The Inflation Battle Is Far From Over

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsToday’s Points

- US April CPI could have been much worse, so stocks rallied to all-time highs;

- It also could have been much better, so treat the rally with caution;

- Real retail sales are back down to their post-financial crisis trend;

- King Dollar hasn’t abdicated, but he’s looking a bit weaker;

- AND Great news on presidential debates; they’re reliably compelling.

Calmer on the Inflation Front

There was white smoke over the Bureau of Labor Statistics, sort of, on Wednesday morning. The key measures of consumer price inflation for April confirmed expectations for a slight decline, and alleviated growing anxiety over a possible reacceleration. Risk assets across the world spent the rest of the day exhaling deeply.

The numbers could easily have been worse, and after a month in which prices had discounted growing risks of inflation the direction of travel on markets made total sense. Plainly bond yields should come down a little in these circumstances, while equities are reinforced. It is, however, reasonable to question whether these numbers were any kind of a turning point in the battle against inflation.

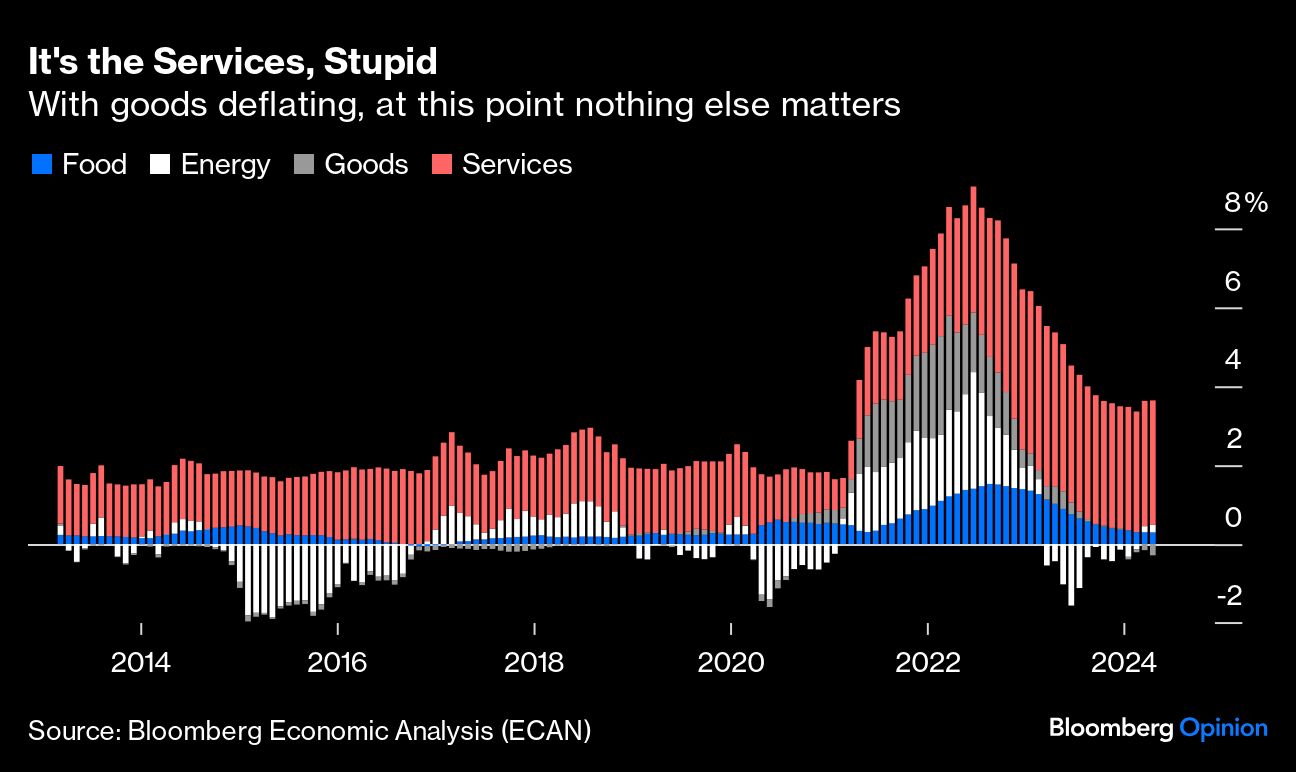

To start, this beautiful chart generated by Bloomberg Economic Analysis breaks CPI into four major components; food, fuel, other goods, and other services. Two years ago there were major shocks to the prices of goods, food and energy, all of which have now dissipated. That’s why inflation is much lower now. The problem is that services inflation remains stubbornly high, and accounts for substantially all of headline inflation at this point:

Services are people-heavy businesses in which wages are crucial drivers of prices. Unlike with food and fuel, monetary policy can be an effective counter to wage inflation, so this is an incentive for the Federal Reserve to keep rates where they are.

