Everyone is worried about the excessively high level of US government debt. Everyone, that is, except America’s creditors.

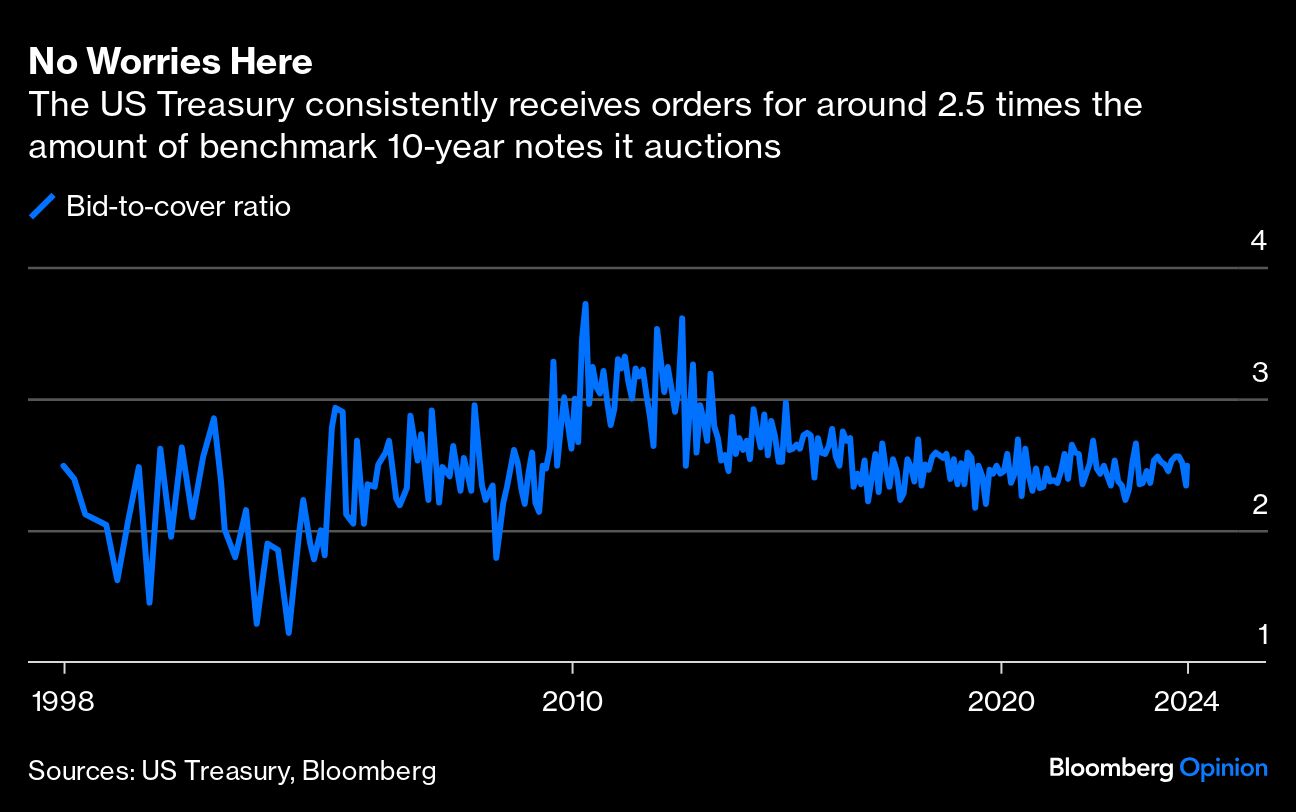

Take last week’s quarterly refunding by the US government. The US Treasury Department auctioned $125 billion of three-, 10- and 30-year bonds. Investors submitted bids for about 2.5 times the amount offered at each of the auctions, which was slightly above the average going back to early 2020 when the government ramped up its borrowing to support the economy through the Covid-19 pandemic. When it comes to the benchmark Treasury, that’s even higher than the average during the late 1990s and early 2000s when the US was running budget surpluses!

There are two primary explanations for why investors continue to clamor for US government debt despite federal borrowing having soared to $34.6 trillion, or around 120% of gross domestic product, from $23 trillion, or 106%, at the start of 2020. Each on their own should be enough to redirect the conversation about how much debt is too much. But taken together they paint a far less dire picture of US government finances than suggested by fiscal hawks.

