Why Nvidia, Not Solar, Has a Place in the Sun

Membership required

Membership is now required to use this feature. To learn more:

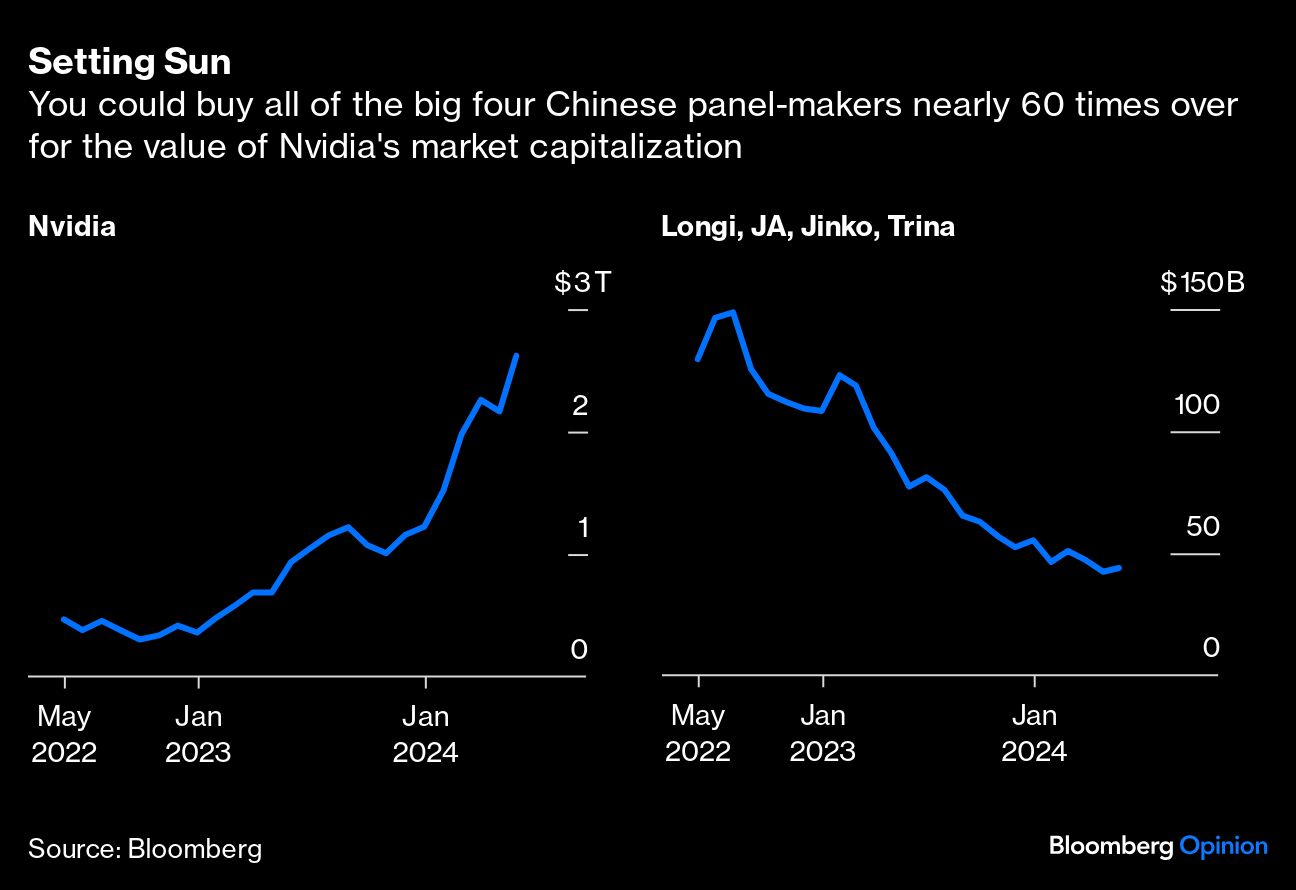

View Membership BenefitsThe semiconductor industry is a strange field. Play your cards right, and you can turn $60 billion or so of annual revenue into a $2.62 trillion business. Do things differently, and roughly the same volume of sales might translate into $44 billion of market capitalization.

Such divergent outcomes tell us a lot about the way capitalism in the US and China is producing drastically different outcomes on a planet confronting the wrenching shifts driven by artificial intelligence and climate change.

