for people to pay their taxes, which swelled the government’s holdings by some $191.8 billion. That brings us to…

-

The TGA

Higher balances in the TGA mean lower liquidity. A rising TGA takes liquidity out of the system, while a decline indicates that cash is returning to people who can then deploy it. This is not (as a rule) meant as any kind of a monetary policy tool. One reason that it has mattered more since the Global Financial Crisis is the advent of regular cliffhangers over whether Congress will raise the federal government’s borrowing limit. If the Treasury secretary gets it right, the TGA will be high entering the period of fraught negotiations, and that means there is no need for the government to raise new debt; it simply spends the money sitting in the TGA, and adds liquidity to the system in the process.

Like a checking account, the TGA can vary dramatically, and in the last four years it has twice been drawn down (boosting liquidity in the process) to give the government more time to thrash out a deal with Congress on the debt limit. After swelling in April, the plan is that it will expand by only another $100 billion by the end of September — more than offset by changes by the Fed.

-

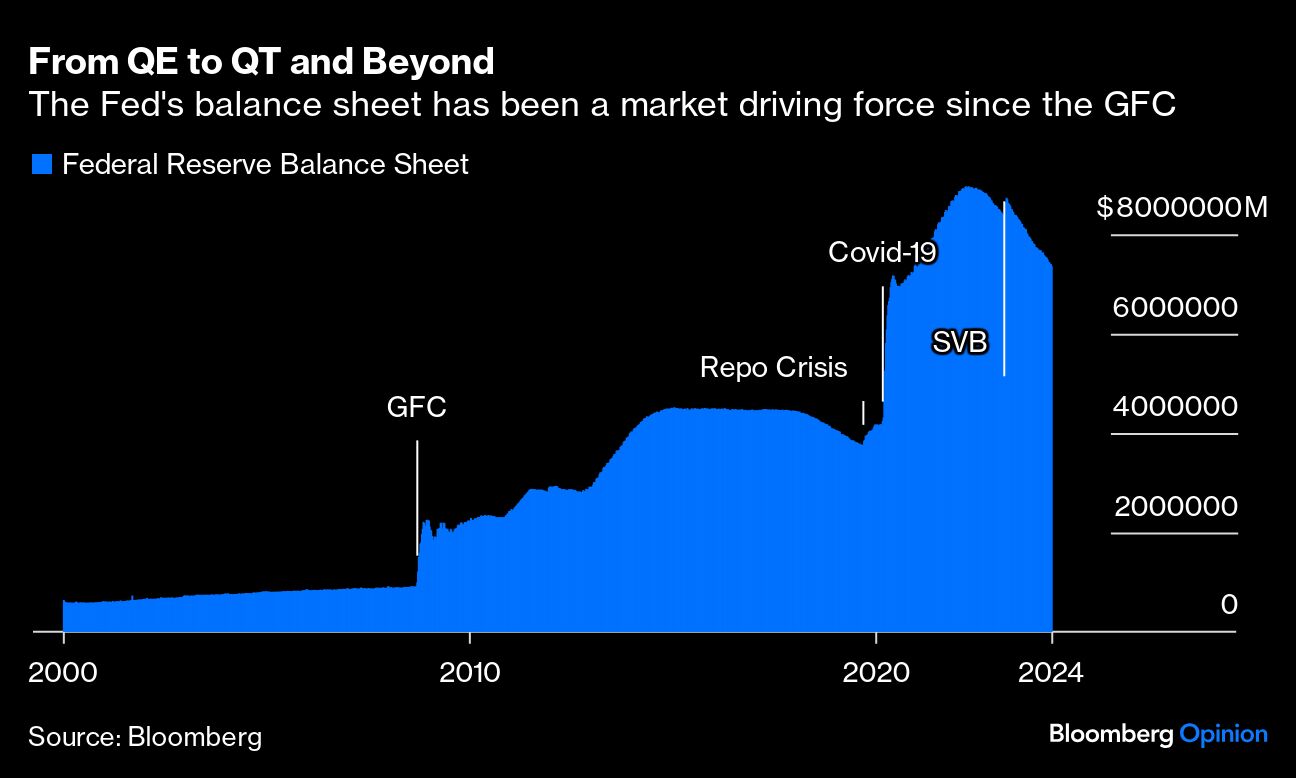

QT (or QE)

Quantitative Tightening refers to the Fed’s manipulation of its balance sheet, in which keeps the bonds it has previously bought as part of QE (Quantitative Easing). When a bond is bought via QE, that means the ultimate investor is made liquid, receiving cash in return for the bond they’ve just sold to the Fed. A growing Fed balance sheet is therefore an indicator of burgeoning liquidity, with more money in the system available to buy stocks or bonds. QT, in theory, means the opposite. It effectively tightens monetary policy.

