When people think about the Federal Reserve and interest rates in 2024, one common view is that economic growth and inflation remain too hot to justify rate cuts. Another is that the labor market and inflation continue to cool, and it will soon be time for rate cuts.

In deciding which of these opposing views will prevail, it’s helpful to look at the parts of the economy that the Fed has slowed most effectively. In sectors such as housing and manufacturing, the downward pressure from high borrowing costs is abating after a difficult few years. These areas are somewhere between bottoming and recovering even without Fed cuts. A meaningful easing cycle would likely create the conditions for a boom at a time when the central bank is still struggling to contain inflation — meaning any accommodation will need to wait until parts of the economy that have been less Fed-sensitive start to moderate.

The place where the central bank’s impact has been most pronounced is in housing, particularly the resale market where the pace of transactions bottomed at a 3.85 million annualized run rate last October, around the levels seen during the worst of the 2008 Great Recession. The number of owner-occupied homes in the US has increased by roughly 15% since then, so the overall turnover rate was effectively lower at the end of last year than it was at the end of 2008 when the economy was imploding.

Sales of existing homes have begun to recover modestly over the past several months, and as inventory levels rise, softening prices in some locations, that’s likely to continue even with elevated home loan rates.

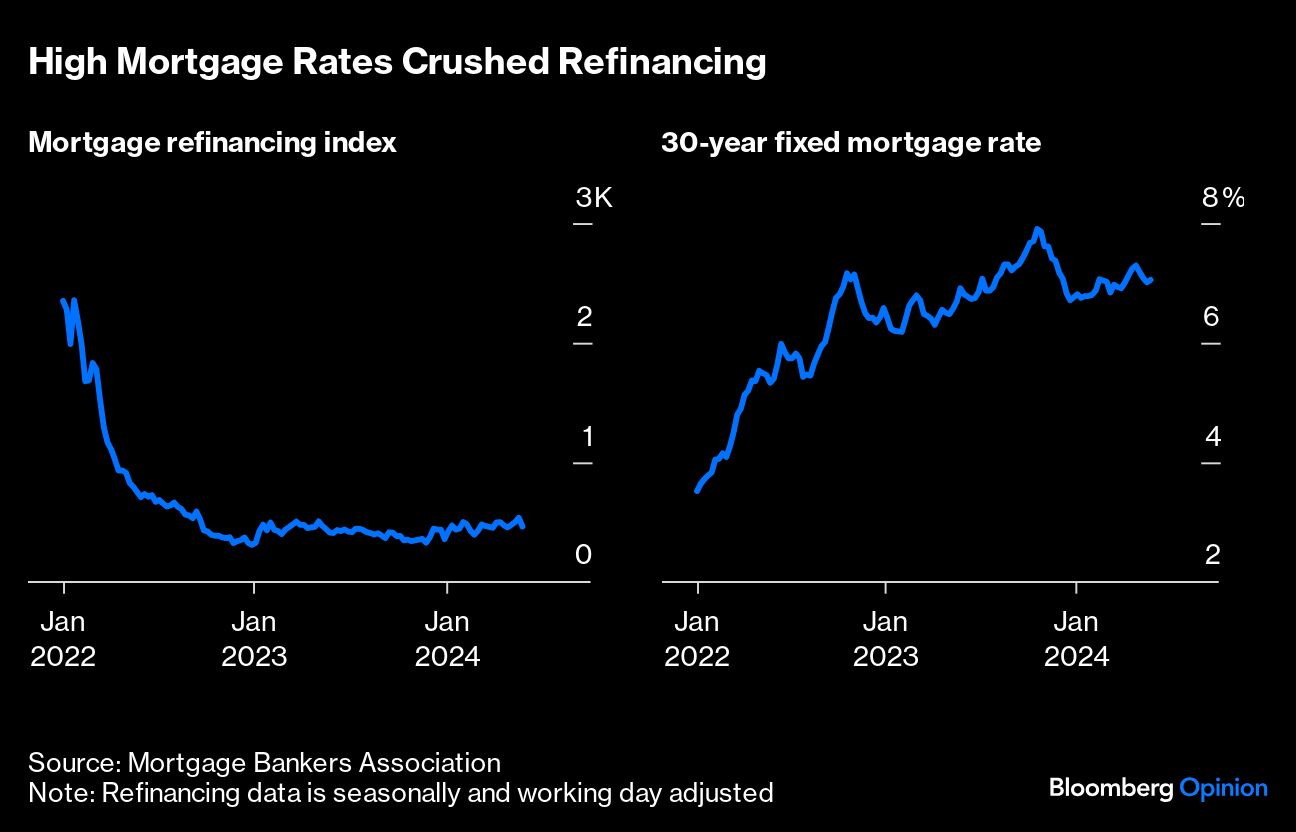

Mortgage refinancing is another part of the housing market that was crushed as rising borrowing costs eliminated the incentive to refinance. Activity levels fell by almost 95% between early 2021 and the end of 2022. Refinancing applications are now creeping higher even with mortgage rates above 7%, climbing in three of the past four weeks. To be fair, the absolute level remains very low by historical standards, but activity has picked up as some of the 8% mortgages issued last autumn become eligible for refinancing, and perhaps as some homeowners consolidate other higher interest rate consumer debt.

Mortgage rates ticking down to around 6.5% would keep refinancings flowing and unlock spending that has been so far constrained on things including automobiles and home furnishings, or home renovation projects.

Sales at home improvement and furniture stores, for example, have languished for over a year in line with subdued activity in the housing sector. Companies have instead prioritized tightly managing inventory levels while waiting for consumer sentiment to turn more positive.

Home Depot Inc. said earlier this month that inventory levels fell 11.7% year-over-year, and Target Corp. showed a 7% decline, on a view that households remain wary of spending on their homes and discretionary goods. Such caution from retailers is one reason why sentiment surveys of factory owners remain so pessimistic. Even so, the Institute for Supply Management’s manufacturing gauge moved back into expansionary territory in March for the first time since late 2022, before slipping back in April.

An increase in housing transactions or a greater willingness to borrow would fuel activity and spending. Households, after all, are in good financial health and sitting on trillions of dollars of home equity that many are waiting to tap into once borrowing costs moderate meaningfully.

Home Depot executives said during their earnings call that many households put off large projects not due to an inability to fund them, but because they keep hearing about how rate cuts are coming. This “waiting on the Fed to cut” dynamic didn’t exist in prior cycles but has emerged since the early 2010s once the central bank began to emphasize communicating its plans to the public.

That raises the question of how much additional economic activity is on hold. The used vehicle market, for one, seems poised for a pickup with sales growth having accelerated on a year-over-year basis for three consecutive months as price declines offset high financing costs. Apartment construction, commercial real estate transactions, and investment banking activity have all been in slumps and would benefit if interest rates fell. And banks are now in a better position to respond to loan demand after building up capital levels and offloading some risk following last year’s regional banking crisis.

These sectors — from resale housing to discretionary spending and bank lending — collectively represent an enormous amount of economic activity. Most started to improve over the past six months just as the Fed signaled an end to interest rate increases. All would benefit from more accommodative policy.

Standing in their way are the less credit-sensitive parts of the economy, namely government-backed infrastructure spending and artificial intelligence. So long as these sectors continue to boom, helping keep inflation above the Fed’s 2% target, American households — clamoring for lower borrowing costs — will have to wait.

A message from Advisor Perspectives and VettaFi: Join us on June 27th for the Midyear Market Outlook Symposium, where advisors will gain insights into macroeconomic trends, active ETFs, investing abroad, and more to navigate 2024's challenges.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Conor Sen