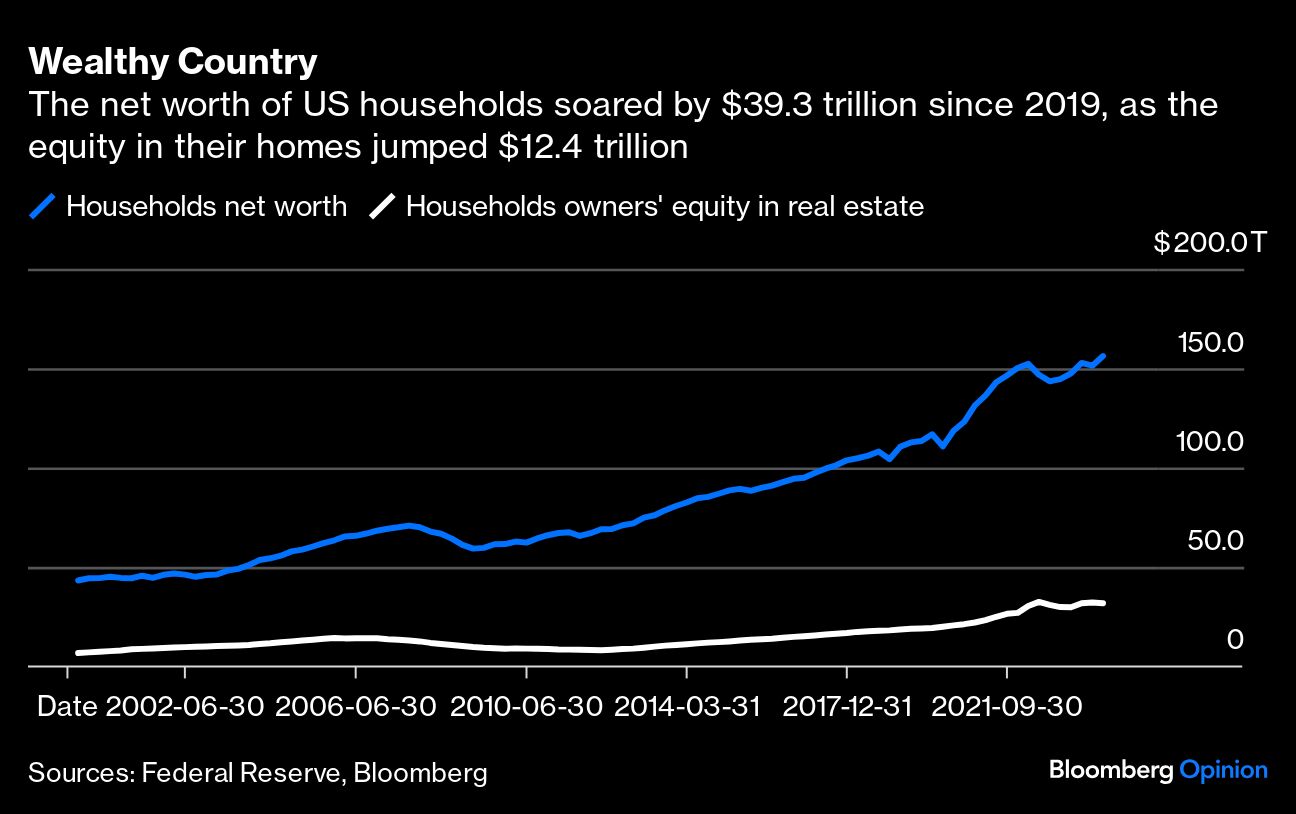

First, the discussion about US borrowing is always too narrow. Sure, government debt has soared as a percentage of GDP, but the US economy overall has de-levered since the finance crisis of 2008. Households, businesses and financial institutions have all significantly shrunk their liabilities, so much so that American debt overall has fallen to 334% of GDP from the peak of 368% in 2009, according to the economists at Wells Fargo & Co. Heck, a record 39% of US homes have no mortgage! Renaissance Investment Management recently took a deep dive into America’s “balance sheet” and concluded that America has a net worth of $116.6 trillion, including the value of everything from real estate and securities to cash less all private and public debt. That is up from $102.9 trillion at the end of 2019. This is what the bond market knows — that America is an extremely wealthy country with the capacity to easily finance government debt and deficits.