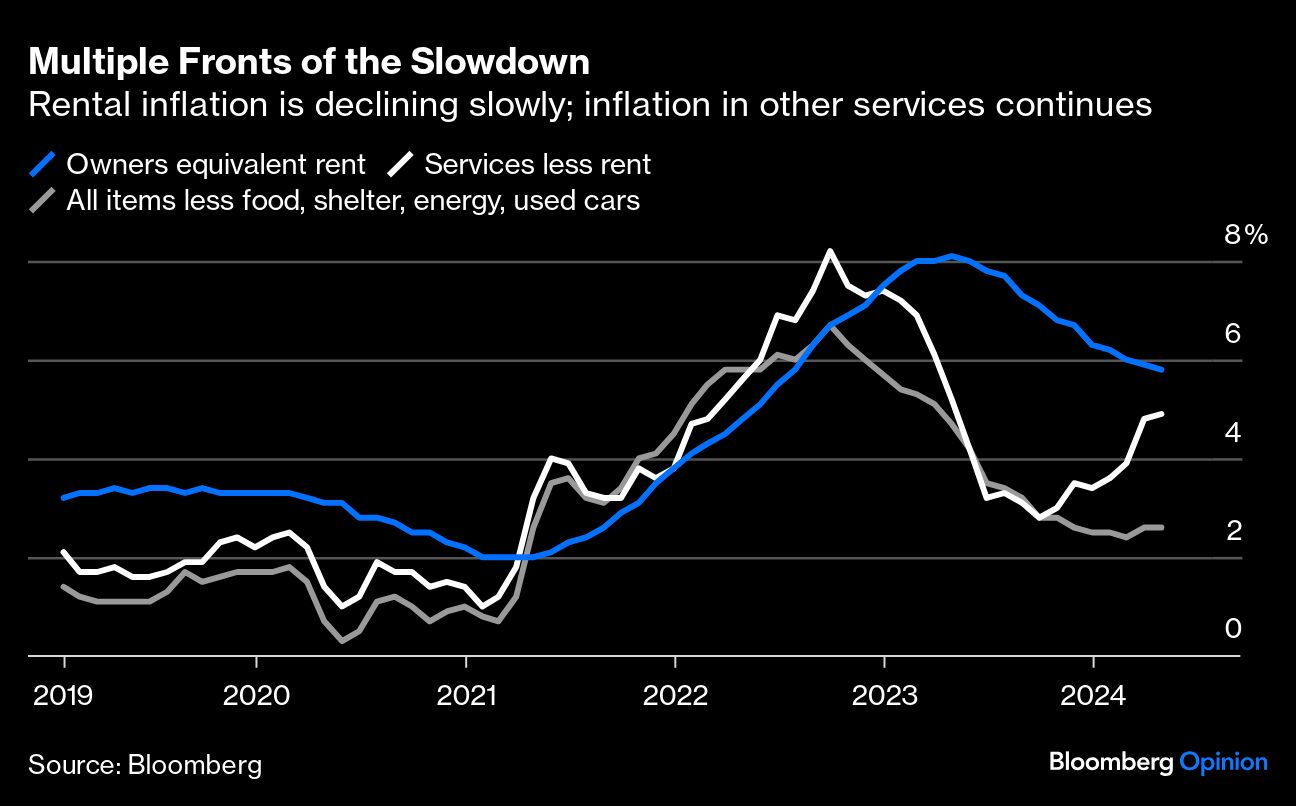

Breaking this down further, the following chart shows inflation for owner’s equivalent rent (a highly contentious measure of shelter cost), and for two measures that were rarely cited before this surge in prices began, but which are now at the center of the debate. One is so-called “supercore” inflation, which measures services excluding shelter, and which the Fed regards as important, and CPI excluding food, shelter, energy and used cars. Most people do need to buy all of these things, but the Bureau of Labor Statistics began printing this number in 2021 at a point when inflationary pressure was concentrated in those items. This is what they look like:

There’s an argument that rent inflation would be coming down quicker if it were better measured, which Points of Return has discussed in the past. The official data show it declining, but painfully slowly. The Stepford measure of inflation, excluding everything that people wanted to exclude in 2021, is far below its peak but it has irritatingly tipped up recently without ever getting down to the target of 2%. We can’t blame the entire resurgence of inflation pressure on these items alone.

Most disquietingly, supercore is on a continuing rising trend. It’s near 5%, and far above any level with which the central bank can be comfortable. It turned upward last fall (coincidentally or otherwise, when Federal Reserve Chair Jerome Powell executed his infamous “pivot” toward reducing rates) and its rise continues. Viewed on a month-on-month basis, supercore rose less in April than it had in the three preceding months of the year, but it still looks historically high. This alone more or less rules out a rate cut as early as next month:

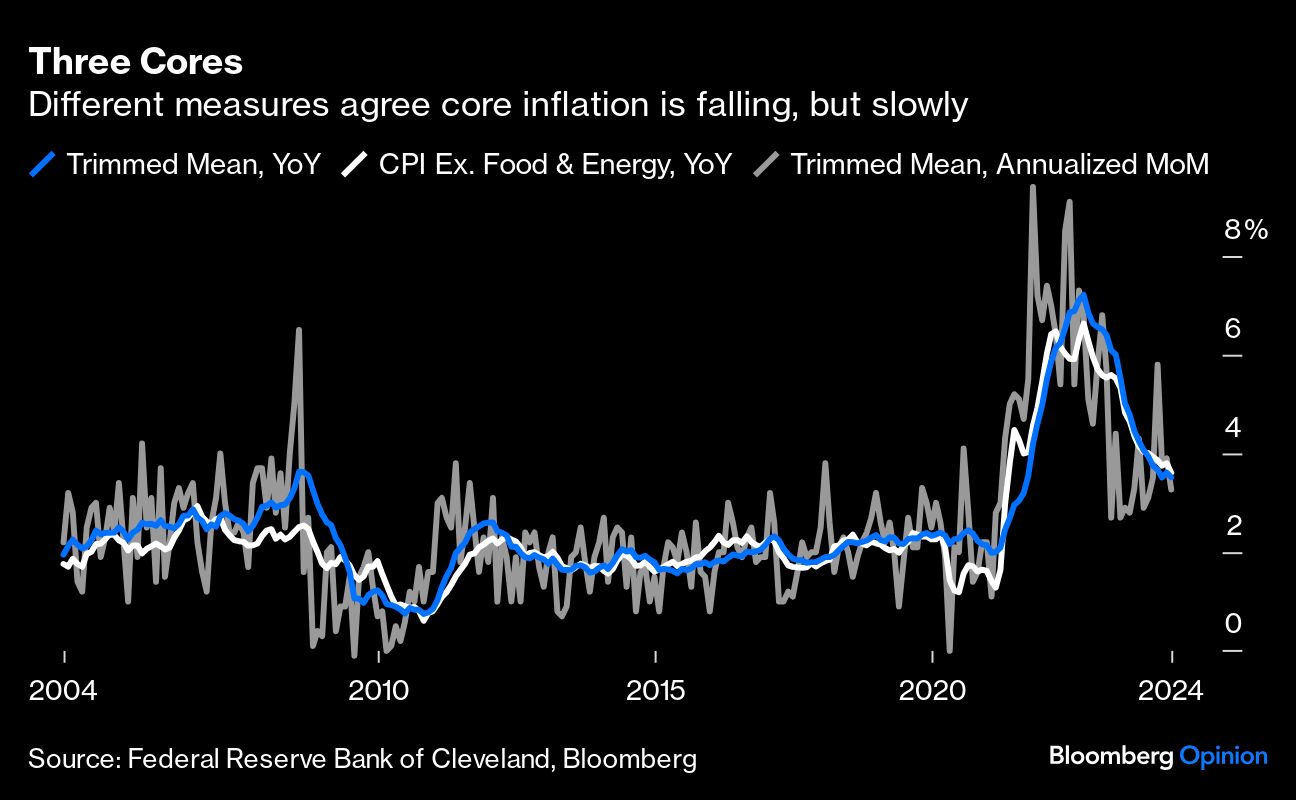

This pattern repeats in the various statistical measures prepared by different research groups at the Fed. The Cleveland Fed’s trimmed mean measure excludes the biggest outliers in either direction and takes the average of the rest. Having risen higher than CPI excluding food and energy, the usual definition of “core” inflation, it’s now at much the same level. The month-on-month number confirms a decline. This measure remains high for the Fed’s liking, but it’s plainly trending downward:

That trend is confirmed by the Atlanta Fed’s sticky price index, which concentrates on goods and services whose prices take a while to change and seldom fall. This is seen as inflation that’s particularly difficult to reverse, and so any rise will make the central bank uncomfortable. It is coming down, but very slowly, and it remains above 4%:

Taken together these confirm that disinflation is still happening while there is no sign of an outright acceleration. So rate hikes look very unlikely. But cuts in the near term can also be ruled out as several key measures are sticky and remain too high.