The Fed has been in QT mode for a while now, as the chart demonstrates. The one true surprise from the Federal Open Markets Committee meeting last week came with the announcement that it would taper monthly QT purchases by more than had expected, reducing them from the current $60 billion to $25 billion, rather than the predicted $30 billion.

-

Treasury Re-funding

The US Treasury needs to borrow to finance the government deficit. If it does this by selling long-dated bonds (coupon issuance in the jargon), that ties up investors’ money and reduces liquidity. If they choose to issue short-term bills instead, that keeps markets far more liquid. For the last year, the Treasury has chosen to borrow much more than it usually would in short-term bills, and thereby maintain liquidity. Last week’s Quarterly Refunding Announcement continued the policy.

This chart from Oxford Economics shows that the effects shouldn’t be overstated, as the total volume of long-dated bonds being auctioned is historically high. But the Treasury’s maneuvers have helped avoid much higher supply of bonds, which could have had a more severe impact on liquidity. Also, note that the much smaller auctions in 2020 and early 2021, when 10-year yields were below 1%, now look like a missed opportunity. The chance to lock in rates that low is unlikely to return for a while:

In sum, Dan Clifton of Strategas Research Partners suggests that last week’s decisions by Jerome Powell and Janet Yellen will mean $273 billion of more of net liquidity by the end of September than previously expected. This can be viewed as an attempt to prime the economy for the election, and many indeed look at it that way. It can also be viewed as a conservative attempt to avoid a crisis. Previous periods of QT were reversed by the repo market crisis of September 2019, and then by the regional banking crisis driven by Silicon Valley Bank in March last year.

Given that the Fed might just have been able to justify starting to cut rates in March, which is what the market expected and what many thought they should do, it is hard for me to brand all of this as politically motivated. I tend to agree with Will Denyer of Gavekal:

Although Powell was slow to respond to the initial pick-up in inflation, everything he has done in the last two years indicates he is committed to the 2% target, including his recent statements as inflation has picked up again. When his term ends in May 2026, there is a risk Powell could be replaced by a political lackey. Until then, the Fed can be regarded as credible.

Whatever the motivations of Yellen and Powell, however, the bottom line is that they are determined not to allow illiquidity to drive a crisis (or possibly even an equity downturn) over the six months between now and the presidential election.

Survival Tips

It was 70 years ago. On May 6, 1954, a 25-year-old medical student called Roger Bannister became the first human to run a mile in under four minutes, in a student track meet in the outskirts of Oxford in front of a crowd of 3,000. It was a team effort by amateur scholar-athletes. His friends Chris Brasher (who went on to win an Olympic gold medal and became a distinguished sports journalist) and Christopher Chataway (who later broke the world 5,000 meter record, worked as a television newscaster, and served as an MP and government minister), took turns to set the pace. Bannister ran the last lap on his own, with only the clock for competition; he went on to a long career as a neurologist, and as the head of an Oxford college.

Since then, 1,663 people have run faster, but there’s something mystical about round numbers, and the 4-minute mile had been thought unattainable. Bannister and friends had real jobs to do, and didn’t have the equipment or nutritional advice that has helped chisel away much further at the record since then. No wonder modern athletes can run faster.

That said, the current recordholder deserves more credit. Bannister held the record for about a month, until it was beaten by the Australian John Landy (who disapproved of using pacemakers). It’s now almost 25 years since the record was last broken. Here it is, being set by the Moroccan Hicham El Guerrouj in Rome in 1999. He covered the distance 18 seconds quicker than Bannister did, but outside the track and field community he is far less famous. Googling revealed 200,000 results for El Guerrouj, and about 4 million for Bannister. Like his predecessor, El Guerrouj benefited from two pacemakers. What I didn’t know was that El Guerrouj was spurred by Noah Ngeny, a 20-year-old Kenyan, who tore up the script by racing him all the way to finish. Both El Guerrouj and Ngeny beat the previous record; nobody has matched Ngeny’s time since. There’s inspiration in the glorious amateurism and teamwork of Bannister, Brasher and Chataway; we can also learn from the competitiveness and professionalism of El Guerrouj and Ngeny.

A message from Advisor Perspectives and VettaFi: Dive into alternative investment opportunities at our upcoming Alternatives Symposium on May 30th, and gain insights into diversifying portfolios beyond traditional equities and fixed income.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.