If you measure technology by the value of the companies that sell it, you would argue — as some in the US have been doing — that AI is the future of industry, while renewable power is a busted flush.

The four biggest solar panel-makers — China’s Longi Green Energy Technology Co., JA Solar Technology Co., JinkoSolar Holding Co., and Trina Solar Co. — have lost about two-thirds of their combined market cap over the past two years to hit that miserable combined $44 billion level. Meanwhile, Nvidia Corp. has ridden a wave of excitement about AI to become the world’s most valuable company after Microsoft Corp. and Apple Inc.

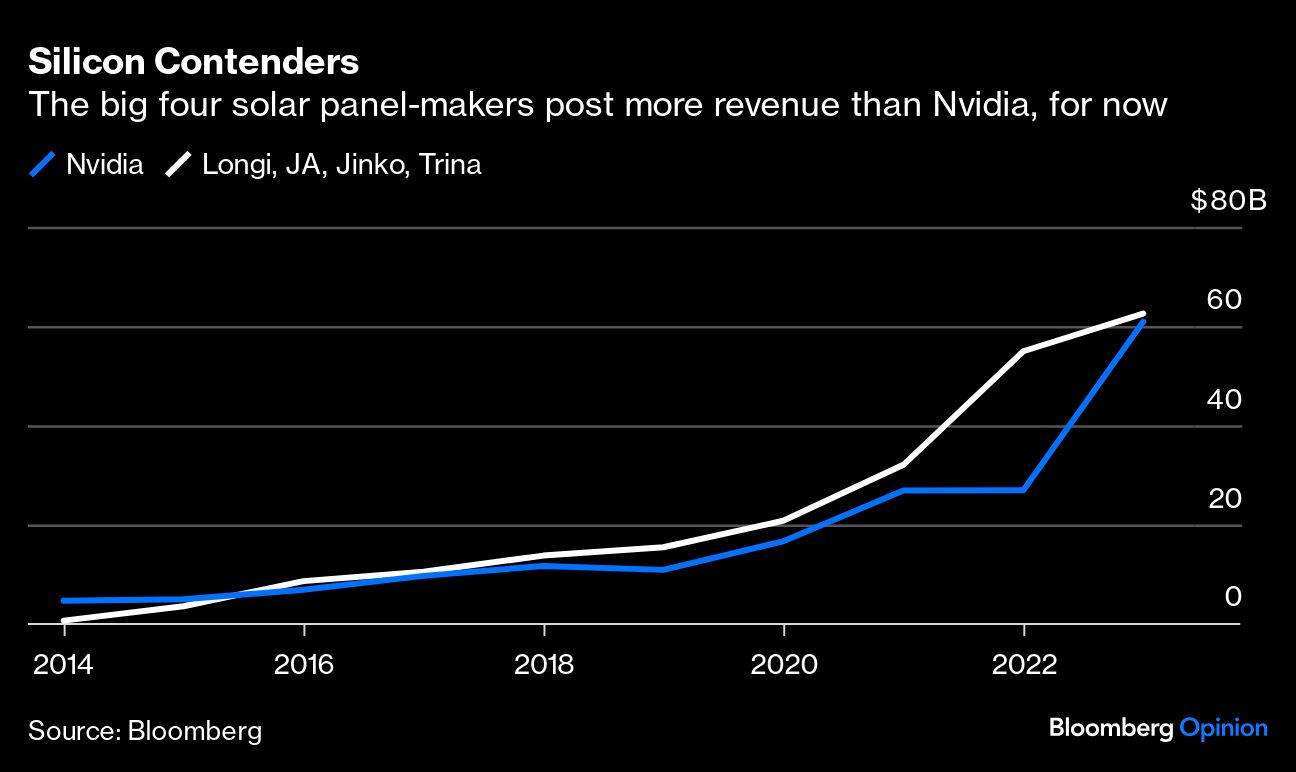

The revenue paths of the two starkly divergent groups are remarkably similar. The semiconductor markets in which both sides specialize — turning silica-rich sand into, respectively, photovoltaic cells and AI chips — have traced almost identical roads to riches:

Markets aren’t wrong to make such a binary assessment. Nvidia really is a fundamentally better business than China’s big solar four. The reasons tell you surprising things about both industries, while providing a warning for investors in AI chips and a glimmer of hope for the beaten-down photovoltaics sector.

