The people who experience the US economy continue to disagree with the people who measure it, and the most likely reason is inflation: Most Americans still see it as a major problem, while most economists don’t. But this debate recently veered from economics to semantics. Has the common definition of “inflation” changed, and do economists just need to accept it?

Felix Salmon of Axios essentially answers yes to both questions. “The meaning of the word ‘inflation’ has changed” he writes. “It used to mean rising prices; now it means high prices.” This helps explain, he says, the disconnect between Americans’ perceptions of the economy and economists’ assessment of it.

I would answer no to both questions, and not because I am an economist. Both people and economists — and I might point out that there is 100% overlap between these two groups — agree on what inflation is. The confusing part has to do with timing.

According to Merriam-Webster, inflation is “a continuing rise in the general price level.” When Americans complain that prices are high, they are implicitly comparing prices now to those of 2021, when inflation took off. When economists point out that “inflation” is lower, they are implicitly comparing prices now to 12 months ago.

Both time frames are informative, and prices rose in both periods, so both are inflation. Redefining “inflation” is unnecessary and counterproductive when all we need to do is make the implicit parts explicit.

This may be a case in which the often-maligned “Fedspeak” is a model. At the US Federal Reserve, where I worked for almost a decade, the time frame was always specified: the percent change in prices over 12 months, four quarters, one month, and so on. Why? Those are all measures of inflation, but without a frame of reference, it is confusing. Moreover, the Fed defines its mandate as “inflation at the rate of 2%, as measured by the annual change in the price index for personal consumption expenditures.” That’s a mouthful, and it makes sense to use “2% inflation” as a shorthand.

So economists don’t need to accept a new meaning for inflation so much as accept that we must communicate more clearly. That might help avoid these distractions over language.

A far more productive use of our time is to try and understand why people are extra gloomy now. The key word is “extra.” Economists would agree that, all else being equal, the 16% increase in overall prices from January 2021 through March 2023 would be cause for gloom. But all else is not equal. Unemployment has been under 4% for more than two years, while median wages are up 18%, and more for low-wage workers. And even with higher prices, consumer spending is up 11%, in nearly every major category, including food at restaurants.

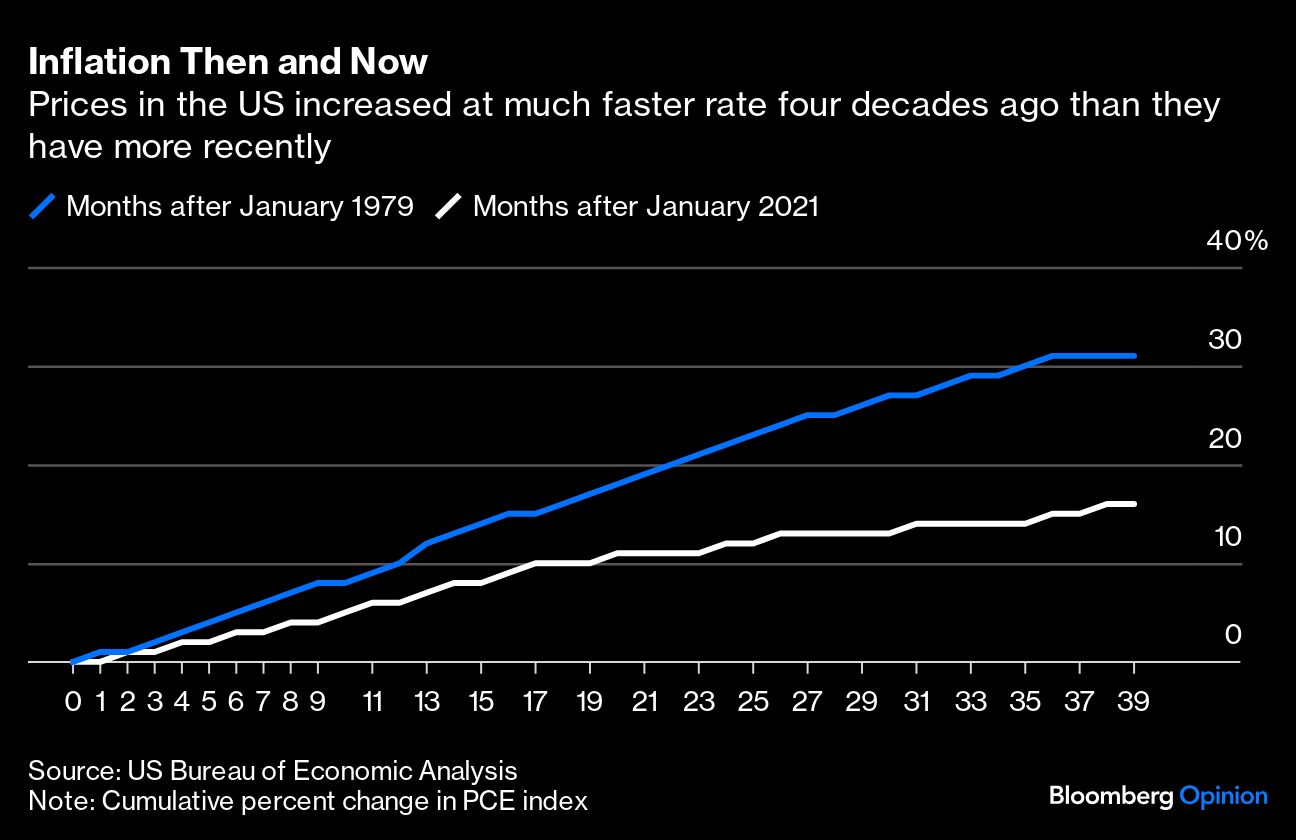

Another way to contextualize the current gloom is to look at past gloom. The 1970s and early 1980s were another period when prices rose rapidly for multiple years. In 2022, when year-over-year inflation peaked, consumer sentiment, as measured by the University of Michigan, hit its lowest level since 1980. From 1978 to 1981, the price level rose 30%, about twice the increase now. In addition, unemployment averaged almost 7%. Yet consumer sentiment in 2022 was lower.

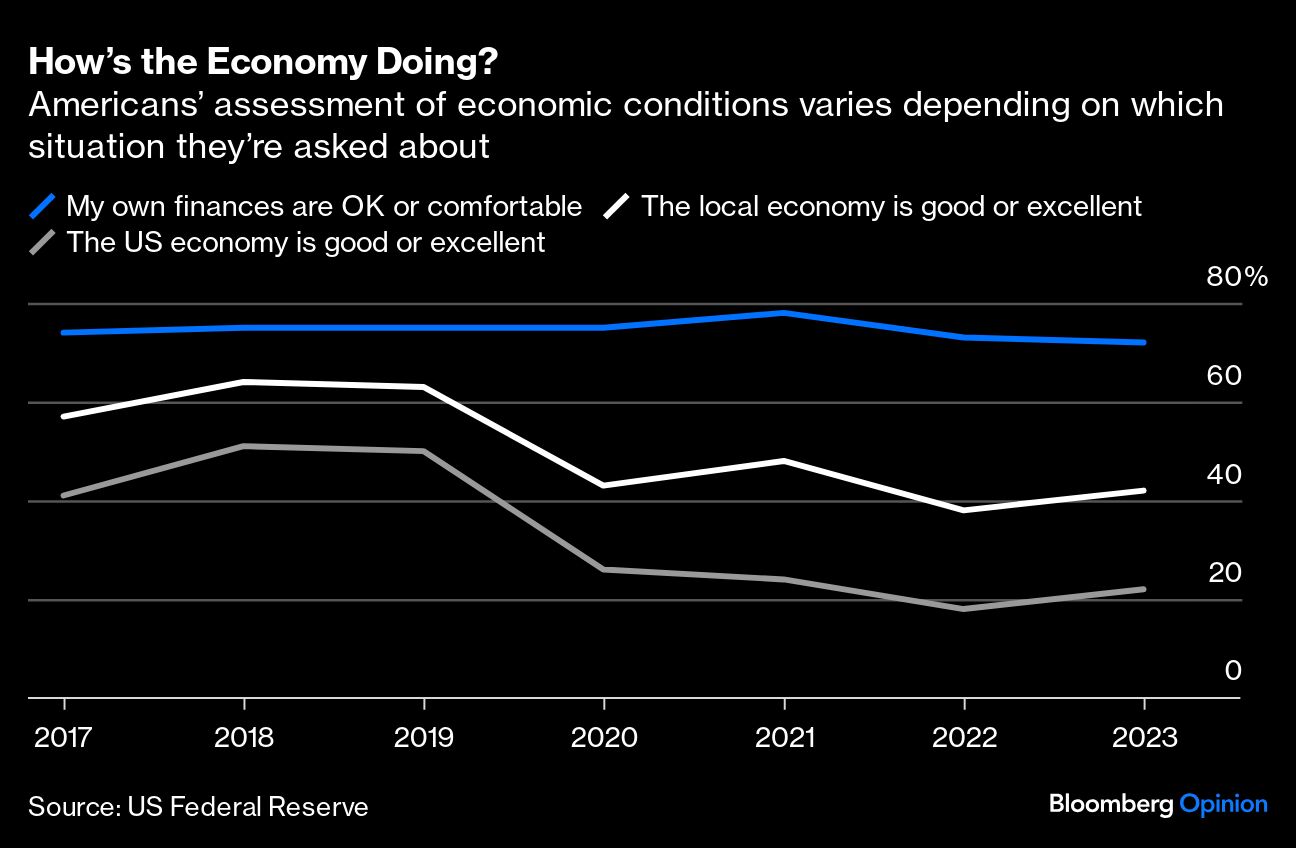

One more puzzling development now is the disconnect between people’s assessment of their own finances and their assessment of the US economy. The Fed’s Survey of Household Economics and Decisionmaking shows that clearly.

Last fall, 72% of respondents said they were financially “doing OK” or “living comfortably.” That’s relatively close to pre-pandemic levels. However, when asked about their local economy, only 42% said it was “good” or “excellent.” And then, when asked about the national economy, there was a big divergence: Only 22% said it was “good” or “excellent.” That’s a 50-percentage-point gap — among the same people. Moreover, the gap widened in 2020 and has been relatively stable since.

It is hard to pin the divergence in 2020 on inflation that arrived a year later. Something happened, surely — but the extra gloom likely goes beyond economics. It may be trauma from the pandemic upending our lives, social media amplifying what was already a bias toward negative news, a hyperpartisan environment, geopolitical events, or fears about what comes next.

Words are not the problem. Nor are economists’ tools especially well-suited to sorting out non-economic explanations. So maybe the best way forward is fewer words from economists, less argument over the meaning of common economic terms, and more discussion about all the non-economic reasons for our gloom. That’s my hope.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Claudia Sahm