The Rise of the Disposable Car

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsModern cars are equipped with heaps of electronic devices, many of which are designed to reduce the frequency and severity of accidents. But there’s a catch: The high cost of repairing these systems may mean the vehicle is written-off, or totaled, following a crash.

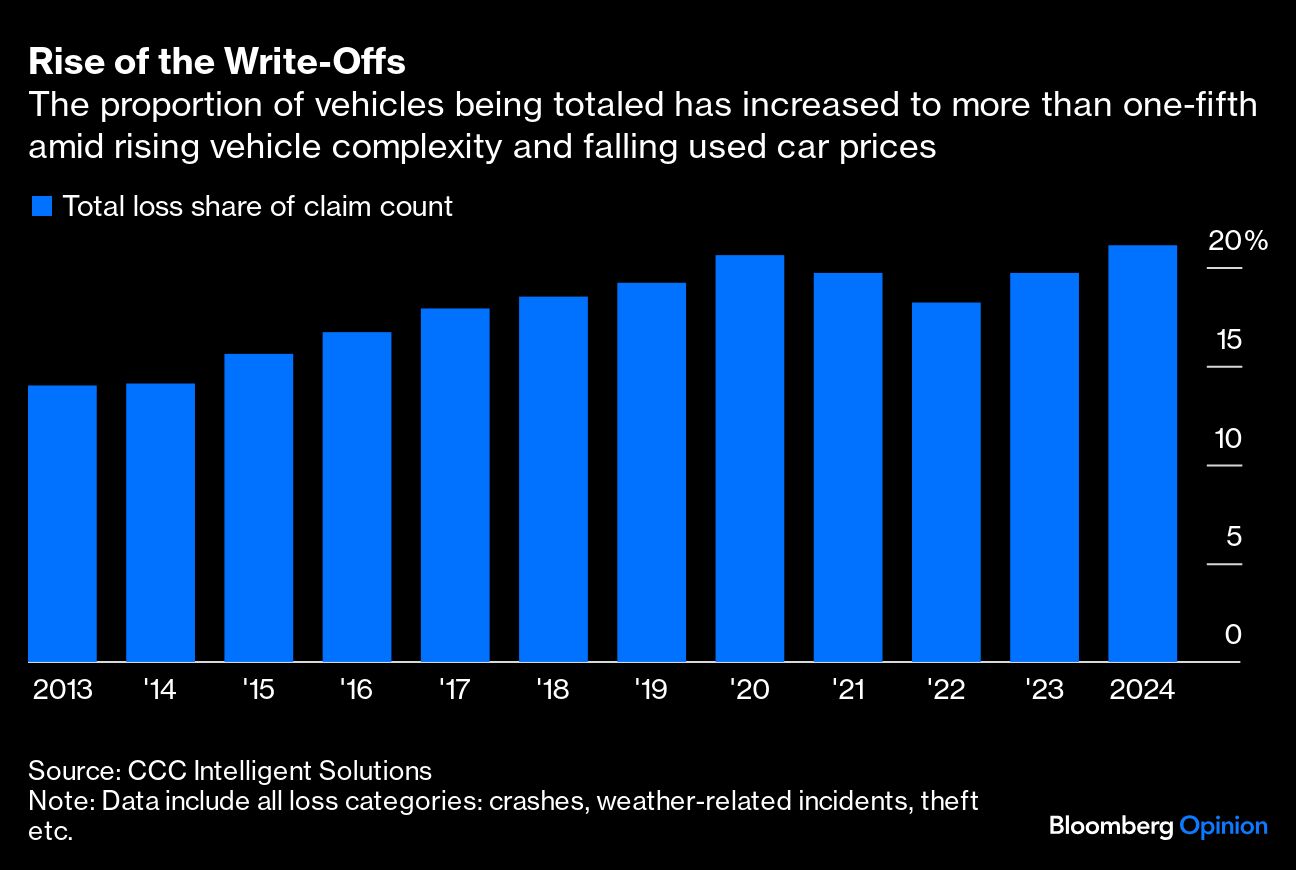

More than one-fifth of vehicles are now declared a write-off by insurers after examining claims; this is close to a record and around five times higher than in 1980, industry participants say. The proportion of totaled cars may increase further as declining used car prices tip the scales in favor of salvage versus repair. Auction firms that re-sell wrecks on behalf of insurers stand to benefit from this trend, whereas car buyers who stretched to finance their vehicles, but scrimped on insurance cover, risk nasty financial shocks.

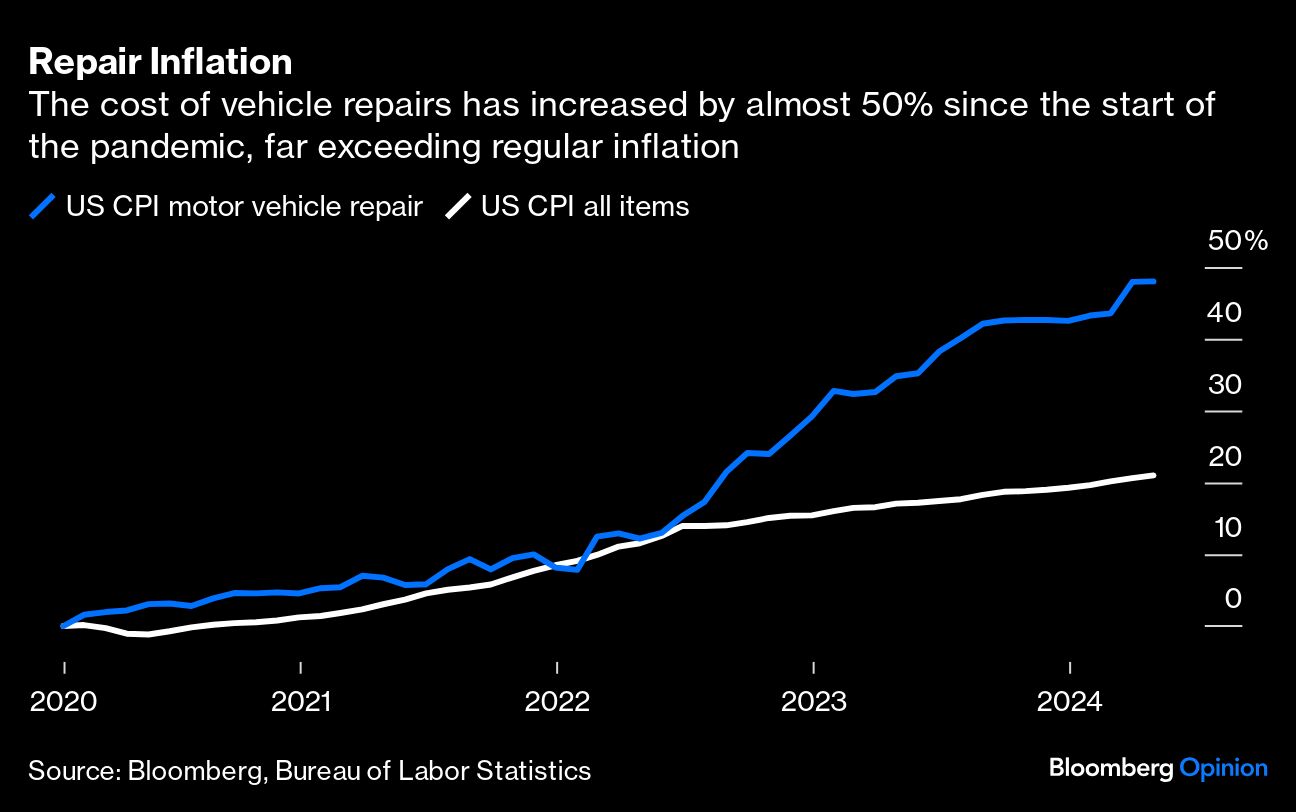

It’s economically rational for insurers to write off vehicles when the cost of repairs exceeds the value of the car immediately before the crash minus the expected salvage proceeds. Right now, repairing a car is very expensive, which means more are getting totaled.1

Of course, most of these write-offs are pretty old — in the past two decades, the average age of cars on US roads has increased to 12.5 years from fewer than 10 years. The fact cars last this long shows their improved durability — but they’re often not worth repairing if involved in a crash.

At the same time, the proportion of brand new vehicles being written off has increased, according to CCC Intelligent Solutions Holdings Inc, a software company that facilitates insurance claims and repairs; it attributed this trend in part to growing vehicle complexity.

For example, newer models include “Advanced Driver Assistance Systems” such as automatic braking and lane-keeping assistance; sensors and cameras are typically located on the exterior of the vehicle and are easily damaged in crashes and hail storms. When that happens, car technicians need to install, test and precisely calibrate the equipment; in several crash scenarios recently examined by the American Automobile Association, ADAS accounted for 38% of repair costs on average. AAA estimated the cost of replacing and calibrating a side mirror with a camera on a new F-150 pickup truck, for example, at an eye-watering $1,600.

Drivers are also still getting into plenty of accidents, perhaps because they are looking at their phones instead of the road or are lulled into a false sense of security by ADAS features, or both. “The presence of more vehicle technology is not significantly reducing claims frequency or accident severity but is increasing overall costs,” the CCC study concludes.

Overall, 21% of vehicles were totaled following an insurance claim in the first-quarter of 2024. Salvage auction firm Copart Inc. says this proportion could eventually exceed 30% as various trends, including rising complexity, continue to make “repairing vehicles less economically attractive to insurance carriers,” its management said in February.

This sounds wasteful, but nowadays wrecks aren’t just broken up for scrap metal and parts — buyers from emerging markets export, restore and then return totaled vehicles to roads; they can do so profitably because labor costs are lower overseas, which increases the potential vehicle value at auction. These tailwinds have boosted Copart’s shares by 23% in the past year, and around 1,110% since 2014, valuing the group at $53 billion. However, with the stock trading on 38 times estimated earnings, Copart isn’t as cheap as some of totaled vehicles it sells.

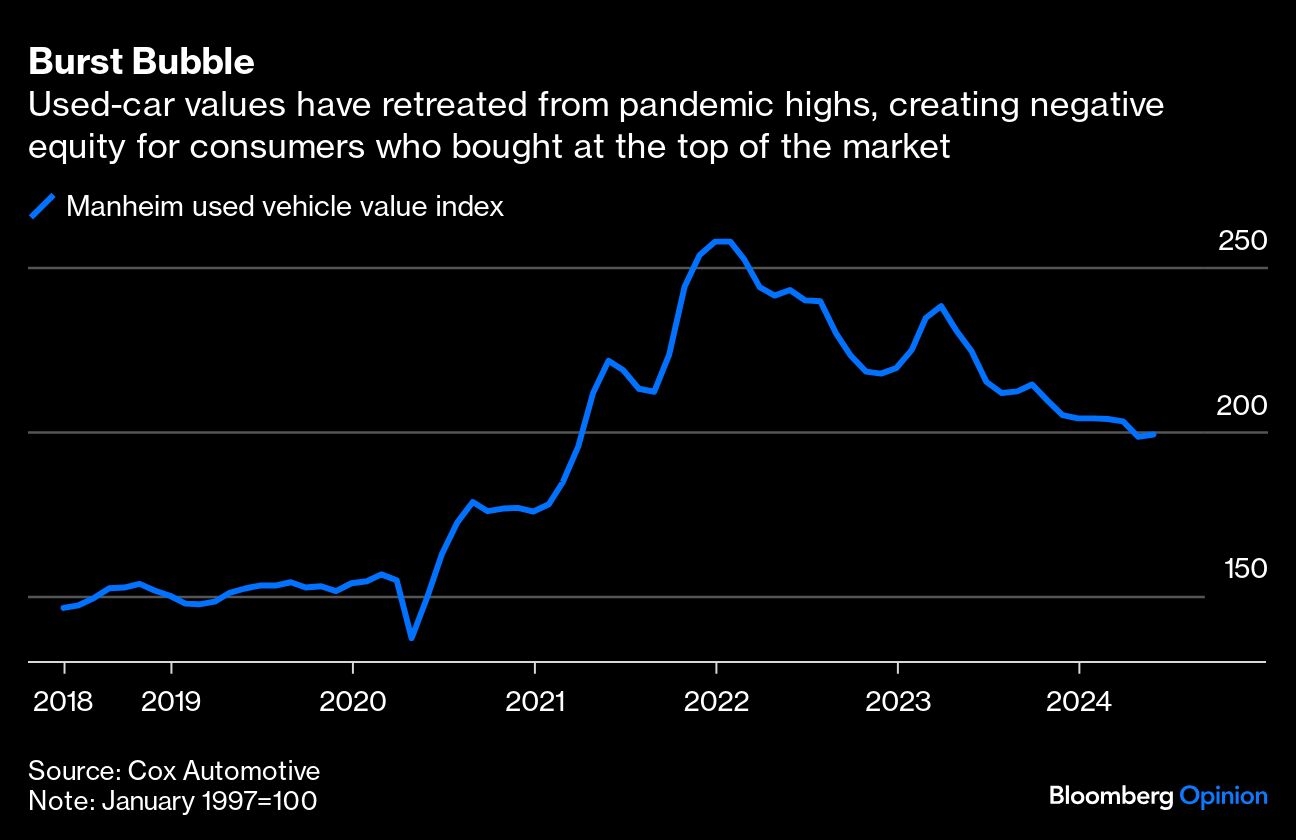

Another factor contributing to more write-offs: declining used car values. Insurers were strongly incentivized to fix vehicles when second-hand prices soared during the pandemic, but these trends have begun to reverse.

The jury is out on whether electric vehicles are more likely to be written-off due to high repair and battery replacement costs — so far EVs have been totaled slightly less than gasoline vehicles. However, I worry very high depreciation rates could result in more EVs heading to the junk yard.2

Plummeting used car prices mean many borrowers owe more on their car loan than their vehicle is worth. Negative equity isn’t a problem if you don’t plan to trade-in or sell your ride, but it could be if you’re in an accident. Drivers who paid top dollar for a new vehicle during the pandemic are particularly vulnerable.

Guaranteed Asset Protection insurance is available, which helps bridge the difference between the current cash value of the car and what the borrower owes. The value of these policies is being scrutinized by UK regulators, due to high dealer commissions. While consumers are already struggling with higher insurance costs, having this add-on could avoid a nasty shock if the vehicle is wrecked.

Perhaps one day we’ll all whizz around in self-driving cars and accidents will be rare. But that’s still a ways off. Until then, expect the cost of fixing vehicles to continue to drive insurance premiums and total loss frequency higher.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Live Virtual Event: Join Now

Upcoming Virtual Events View All