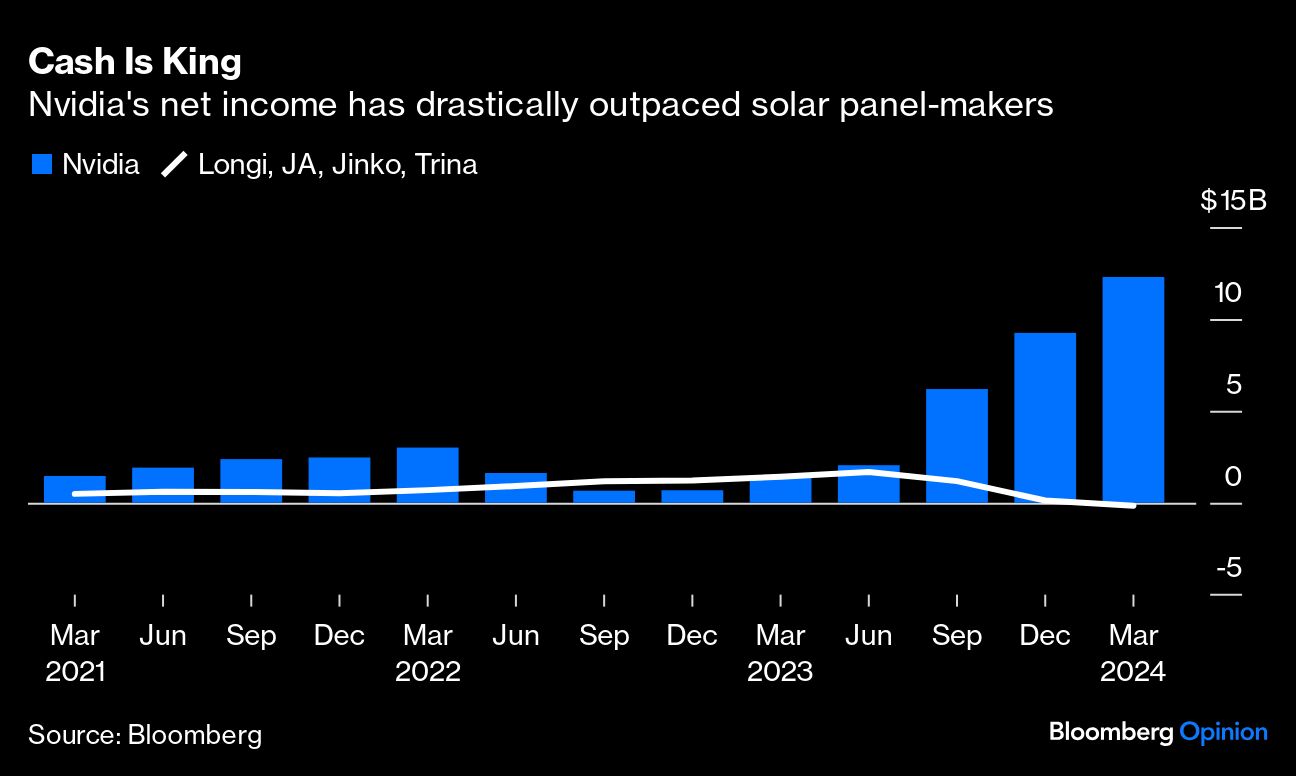

First, it’s worth looking at business models. Nvidia’s competitive edge is in designing chips, and it outsources the capital-intensive business of actually making them to foundries such as Taiwan Semiconductor Manufacturing Co. The solar companies are all physical producers, and as a result they’re exposed to a never-ending rollercoaster ride of depreciation and obsolescence. That shows up in Nvidia’s 56% return on assets, compared to less than 10% at the panel-makers.

There’s also the issue of monopolistic power. While photovoltaic manufacturers are fairly interchangeable and competition is cutthroat, Nvidia’s lead in making AI-appropriate processors means it has about 90% of the relevant market — a license to print money, or at least extract it from cash-rich Silicon Valley tech companies.

That translated into a net income margin of 49% last fiscal year. Solar manufacturers, with their highly commoditized products, perform far worse: an average of 3.7%, with Longi the clear leader on 12.6%.

Investors’ beliefs about the sustainability of this advantage provide the final piece of the puzzle. Nvidia’s valuation multiple of 36.73 times forward earnings isn’t particularly excessive for a red-hot industry darling, but it’s far above the solar companies — and the equity in US-listed businesses generally enjoys a hefty premium compared to China.

