Steward Health Care System LLC was once thought to be the future. Its chief executive officer, Ralph de la Torre, was named “health care’s new maverick” by Fortune in 2012. With the help of private equity giant Cerberus Capital Management LP, de la Torre turned six Boston-area facilities into one of the nation’s largest for-profit hospital chains.

Now Steward is on the brink of financial ruin. The company owes millions in rent and has been sued by several vendors for unpaid supplies and services. Last month, Steward filed for Chapter 11 protection, making it one of the biggest hospital bankruptcies in decades. Tens of thousands of patients and workers are in turmoil.

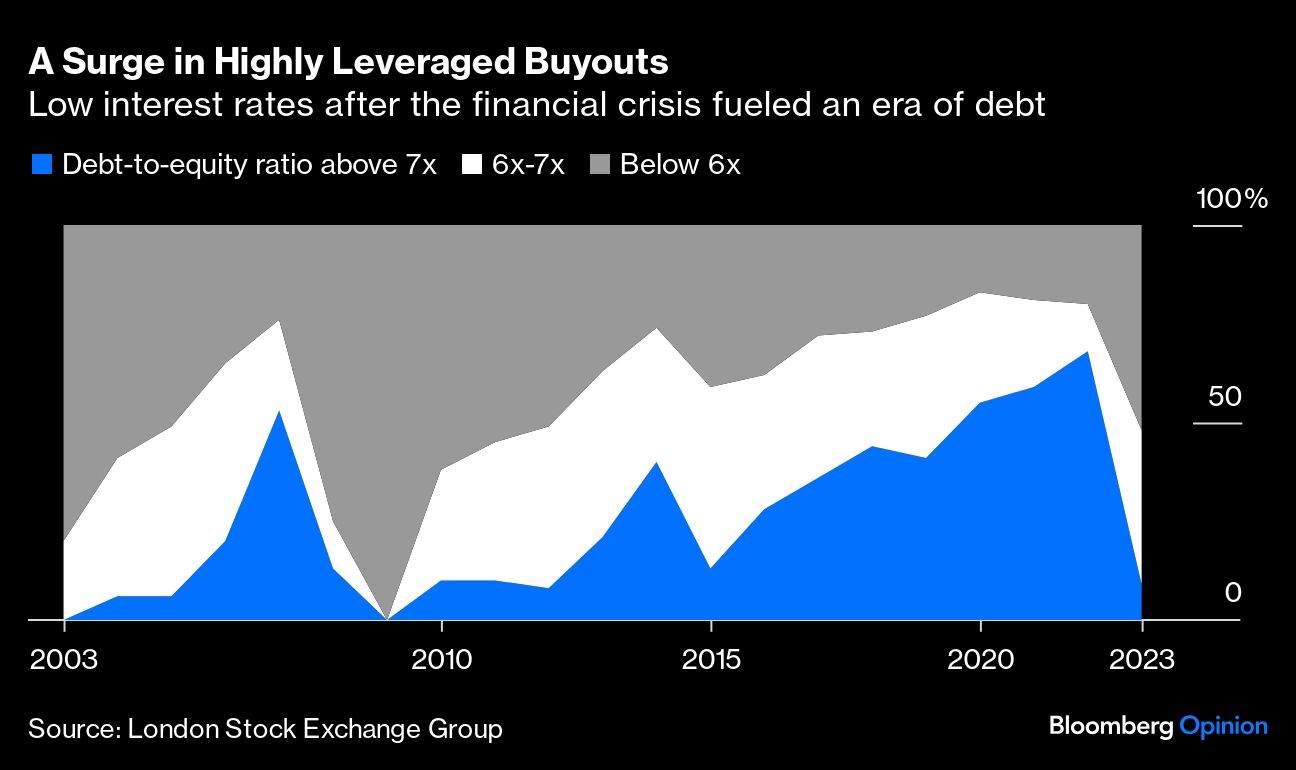

Exactly what caused this unraveling is hard to say — and that’s part of the problem. As private equity investment in health care has surged to almost $1 trillion over the past decade — funding new technologies, clinical trials and more — a lack of transparency has made it hard to assess whether the industry is also putting patients at risk. In that regard and others, Steward’s failure should be a cautionary tale.

When de la Torre became CEO of the Caritas Christi Health Care hospital group in 2008, its facilities were in decay. Caritas faced an underfunded pension obligation for 13,000 workers. The $895 million rescue de la Torre orchestrated made him a local hero.

At first, conditions improved. The newly named Steward Health Care upgraded its technology and electronic records systems. Emergency rooms got much-needed renovations. The pensions were saved. But Steward also borrowed heavily to fund its expansion. Repayment deadlines loomed and the company needed cash. In 2016, Steward sold its only asset — land — for $1.25 billion. The deal required Steward to pay millions in rent on the property it once owned. It also allowed equity owners, including de la Torre, to extract a $484 million dividend.

For Steward, the deal was a fatal blow. Most hospitals make money from expensive procedures and commercially insured patients with their generous reimbursement rates. Steward, with mostly low-income patients, had neither. Its rent payments slipped. Other bills piled up and vendors shied away. Last fall, a woman reportedly died after giving birth because a device that would’ve stopped her bleeding had been repossessed.

