Wednesday is shaping up to be a doozy in the US bond market. Following the release of the consumer price index at 8:30 a.m. in Washington, investors will turn to the Federal Reserve’s policy rate decision at 2 p.m., which includes an update to policymakers’ carefully scrutinized economic projections. That should create plenty of volatility, but it may prove meaningless as to the ultimate trajectory of interest rates.

Over the past two and a half years, the median CPI report has been good for an 8-basis-point swing in 10-year Treasury yields, and the median Fed day has produced a 5-basis-point move (irrespective of sign). Yet, that probably understates the circus of it all, because markets have often taken off in one direction upon the release of Fed policy decisions, only to completely reverse direction moments later during Chair Jerome Powell’s post-decision press conferences. In Wednesday’s back-to-back, you could see an especially big move in one direction, or perhaps a sequence of offsetting developments that take us on a roller coaster ride to nowhere.

This sort of manic behavior won’t tell us much about the big outstanding question for the US economy: Will inflation return to the Fed’s 2% target, allowing the central bank to reduce rates before tight monetary policy causes a recession?

Consider the consumer price index. Month-to-month inflation reports are always noisy, but the signal in the data has been especially faint in recent periods. Shelter and insurance inflation have kept the overall core CPI numbers relatively high due to lags inherent to those particular categories, even though there are good reasons to expect them to abate in the medium run. Inflation in new housing leases has long ago cooled, yet landlords have raised rents on existing tenants more slowly and are still playing catchup.

In motor vehicle insurance, companies have lifted premiums to account for past inflation in the underlying cost of autos, parts and repairs, yet that occurs with a lag as well due to heavily regulated pricing. Allstate Corp., for instance, said on an investor conference call last month that it had achieved “rate adequacy” in many states but that it was still pursuing increases in others, including a 13.9% increase coming to New Jersey in the second half of the year. Policymakers are sure to welcome any signs that housing and insurance inflation are finally fading, but they broadly expect it will take some time.

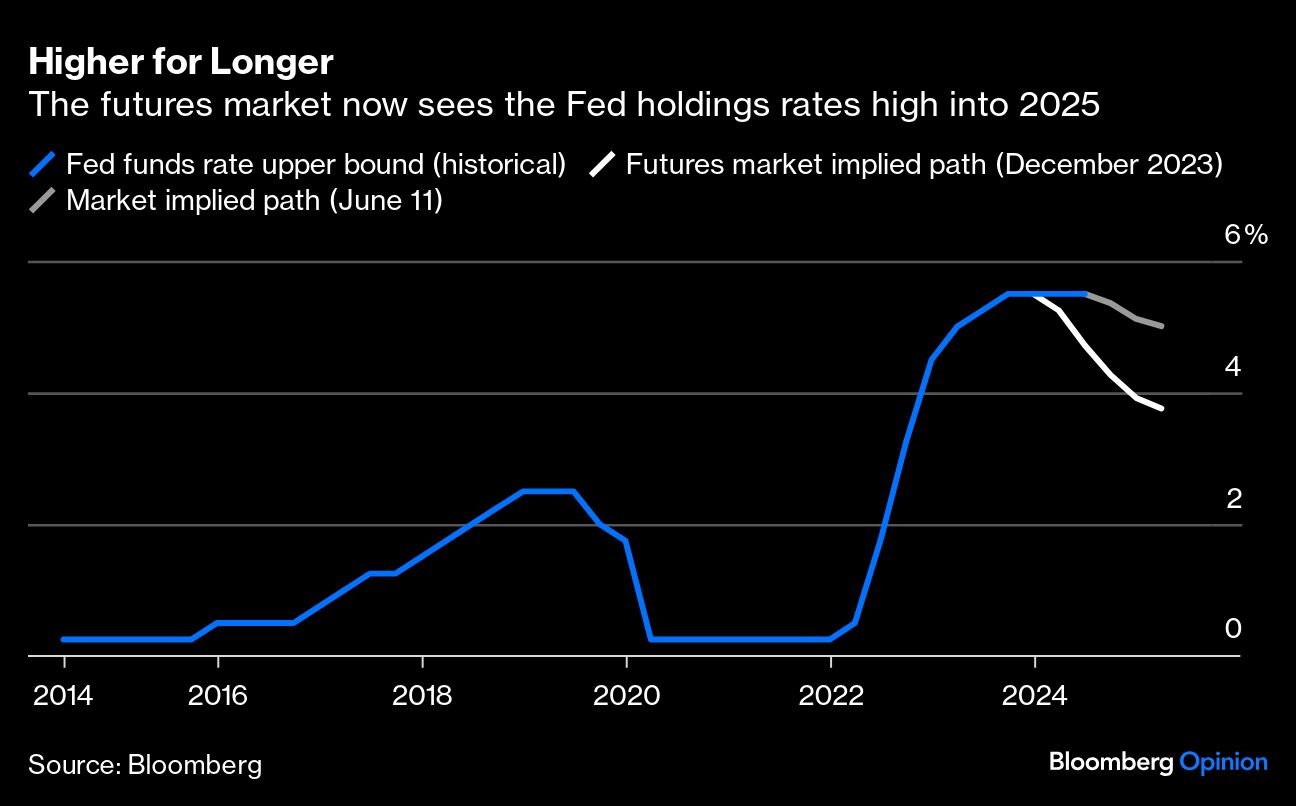

Next, there’s Fed communication to consider. Markets will pay particular attention on Wednesday to the Fed’s Summary of Economic Projections, a quarterly compendium of economic outlooks submitted by Federal Reserve Board members and Federal Reserve Bank presidents. Traders want to know whether policymakers still expect three rate cuts this year (futures markets are expecting just one or two); how quickly they expect to reduce policy rates in 2025 and 2026; and where they might land benchmark rates when all is said and done. Unfortunately, of course, policymakers’ crystal balls are just as hazy as everyone else’s.

