Bond traders who have come to terms with the prospect of higher-for-longer interest rates through 2024 are looking toward this week’s Federal Reserve meeting for clues on how to game out 2025 and beyond.

Treasuries inched higher on Tuesday as investors look to parse policymakers’ latest quarterly economic and interest rate projections — known as the dot plot — on Wednesday. As of March, officials were signaling three quarter-point cuts in 2024, but they’re expected to scale back that forecast in the face of a barrage of robust economic data, including strong May jobs growth.

Just hours before the Fed wraps up its two-day meeting, a fresh read on inflation will likely show prices running well ahead of the central bank’s comfort zone. With the data giving the Fed little leeway to cut rates soon, investors are now debating whether future easing will amount to only a smallish tweak of policy into next year, as opposed to the series of reductions many had been expecting. The difference may have big market consequences.

“We’re going to quickly turn the page to 2025,” said Kevin Flanagan, head of fixed income strategy at WisdomTree. “Maybe we get one or two cuts this year, but how many are we going to get next year?” said Flanagan. “That will quickly become the center of attention as we move into the second half of this year.”

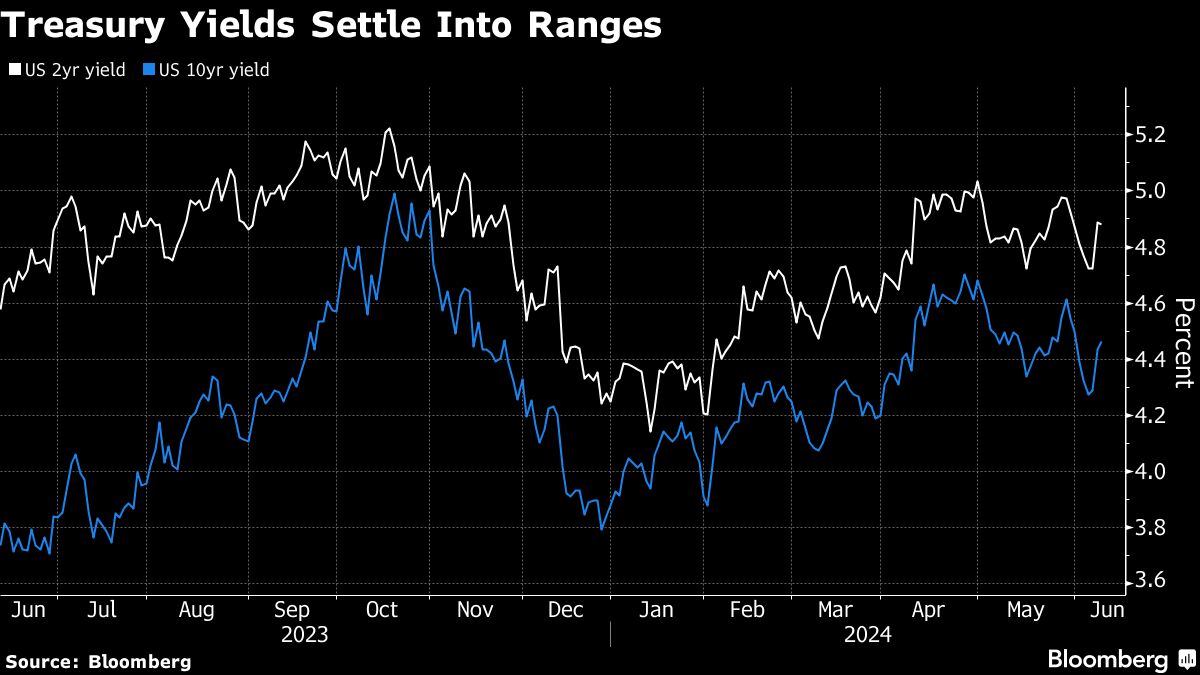

The Fed has maintained a two-decade-high policy-rate range of 5.25% to 5.5% since July as the economy has held fairly strong, leaving two-year Treasury yields hovering just below 5% and 10-year rates at around 4.5%.

While the market is pricing in less than two quarter-point rate cuts for this year, the general thinking has been that an easing cycle would kick in as the economy eventually cools. On the margins, that’s starting to change.

Trades positioning for Fed policy rates staying elevated well into next year and 2026 have picked up via recent interest-rate option trades. Options traders are more hawkish than their counterparts in the swaps market, with March 2026 options targeting a Fed rate of roughly 5.75% while swaps indicate a rate around 4% by that time.

Jean Boivin, head of the BlackRock Investment Institute said the bond market should be wary of anticipating that “a delayed easing cycle” will finally arrive given the likelihood that inflation averages above the Fed’s 2% target. He said the bond market faces the prospect of “adjusting to the realization that this is a shallow cutting cycle.”

The March dot plot saw the Fed moving the policy benchmark down to 4.6% in December and then to 3.9% by the end of 2025, according to the median forecast. It wouldn’t take many officials becoming more hawkish on their rate outlook to move the median projections higher. Only a narrow majority signaled they expected to cut rates three times this year, with nearly half of policymakers preferring two or fewer reductions in 2024.

“It’s the dots that matter,” said David Robin, a strategist at TJM Institutional who’s been working in debt derivatives markets for decades. “It’s either two moves or lower. And we would not at all be surprised to see at least two or three dots move to one or none for 2024.”

The resilience of the economy and loose financial conditions in spite of a 5% plus Fed funds rate has spurred chatter that policy isn’t truly restrictive and may need to rise.

“The debate on whether policy is restrictive or not will continue as the data is mixed on the whole,” said Priya Misra, portfolio manager at J.P. Morgan Asset Management. “There is strong labor supply but consumer confidence and hiring intentions from small business is weakening.”

As for the dots, she expects the FOMC to signal a median of two cuts for 2024 and three cuts in 2025, with “chair Powell to emphasize that the dots are not a forecast but a function of the data.”

Higher Long-Term Rates

Mark Dowding, chief investment officer at RBC BlueBay Asset Management, is focused on the Fed’s so-called terminal rate, which he thinks is too low at 2.6%. Fed officials in March lifted their outlook for the long-run policy benchmark to 2.6% from 2.5%.

“We’re now in a world where inflation continues to overshoot,” and that long-run dot shifts toward 2.75% on a “journey somewhere north of 3%.”

A market aligned closer to the Fed’s expectations for the rate path leaves Dowding advocating caution over longer-dated Treasuries, “largely because of debt levels in the US.”

For that reason, he favors a so-called steepener trade — where short-term yields decline faster than those on longer-term debt — although that positioning has failed to work lately. “Eventually we think the chickens will come home to roost there and you’ll see some steepening of the curve,” he said.

Kristina Hooper, chief global market strategist at Invesco, said she doesn’t anticipate a very aggressive rate-cut cycle. Instead, she sees a “more gradual” pace that will support an environment for risk assets and a re-acceleration in economic growth.

“Every day that goes by that the Fed doesn’t cut there’s a psychological and a real impact to the economy,” Hooper said Monday on Invesco’s mid-year outlook call. “Having said that though, I do think that the US economy has been resilient.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Michael Mackenzie, Liz Capo McCormick