Such financial problems aren’t uncommon. Medicaid and Medicare pay for more than half of inpatient days at 96% of hospitals nationwide. For many struggling hospitals, private equity offers a lifeline: a way to streamline operations, upgrade facilities and outsource administrative burdens. Yet the industry’s business model — loading up acquired entities with debt, stripping down assets and leasing them back, and making a quick and profitable exit — can be a poor fit with the messy reality of American hospitals.

In health care, “efficiencies” are typically achieved by reducing staff, slashing labor costs and eliminating hospital units, all of which are dangerous for patients. One study found that hospital-acquired complications rose 25% after a facility had been bought by a private equity firm; falls increased 27%; and central-line infections were 38% higher. And while aggregate findings on health outcomes are mixed, many measures of quality, including patient satisfaction, are negative.

Alarmed by these trends, some states are seeking to rein in private equity acquisitions in health care. They need to strike a careful balance: The goal should be preventing irresponsible behavior while still encouraging much-needed investment.

As a start, more transparency would help. The property deal that sank Steward transpired with regulators none the wiser. Bringing certain disclosures in line with public companies — including financial statements, ownership changes, sales of important assets and health outcomes at private-equity-owned facilities — would be a sensible step.

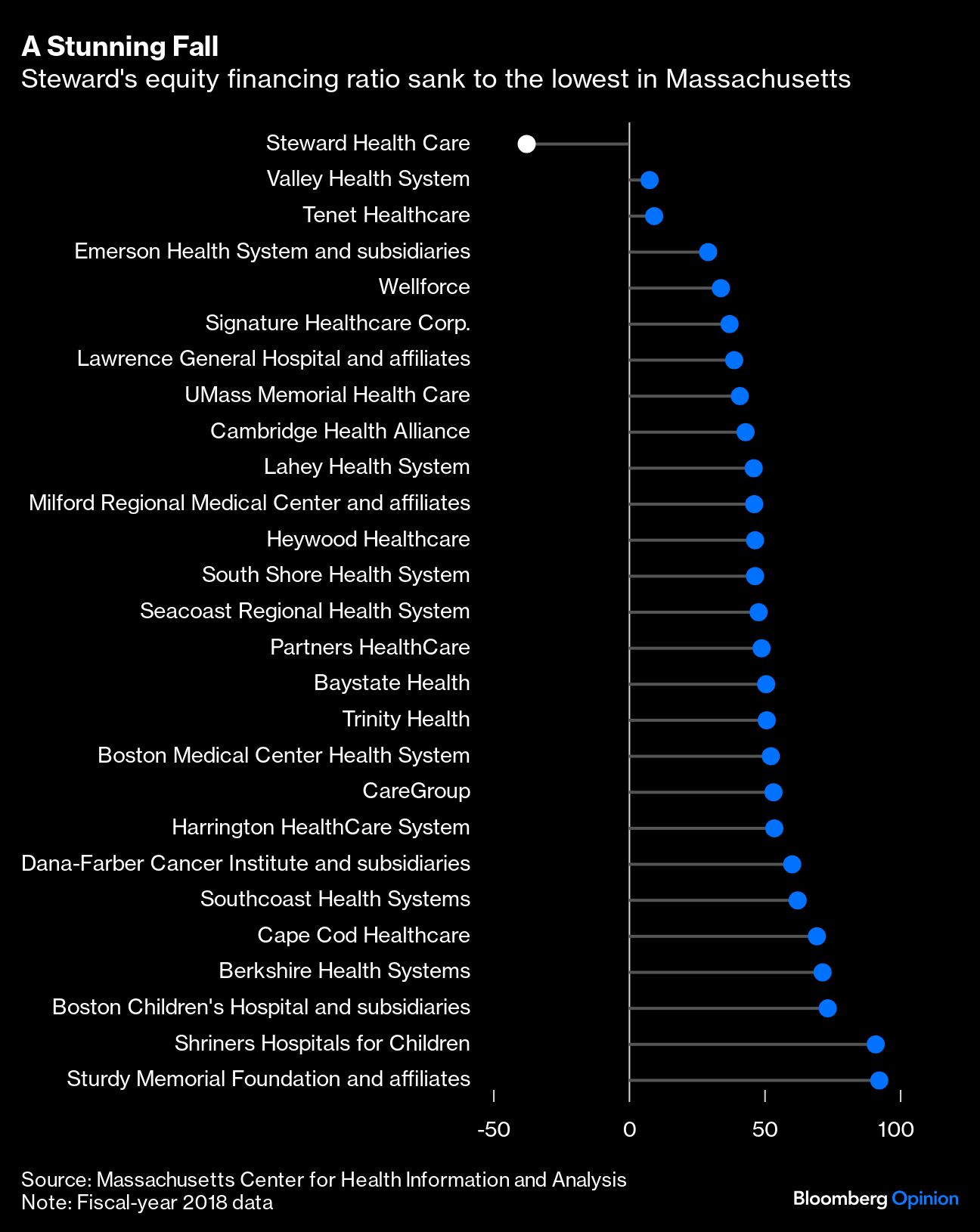

Lawmakers also must be alert to excessive debt. When Cerberus bought Caritas, it assumed $275 million in debt and $200 million in pension liabilities; by 2018, Steward’s equity financing ratio had sunk to the lowest of any hospital system in the state. Curbing risky practices, such as borrowing to repay investors quickly, and reducing tax advantages that encourage outsized leverage should also be a priority.

In the best of times, the American health-care market is a marvel of complexity, hidden costs and opaque incentives. The more policymakers can shine a light on this system, the better — especially when patients’ lives are on the line.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.