So what does matter?

Powell is understandably looking for additional evidence that inflation is still on its long, albeit slow, path to moderation. That would amount to a core CPI report devoid of new surprises. The same old pain points may persist, but I’d get a bit nervous only if inflation started creeping into new categories. You’d particularly like to see signs from the more vanilla consumer services areas (restaurants, haircuts and the like) that inflation is moderating, and that wage pressures aren’t putting a floor under prices.

Shelter inflation will need to step down eventually to get inflation back to target, but Inflation Insights LLC President Omair Sharif projects that may not start happening until June (with the data released in July). He’s keeping an eye on the Bureau of Labor Statistics’ All Tenant Regressed Rent Index, which will get updated again in July and tends to provide strong signal about where CPI rents are going.

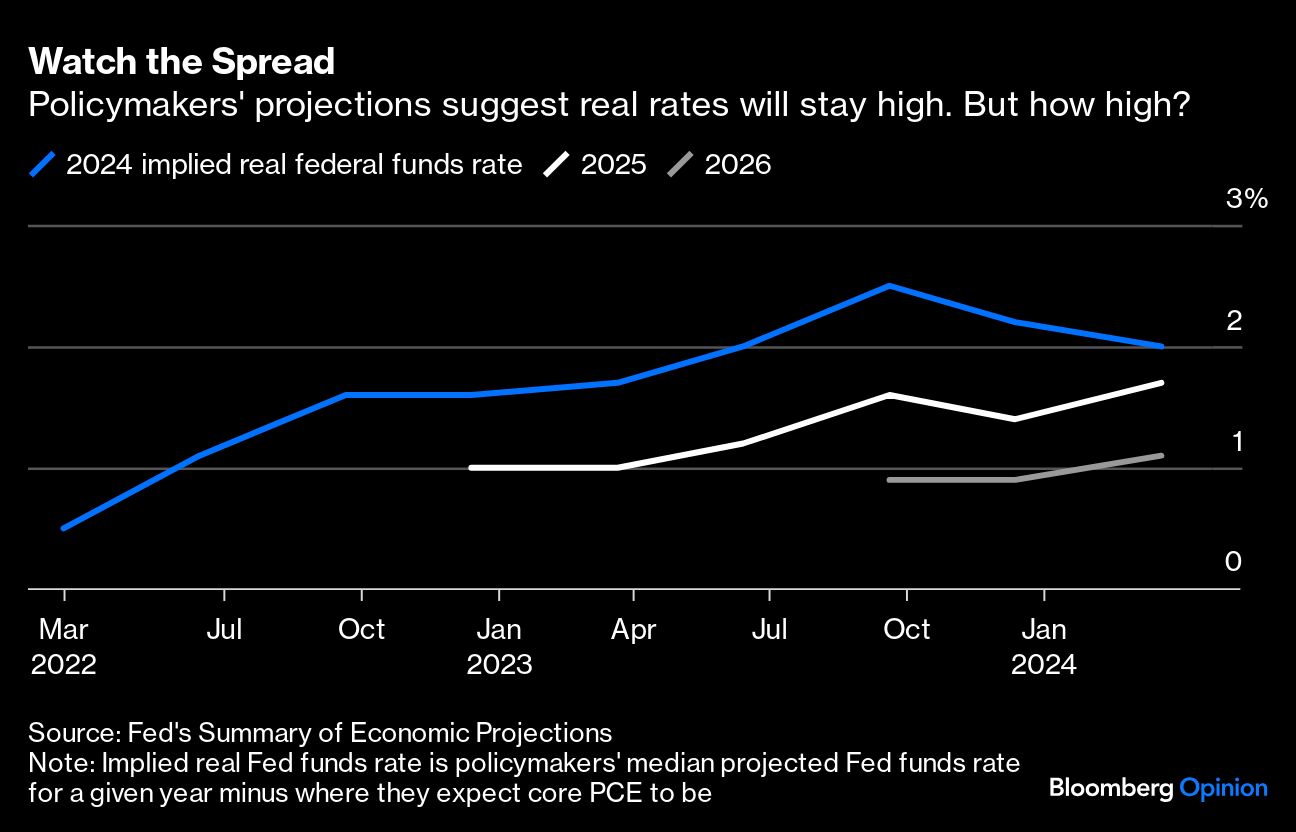

In the Fed’s projections, I tend to believe that real rates matter more than nominal ones, since policymakers’ inflation outlooks are as fallible as everyone else’s. In the last SEP, the median policymaker saw the federal funds rate ending 2025 at 3.9% even as core PCE inflation returned to 2.2% — a 1.7% implied real rate. Frankly, that feels a bit extreme for a 2025 environment in which inflation is projected to be a whisker away from target, and real rates should therefore return to a longer-run neutral rate of somewhere in the 0.5%-1% range. Still, it’s been a fool’s errand to bet against Fed resolve. If policymakers are coalescing around the need for tight policy irrespective of realized inflation, that will have important implications for government borrowing costs, mortgages and corporate finance going forward, and we all have to pay attention.

Ultimately, though, the bond market’s big day is shaping up to be a festival of overreaction, with too much focus on the headlines and too little on the nuances that really matter.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin