The consumer price data last week showed a gradual deceleration in housing inflation. Economists expect this will persist for a while as official statistics slowly catch up to moderating market rents. Before you celebrate, it’s worth noting the first-quarter earnings updates of major real estate investment trusts, or REITs, where executives painted a less optimistic picture for tenants.

Elevated levels of new supply are weighing on rents in many metros at the moment, but apartment REITs — which set the pace for the rental market in many wealthy and growing metro areas — are seeing some unexpected offsets. The upshot of their commentary suggests that by the time tamer readings of shelter inflation allow the Federal Reserve to consider cutting interest rates, real-time rent increases should actually make them question whether easing policy is the right idea.

The most significant unexpected dynamic supporting apartment demand — and hence occupancy and rents — that executives called out was the sharp drop in the number of people leaving rental apartments to move into homes they have bought. Coastal powerhouse AvalonBay Communities Inc. reported a record-low 7% turnover due to homebuying, compared with their long-term average of 16% to 17%. Essex Property Trust Inc. put the number at 5%, also a record low, versus their longer-term average of 12%.

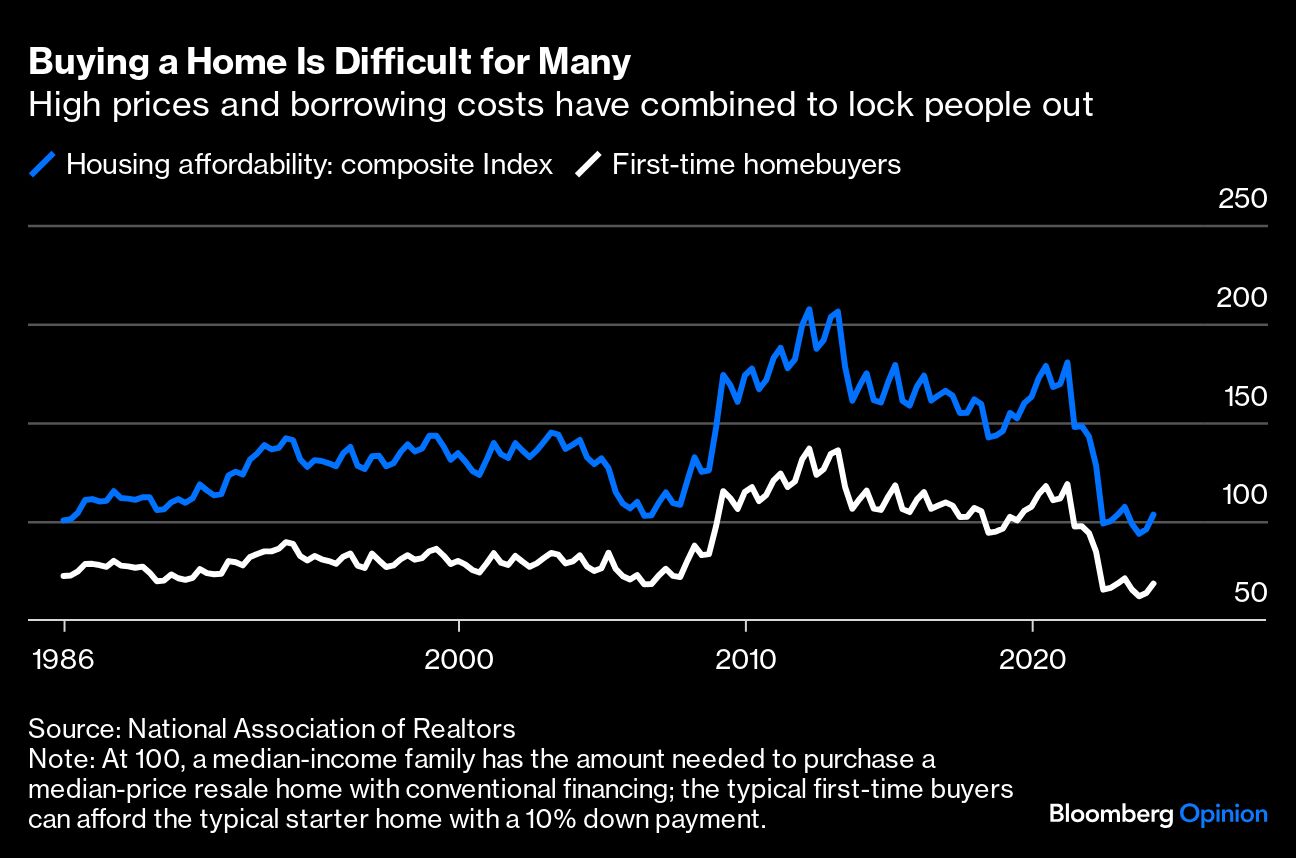

I say unexpected because even though homebuying affordability has been bad for a while, the last time these companies reported earnings, in late January, it looked like homebuyers might catch a break in 2024. At that point, markets were still anticipating a fairly aggressive cycle of rate cuts from the Fed, and 30-year mortgage rates had declined to around 6.6%. Expectations of rate cuts have been dashed since then, and mortgage rates have risen above 7% to further worsen housing affordability.

Due to both the seasonal spring increase in home prices and higher loan rates, the monthly payment that homebuyers are committing to has increased by around 15% since late January, according to Redfin Corp. That payment shock has left many would-be buyers trapped in apartments and kept the rental market from softening as much as it otherwise might have.

Continued strong job growth is another dynamic that’s allowing the apartment market to weather the flood of supply hitting some parts of the country such as Phoenix and Austin in the Sun Belt. In the first four months of 2024, the US added almost 250,000 jobs per month, defying economists’ expectations for weaker numbers. And in general, job growth equals apartment demand growth.

