Like clockwork, the commodities market worries in May about the strength of oil demand heading into the northern hemisphere summer holiday. Nervousness about the seasonal pickup in oil consumption abounds. It happened in 2023, and it’s happening again this year. But as before, traders’ concerns are misplaced: Oil demand growth is doing just fine.

The anxiety is reflected in the price of Brent crude, the global oil benchmark, which has dropped to less than $85 a barrel in recent days, down from about $90 a barrel in April. With the OPEC+ oil cartel meeting on June 1 to decide whether to prolong production cuts, the status of global demand matters. The group should look beyond the current noise and see that consumption remains firm.

Admittedly, there are pockets of demand weakness. The middle distillates fuel segment, which includes diesel and heating oil, have seen soft consumption so far this year. But that’s largely due to a warm winter in the northern hemisphere, which reduced heating needs, rather than underlying economic malaise.

In the diesel market, the biggest problem isn’t demand, but supply: Renewable diesel and bio-diesel are taking market share more rapidly than expected, in the process magnifying the diesel glut. In February, the last month with monthly data available, biodiesel and renewable diesel accounted for about 8.5% of total US diesel consumption. In 2020, the market share of both was under 1%.

Overlooked, however, are the pockets of demand strength.

Gasoline consumption is rising beyond what many had anticipated even as electric vehicles become more popular. Notwithstanding the increase in EV sales, there are now more cars than ever powered by internal-combustion engines. And pump prices are at levels that don’t discourage consumption, particularly in emerging markets.

Only a year ago, the International Energy Agency ventured that global gasoline demand peaked in 2019, and EVs meant that consumption would never return to pre-pandemic levels. Now we know better: Already last year, gasoline demand surpassed that, and in 2024 it’s growing even further.

Jet fuel is the other refined product doing better than expected despite the widespread adoption of more fuel-efficient planes. For the last 18 months or so, those efficiency gains put a brake on jet-fuel demand. But now the number of flights and, importantly, the quantity of miles flown have increased so much above 2019 levels as intercontinental travel resurges that jet-fuel consumption is for the first time matching seasonal pre-Covid-19 levels. In early May, the number of flights was 5% above the same time of 2019, while the number of flight-miles was nearly 10% higher, according to Airportia, a data provider.

When you add it all up, oil demand growth is still looking healthy for 2024. Granted, it won’t advance as much as the uber-bullish forecasters had hoped. In particular, OPEC’s own prediction of a 2.2 million-barrel-a-day gain looks farfetched — if not absurd. Yet, it’s on track to reach the far more reasonable 1.2 million gain anticipated by the International Energy Agency, setting a record of more than 103 million barrels a day.

If anything, the balance of risk is skewed toward demand growing this year by more than the IEA currently expects. A lot more? Not much, but a gain of 1.3 million to 1.5 million appears at hand.

Healthy demand notwithstanding, the market seems to be struggling with two problems.

The first is optics: While growth is robust, even strong, it’s much slower than in 2021, 2022 and 2023, the years of recovery from the 2020 pandemic-induced collapse. The IEA, which has overhyped the slowdown for months, put it in its right context in April: “Despite the deceleration that is forecast, this level of oil demand growth remains largely in line with the pre-Covid trend, even amid muted expectations for global economic growth this year and increased deployment of clean energy technologies.”