You might see this as a triumph of American free markets over Chinese dirigisme. That’s not quite right, though. The reason the panel-makers are struggling is precisely because they operate in a wide-open market with very low barriers to entry — a great setup if you want to grow the industry, but a terrible one for generating sustainable profits.

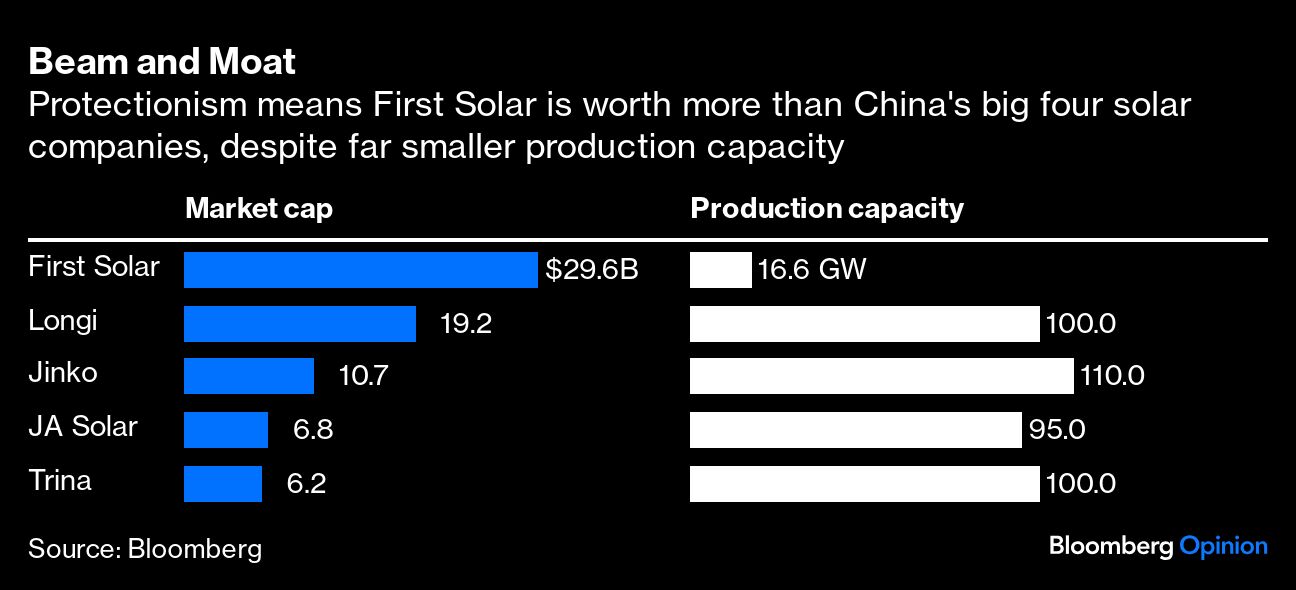

One telling detail of the above chart is the presence of one US cell company on it, First Solar Inc. After President Joe Biden doubled tariffs and announced new import investigations on Chinese solar panels this month, First Solar is now worth more than JA Solar, JinkoSolar and Trina Solar put together. That’s in spite of the fact that it uses a niche, high-cost technology that most companies have given up on, and can produce less than one gigawatt of cells for every 18 GW from the three Chinese companies.

The lesson is that shelter from the ravages of capitalist competition is great for shareholders, whether it comes as a result of intellectual property laws (as with Nvidia) or protectionism (as with First Solar).

It would be a mistake for either side to get either too despondent or too triumphant. Defensive moats like Nvidia’s are great until they aren’t. That 49% profit margin and 90% market share is an open invitation to the rest of the chip sector to invest heavily to compete.

The tech sector is littered with one-time market darlings — Nokia Oyj, Intel Corp., Cisco Systems Inc. — that suddenly found themselves brought down to earth by the resurgence of competition. On the flip side, the possibility of Beijing intervening to halt suicidal rounds of price-cutting has caused Chinese solar stocks to revive in recent days.

The deeper lesson for the battered photovoltaics sector is to look at what Nvidia has done right, and what they’re doing wrong. With such an interchangeable product, there’s very rarely a good reason to prefer a Longi over a Trina panel. No cell is indispensable the way an Nvidia GPU is. If solar panel-makers can crack that secret, they too might one day join the ranks of trillion-dollar businesses.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Live Virtual Event: Join Now

Upcoming Virtual Events View All