Its business is massive, its profits are booming and everyone already knows Nvidia Corp. is the hottest stock on Wall Street.

And yet many investors are betting the rally in the world’s most valuable chipmaker still has room to run.

For more than a year, Nvidia has sailed past earnings and share-price expectations. On Sunday, the company announced plans for new chips to stay ahead of the competition. On Monday, Bank of America analysts lifted their price target, once again, to a Street-wide high of $1,500, saying Nvidia’s premium is justified by its growth outlook. On Wednesday, its stock pushed deeper into record territory, rising as much as 2.7% to $1,195.48 in New York trading.

“It’s like trying to catch a marathon runner that’s running at full speed,” said Adam Gold, founder and chief investment officer at Katam Hill LLC. “They’ve been in the race for a long time. At the moment they’ve got a big lead and they’re poised to extend it this year and next year.”

Gold has owned Nvidia shares since 2016. It is now his largest position, and he keeps adding to it.

Gold is part of a Wall Street consensus that Nvidia’s lead is unassailable, at least for now. Rivals haven’t been able to catch up to Nvidia with chips that power artificial intelligence workloads, known as accelerators.

Its rapid growth in that space has transformed Nvidia from a niche maker of graphics processing units used for gaming to the third-most valuable company in the world. It is now worth $2.94 trillion, having added more than $2 trillion of that since a landmark earnings report sent its stock into the stratosphere last year.

The day after Nvidia unveiled its latest chip plans, Advanced Micro Devices Inc. said it’s speeding up introductions of its own. On Tuesday, Intel Corp.’s chief executive spoke about new products as well. But none of Nvidia’s competitors are close to its dominance in AI.

Its recent earnings report showed customers are still snapping up its current H100 chips despite a more advanced chip called Blackwell coming later this year. Capital spending forecasts from major technology companies revealed that they plan to spend even more than previously anticipated on AI computing infrastructure.

“The only thing stopping them from selling any more is supply,” said Michael Kirkbride, partner and portfolio manager at Evercore Wealth Management.

Visibility from Nvidia’s biggest customers and rising demand from other industries makes its valuation “really reasonable,” he said. “We continue to be buyers.”

Few Naysayers

The scale and pace of Nvidia’s rise has generated some caution and even skepticism. But so far the naysayers keep being proven wrong.

Take Rob Arnott, who’s been warning of a Nvidia bubble since at least September. He compares its rise to other tech darlings that shot to glory only to see their products’ relevance evaporate: the PalmPilot overshadowed by the BlackBerry, which, in turn, was annihilated by the iPhone. Arnott views Nvidia as no different.

“When narratives get ahead of themselves is when they extrapolate recent trends into the future,” Arnott, founder and chairman of Research Affiliates LLC, said in an interview. “Nvidia’s sales doubled in 12 months. Fantastic. How long does that persist?”

Others express a mixture of worry and surprise at Nvidia’s success, but say they cannot help but be buyers of the stock. For instance, JP Scandalios, senior vice president and portfolio manager at Franklin Equity Group, gets a little rattled when friends or Uber drivers or barbers want to talk to him about Nvidia — that type of enthusiasm usually puts him on guard. Nonetheless, he remains bullish because of the eye-popping numbers on his screens.

“That kind of hype always makes me a little nervous,” he said. “But I come back to my model and look at the discounted cash flow and you go, they have a dominant share and if anything seem to be accelerating the pace of innovation. The numbers have just become staggering very quickly.”

Climbing Estimates

Analysts expect Nvidia’s net income to jump to $65 billion, on average, in the current fiscal year from $30 billion the year before, according to estimates compiled by Bloomberg. Those projections have risen 10% in just the past month.

Importantly, Nvidia is not just growing profits but profit margins, showing its pricing power as revenue shoots higher. Analysts expect Nvidia’s gross margin — the percentage of revenue that remains after production costs — to rise to 76% this fiscal year, up from 59% two years ago.

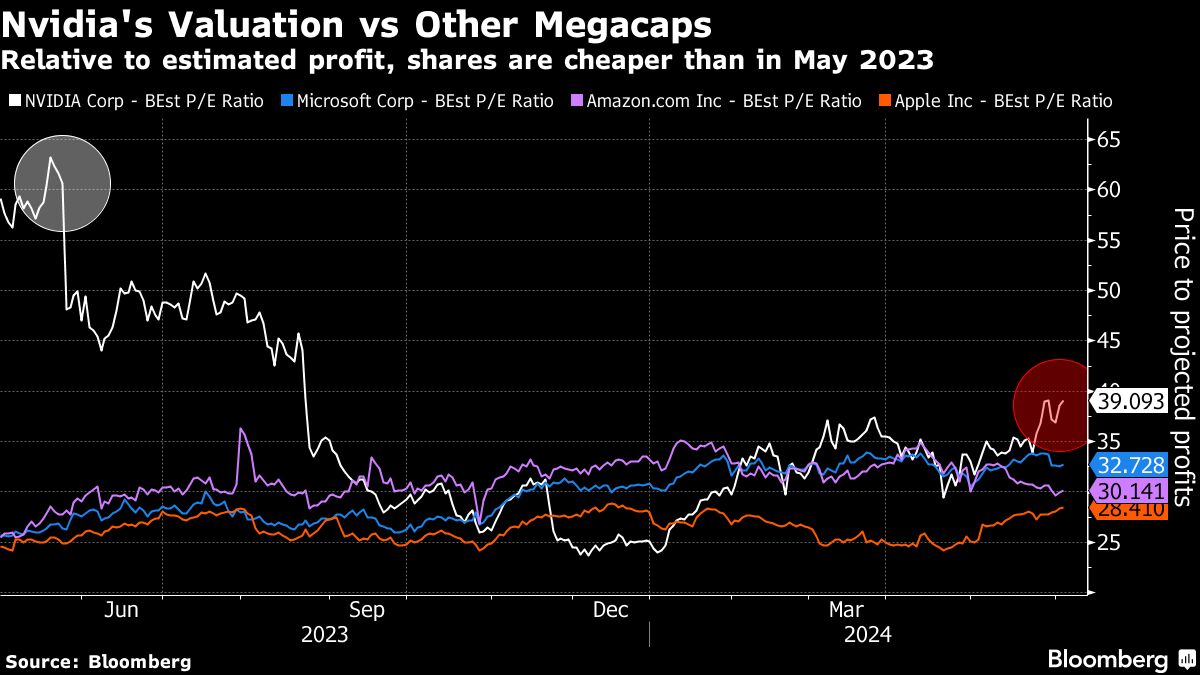

While Nvidia shares are relatively pricey at 39 times profits expected over the next 12 months, they are much less expensive than the multiple of 60 they were trading at before its May 2023 earnings report.

The ratio change is a function of analysts’ profit estimates rising even faster than the stock. That makes Nvidia attractive compared with other big tech names like Microsoft Corp., which is priced at 31 times future earnings, said Michael O’Rourke, chief market strategist at Jonestrading.

“For a similar valuation, you’re getting so much greater growth with Nvidia,” he said. “There’s no competition for that kind of fundamental growth in a megacap company.”

Of the 72 analysts tracked by Bloomberg who cover Nvidia’s stock, 65 rate it a buy and none rate it a sell.

Even Arnott, the Nvidia bear, describes it as “a wonderful company with phenomenal products.” He just can’t help feeling like he’s seen this movie before.

“Bubbles continue until they don’t,” he said. “The best thing to do in a bubble is stay the course, ride with the herd as long as you know when the bull is going to signal. There’s the challenge: it’s almost impossible to know when a bubble will have run its course.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of ourwebcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.