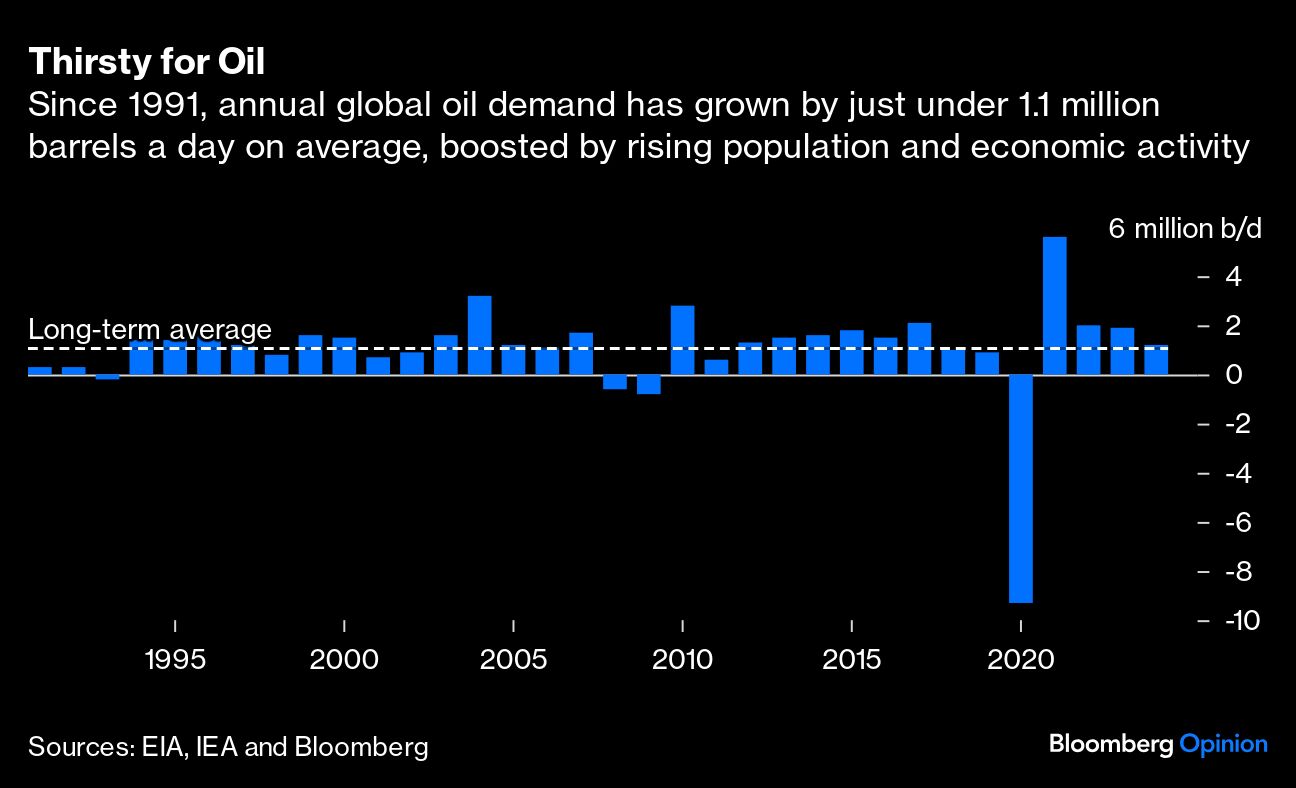

From 1991 to 2023, global demand for crude grew an average of 1.05 million barrels a day. Excluding the Covid-19 impact — and the recovery from it — oil-demand growth has averaged 1.18 million barrels a day over the last 30 years — in line with the IEA’s forecast of 1.2 million for 2024 which, technically, signals an above-average number.

The second is overreliance on US weekly oil data, which is inherently noisy – the typical statistical tradeoff between speed and completeness. The Energy Information Administration, which compiles oil statistics for the federal government, has been struggling for several years to nail the true level of consumption. Weekly data moves the market, but when the numbers are revised with the publication of monthly statistics – almost invariably higher – fewer pay attention.

Consider February, the latest fully revised: Using weekly statistics, the EIA estimated US oil demand initially at about 19.52 million barrels a day for the month, lower than a year before, raising alarms in the market. But final data, which was released only a few days ago, showed a very different reality: demand was higher year-on-year, reaching the quite punchy level of 19.95 million barrels a day.

The oil bulls still have reason to worry: With OPEC+ trying to keep prices as close as possible to $100 a barrel, non-OPEC supply, including from biofuels, keeps surging. But the focus on demand weakness is misplaced.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Javier Blas