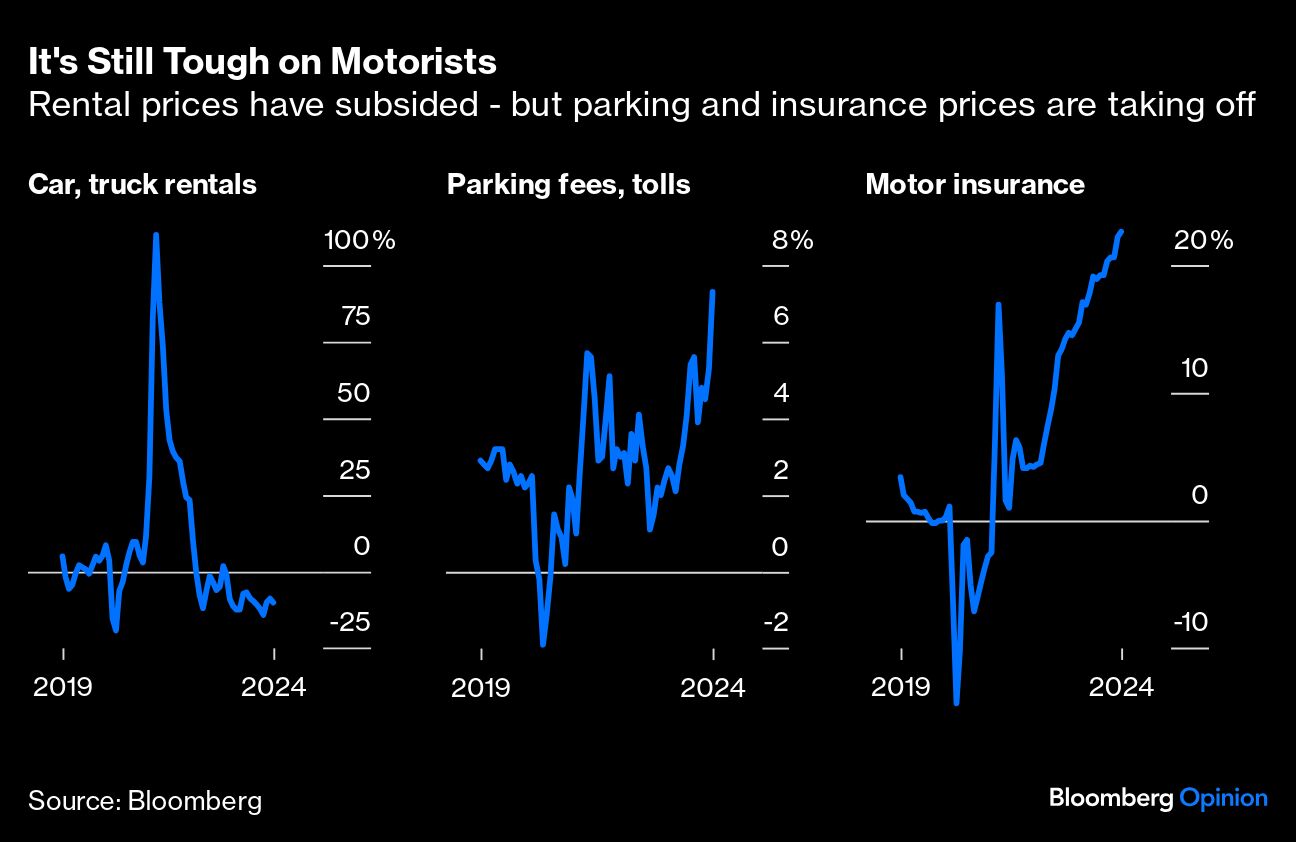

Also, some of the weirdnesses created by supply interruptions during the pandemic persist. Car rental inflation at one point topped 100%; it’s now running at minus 10%. However, the knock-on effects on other costs borne by motorists persist. Parking fee inflation is now above 7% while car insurance costs are above 20% and rising:

What About Rates?