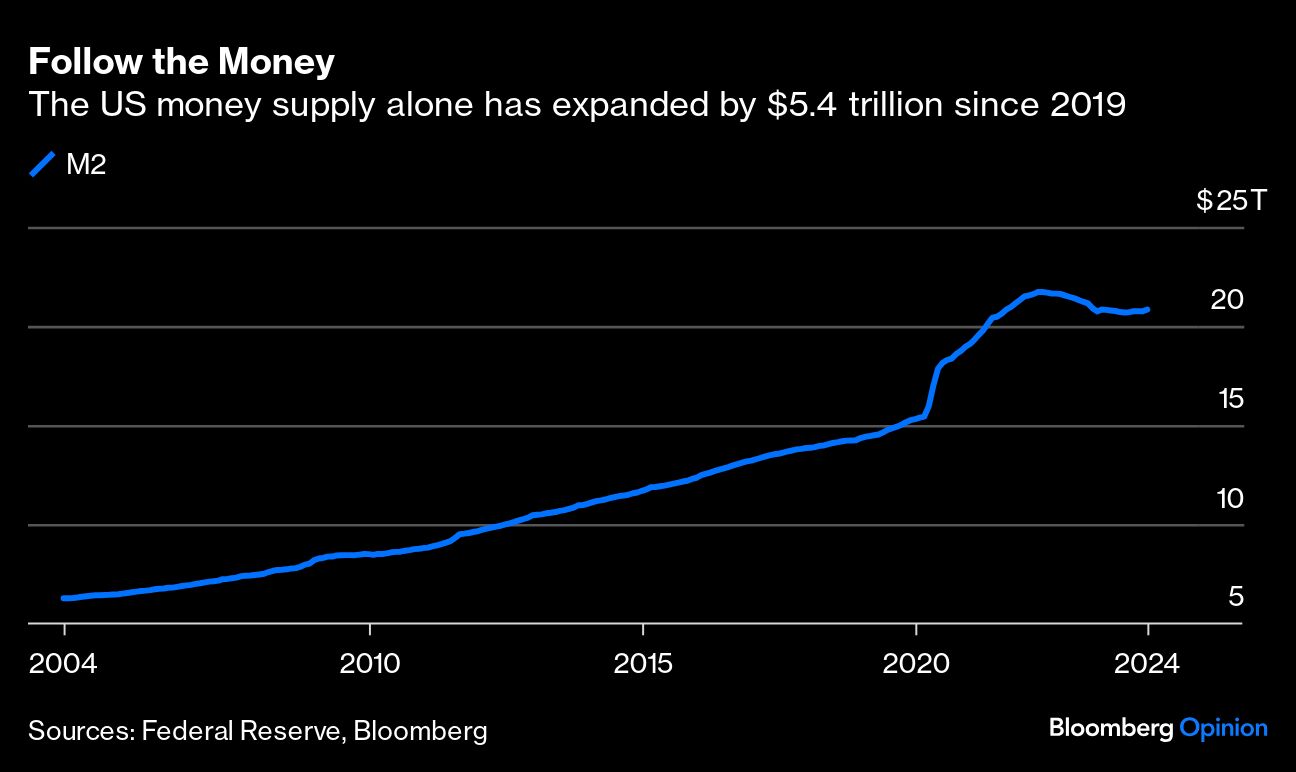

Second, the discussions around US debt focus too much on supply and not enough on demand. What gets lost is all the extra money created by governments as part of their response to the pandemic that’s still sloshing around the global financial system, looking for a home. The combined money supply of the US, China, the euro zone, Japan and eight other major developed economies has surged by $21.5 trillion since 2019 to around $102 trillion, according to data compiled by Bloomberg.