Coastal markets don’t have nearly as much supply being delivered, and the impact is already apparent. Equity Residential Property Trust, which like AvalonBay has a large coastal presence, noted that Seattle and San Francisco have both been performing better than was expected earlier this year. Executives pointed to the boost from artificial intelligence to the labor market, return-to-office mandates, and a perceived improvement in local governance that has led to more confidence in downtown areas.

And while the furious construction of the pandemic years means new apartments will continue to hit some markets for a few quarters to come, this will likely be followed by a lull. AvalonBay, which is looking to increase its exposure to Sun Belt markets, said that they would rather try to buy existing properties at a discount than take on the costs and risk of building something new. Camden Property Trust, which has a sizable Sun Belt presence, said they will get “more aggressive on the development side towards the end of the year and beginning of next year,” if economic conditions continue as expected. By that timetable, units wouldn’t hit the market until 2027 at the earliest.

The improved outlook for rents without meaningful development on the horizon is probably why the stocks of AvalonBay and Essex hit their highest levels since 2022 last week. The Bloomberg REIT Apartment Index has climbed almost 13% since the end of February, compared with the S&P 500 Index’s 4% advance.

All this raises questions about how the Fed will think about housing inflation in September, around the time markets expect the first interest rate cut. It’s likely that housing inflation as measured in the indices that policymakers track will keep decelerating, at least modestly, for the balance of the year. But based on what the apartment REITs are saying — and some aggregated measures such as Apartment List data as well — real-time or market rent growth will be accelerating by then, with a strong likelihood of that continuing into 2025. If current market trends are giving Fed Chair Jerome Powell confidence that the shelter inflation data will moderate later this year, how will he respond when the official numbers look good, but market signals don’t?

For renters looking for reasons for optimism, the best hope in the short term is that the Fed ignores any reacceleration in shelter inflation and cuts rates anyway, that mortgage rates fall and that affordability in the for-sale market improves. This would pull more people out of the rental market, putting downward pressure on occupancy and rents. But it sure seems like, in the aggregate, the timetable for rising rents is moving up, and I’d expect a pickup by late summer or early fall, if it’s not happening in some places already.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Conor Sen