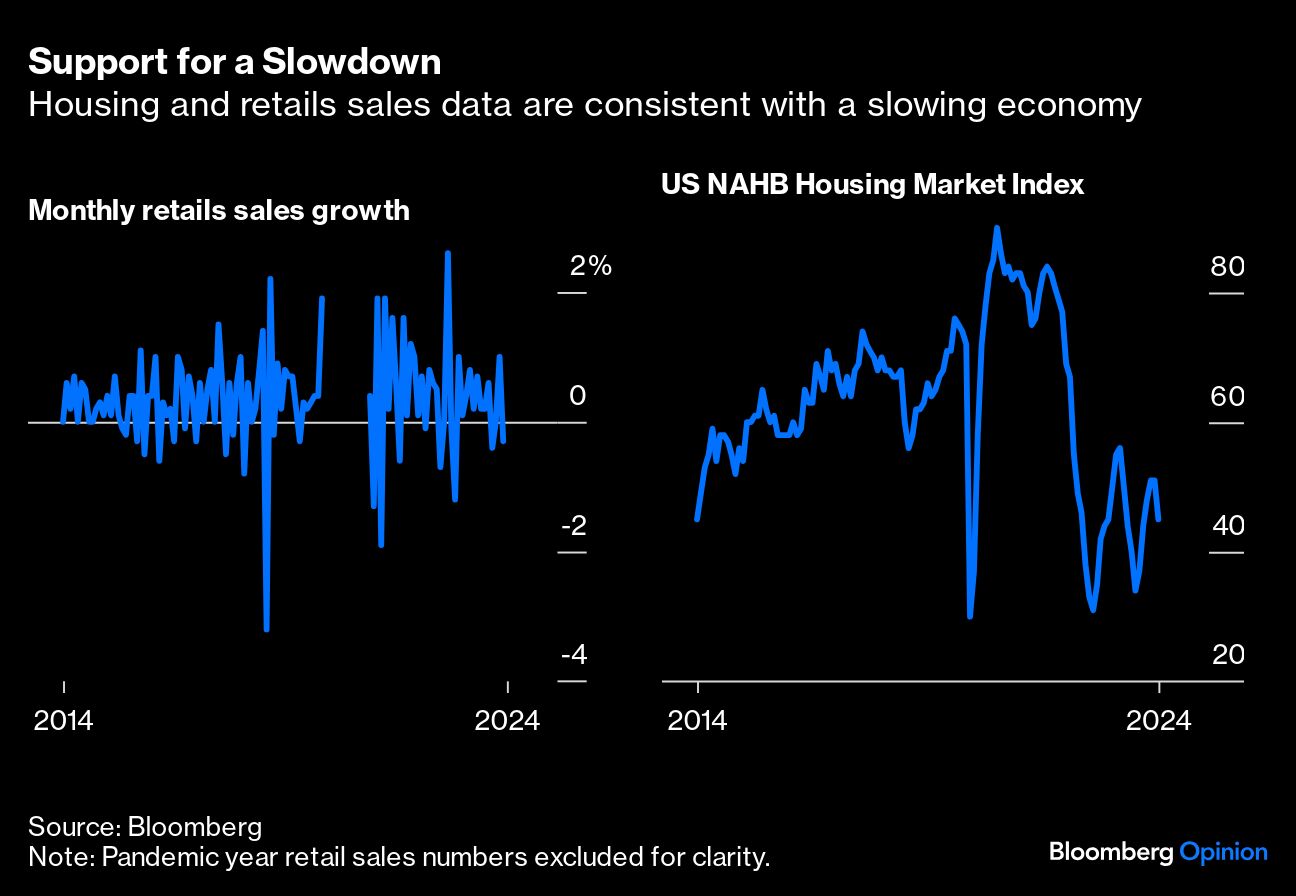

Markets tend to view inflation through the lens of the implications for the Federal Reserve and interest rates. On that front, other economic data suggested rate cuts might soon be justified, with retail sales growth slipping after starting the year strong, and the National Association of Home Builders’ monthly survey showing that sentiment in the housing industry was turning negative again:

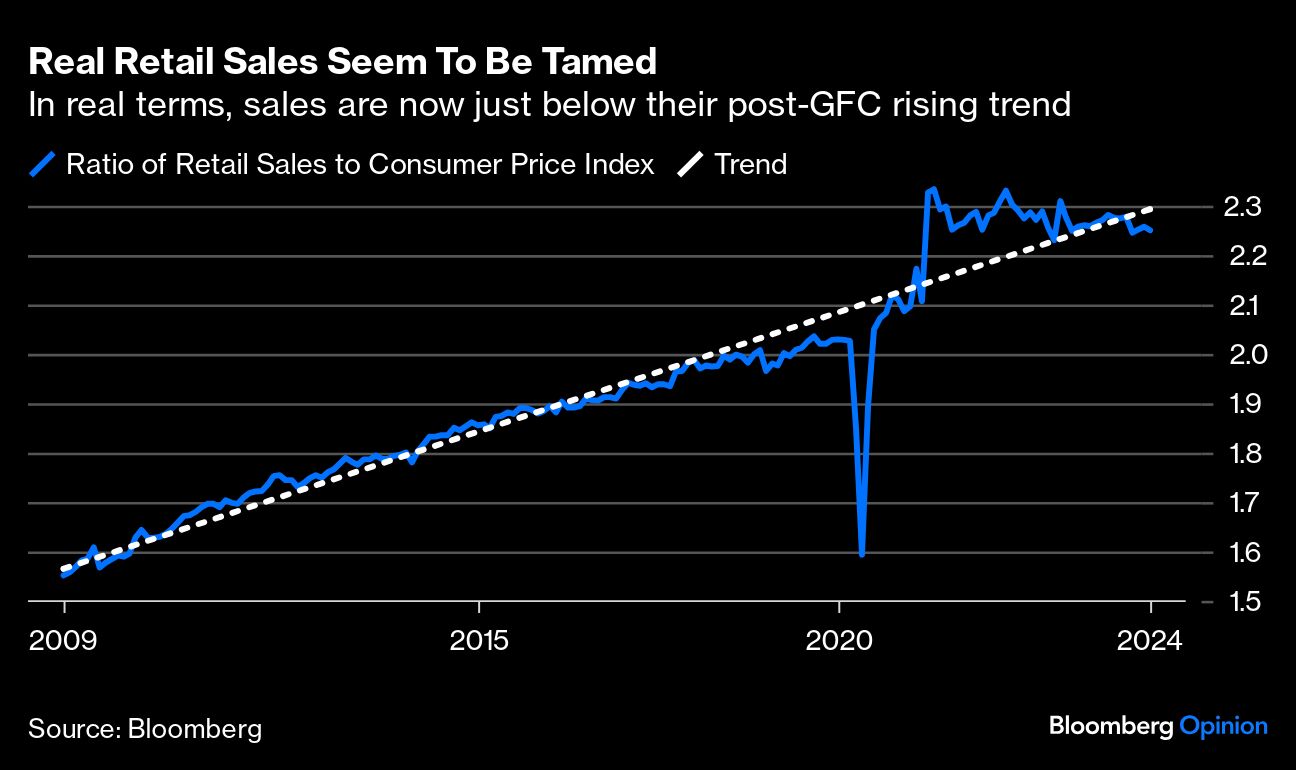

On retail sales, Troy Ludtka of SMBC Nikko also points out that in real terms (dividing total sales by the consumer price index), they have now fallen back to, or even slightly below, the rising trend that was in force between the global financial crisis and the pandemic. Any evidence of a tiring consumer helps the case for rate cuts:

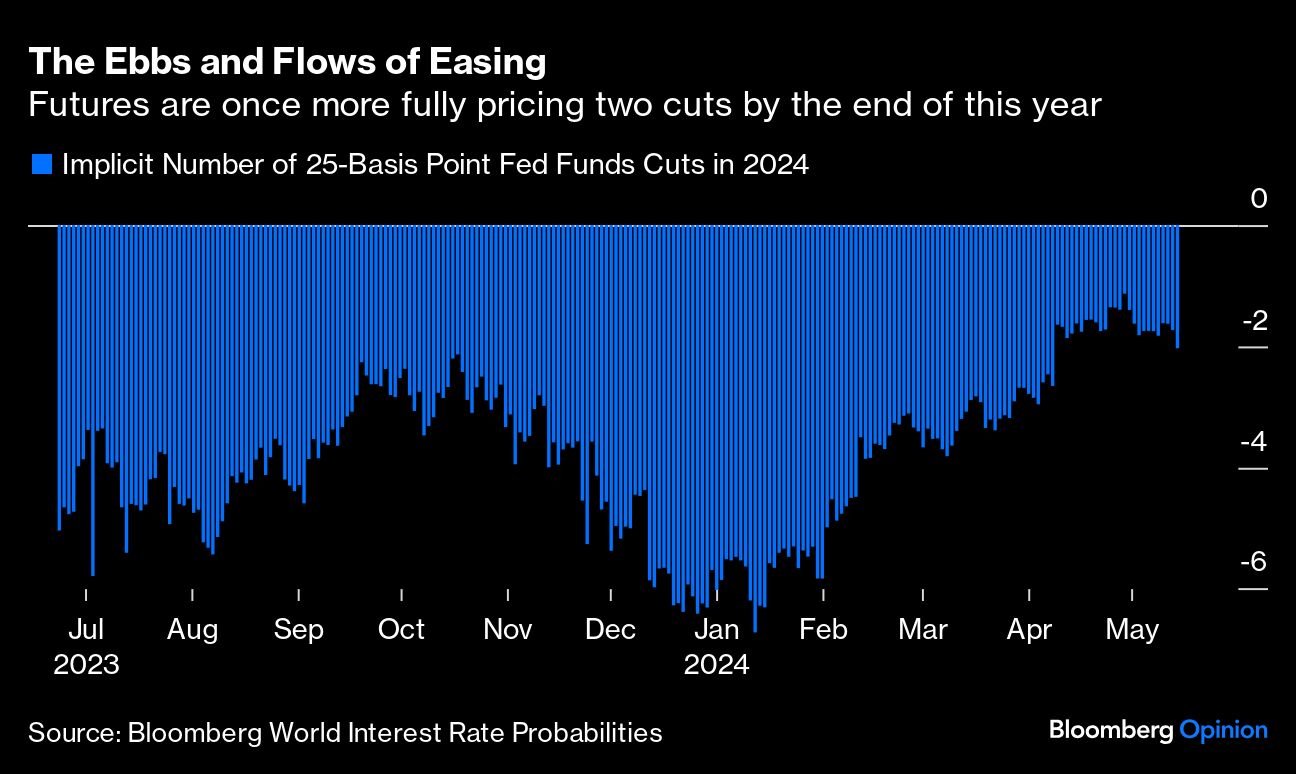

However, the effect on implicit fed funds rates in the futures market was subdued. Cuts are out of the question for June, almost everyone agrees, and very unlikely in July. But the fed funds futures market is now back to fully pricing in two cuts of 25 basis points each by the end of the year:

This is still far short of the radical easing that was expected back in January, but it was enough to persuade investors back into buying bonds. Most notably, the benchmark 10-year Treasury yield, very directly affected by rate forecasts, is now back in line with trends. Only a few weeks ago a breakout beyond 5% had seemed a real possibility, so this is a relief to many:

As for stock markets, the good news on lower rates faced up against the bad news that the economy really is slowing down — and the rates argument won out. The S&P 500 hit its first all-time high since March, while FTSE’s index for the rest of the world is now at its highest since early 2022. Both have fully recovered from last month’s sell-off, which really wasn’t a correction:

The Magnificent Seven internet platform stocks also hit a new record, while the long-anticipated resurgence for cheap value stocks relative to growth continues not to materialize:

Markets have momentum, and should be safe from any big shocks on rates for a week or two, so in the short term it’s fair to expect the rally to trundle on for longer. The weaker dollar (of which more below) also helps salve worries. In the longer term, recent events are consistent with two narratives. Inflation remains too high as the economy slows down, pointing to an eventual hard landing; and inflation is slowing gently without halting economic growth, producing a Goldilocks outcome. Neither can be ruled out.

Weak Dollar Buys Time

US inflation cooling is music in the ears of central bankers around the world who have been having to deal with the dollar's strength. Already selling off in expectation of cooler inflation, the actual print piled on the greenback’s pressure. Higher US rates have constrained other central banks from reducing their interest rates even when their economies plainly need it; things look healthier now.

That showed in the strength of their currencies relative to the dollar after the inflation data. Expectations of imminent rate cuts from the European Central Bank and Bank of England got a boost as their currencies gained, as shown in the chart below, while the yen is on course to benefit from the much-needed cushion:

Historically, it has made sense for central banks to follow the path of the Fed’s easing cycle — the only exception being 1998. Following recent cuts by the Riksbank, Sweden’s central bank and Swiss National Bank, this year is bucking the trend, with the Fed taking a backseat. In all of these instances, central bankers jumping ahead of the Fed were able to do so after disarming inflation and also in response to the stifling of economic growth, but even then downside risk to local currencies was a huge factor. It remains in other central banks’ interest not to stray too far from the Fed. As shown in this Ned Davis Research chart, central banks have taken matters into their own hands when necessary:

With rate cut optimism returning in the US, the prospects that the European Central Bank and Bank of England will cut ahead of the Fed are growing. After all, their battle against inflation has been more successful than that of their cross-Atlantic counterparts. The Bloomberg World Interest Rate Projection function is pricing a first cut for the United Kingdom in August, while Frankfurt could cut as early as June.

It will be interesting to see the extent to which these banks will go to rescue their economies without turning the heat on their currencies. Ned Davis Research analysts made a similar observation:

Most major central banks work in their self-interest. One often sees synchronization in central bank cycles because growth and inflation patterns tend to move in tandem due to globalization. This time, the main cause of the US’s higher inflation is country-specific.

The risk of a resurgence in European inflation remains. SMBC Nikko Securities’ Joseph Lavorgna doubts if the ECB will take the bait:

Maybe they can cut once, but it seems to me that if the Fed isn’t cutting, it’s going to be much harder for the ECB to cut, especially with the possibility that the dollar can strengthen significantly versus the euro and complicate the inflation situation in Europe. I think the ECB might be more constrained than people think.

So far, nothing has broken, and the chances that it will stay that way seem to have improved. But that still depends on inflation in the US.

-- Richard Abbey

Survival Tips

It looks like we do indeed have some presidential debates to look forward to after all, and they should even start much earlier than usual, in June. The debates can be great entertainment. It’s questionable whether they really enlighten voters on what the candidates would do in office, but they’re often startlingly revealing of personalities. They also make great material for Saturday Night Live, which tends to zoom in mercilessly on those personality traits. My personal favorite is their version of the first debate of 2000 between Al Gore and George W. Bush. W did indeed come across as an airhead, while Gore appeared insufferable. The skit on the third debate that year lampooned the notion of holding debates in front of undecided voters, and also featured an appearance by Dana Carvey as George H.W. Bush.

Then there was Jason Sudeikis vs. Tina Fey replicating the 2008 vice presidential debate between Joe Biden and Sarah Palin, Jon Lovitz capturing Michael Dukakis (who came over as a cold fish) in his 1988 debate against George H. W. Bush, and Alec Baldwin and Kate McKinnon skewering almost everything people didn’t like about Donald Trump and Hillary Clinton in 2016. That’s entertainment! True, the first time Trump (who tested positive for Covid days later) and Biden debated each other in 2020, was a car crash. But hope stays.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All