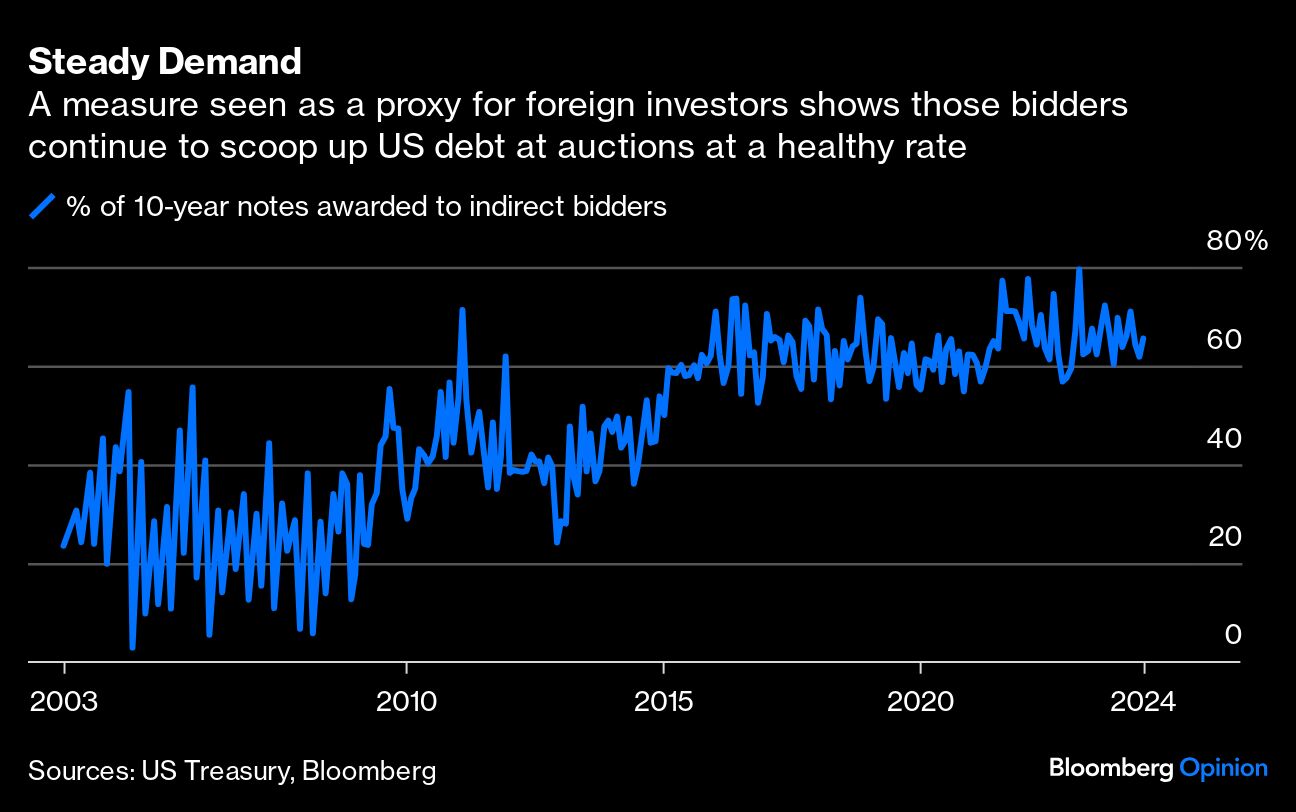

In short, US government debt provides a much-needed outlet for this newly created money. This is evidenced by the Treasury’s debt auctions, where indirect bidders — a group of buyers generally viewed as a proxy for foreign demand — accounted for around 65% of last week’s purchases for the 10-year Treasury note, little changed from four years ago. It doesn’t hurt that US government bonds yield, on average, almost 2.50 percentage points more than the debt of other developed nations, a juicy lure for foreign money considering that the average difference has been around 1 percentage point in favor of the US since 2000, according to ICE BofA bond indexes.

In many ways, foreign demand for US bonds is part of a much bigger story about America’s economy and its perceived exceptionalism. The evidence can be seen in the US stock market, which has outperformed the rest of the world by about 52 percentage points since the end of 2019 as measured by MSCI indexes. Nine of the 10 biggest companies worldwide by stock market capitalization (excluding Saudi Arabia’s state-owned oil company Aramco) are based in the US.

In the currency market, the dollar has strengthened since the end of 2019 against the 31 most actively traded currencies, as measured by Bloomberg, with the exception of Mexico’s peso and the Swiss franc. The US is the world’s biggest oil producer. It ranks as the third-most innovative country, behind Switzerland and Sweden. The global tech industry is centered in the US, as is the burgeoning artificial intelligence sector. And 54% of the world’s more than 1,200 global unicorns — startups valued at more than $1 billion — last year called the US home.

No doubt, America’s 334% debt-to-GDP ratio is uncomfortably high, even if it is down from the 2009 peak. Less debt is preferable, if only to ensure we have enough of a financial cushion to support the economy through the next crisis, whatever it may be. Alexander Hamilton, the first Secretary of the Treasury, said 242 years ago that “a national debt, if not excessive, will be to us a national blessing.” That still holds true, and we seem to be quite a bit away from what the bond market considers excessive.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Robert Burgess