Bond traders loaded back up on interest-rate-cut bets — and even the pushback coming out of the Federal Reserve did little to shake their conviction.

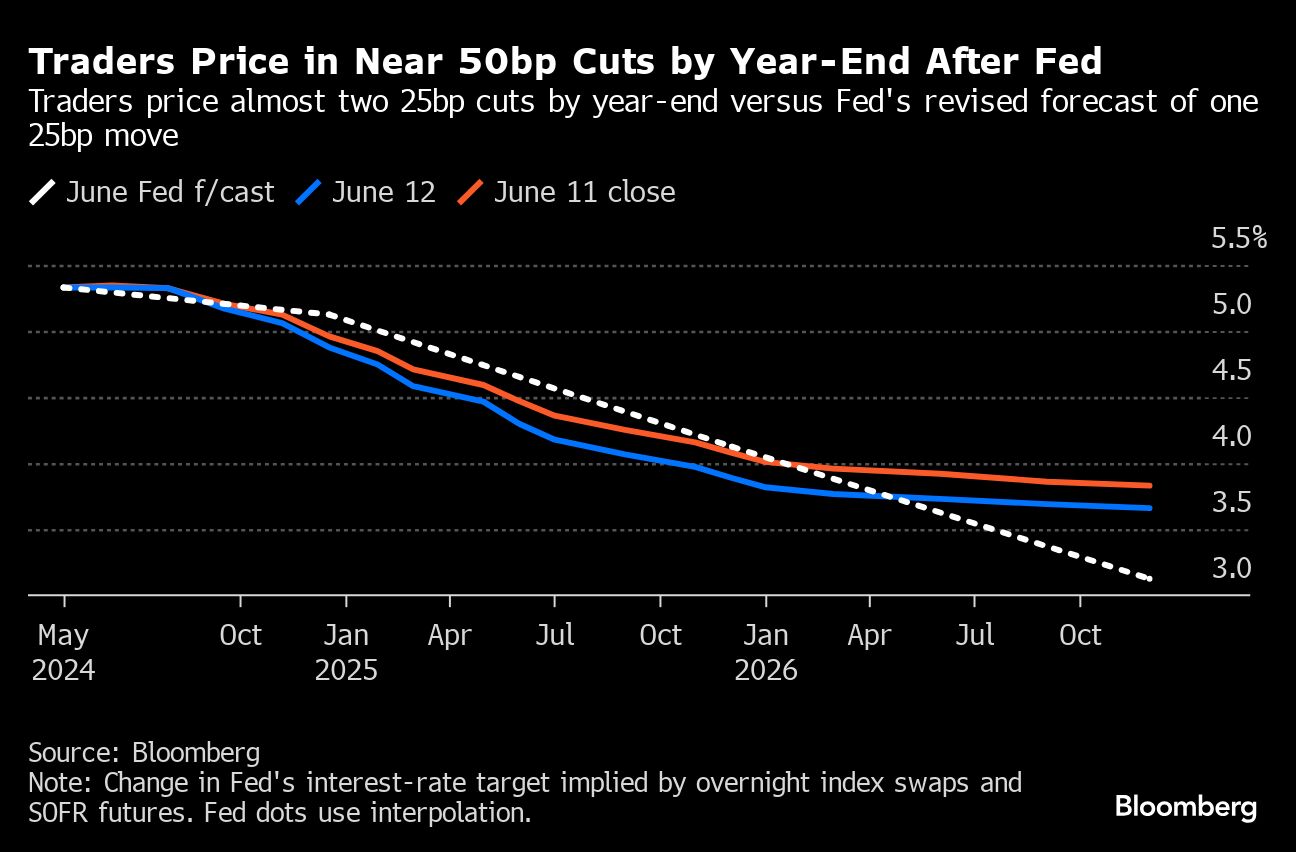

Policymakers kept rates steady at a more than two-decade high on Wednesday and dialed back their forecasts to pencil in just one quarter-point rate cut by year end, about half of what markets are pricing in. At his post-meeting press conference, Jerome Powell stuck to the message that the central bank is in no rush to shift gears, waiting for more evidence that its fight against inflation is moving in the right direction.

But the morning’s consumer price index report had already delivered what traders were waiting for, setting off a bond-market rally by showing that a key measure of inflation cooled to the slowest pace in more than three years.

The gains were extended in early trading Thursday after producer prices provided further evidence of disinflation and the number of weekly jobless claims exceeded forecasts. The 10-year Treasury yield slid 5 basis points to 4.26% as traders stepped up bets that the Fed will cut rates by half a percentage point this year, seeing Powell’s hawkish talk as just a signal that the central bank doesn’t want to be boxed in.

“Powell clearly wants to retain optionality,” said Michael de Pass, global head of rates trading at Citadel Securities. “Powell wanted to come across more even handed and make sure he didn’t fan the flames following the softer-than -expected inflation print.”

The markets, of course, have jumped the gun repeatedly in recent years, anticipating that a Fed pivot was imminent only to be whipsawed by another painful reset when the central bank held its course.

Policymakers have made it clear, though, that they’re ready to start dialing back rates once they’re confident that inflation is comfortably receding back to their 2% target.

Prices are still rising faster than that, which Powell said justifies the central bank’s restrictive policy stance. But he also said the job market is no longer overheating — pulling back to its pre-pandemic state — and underscored that the Fed is watching for the downside risks of an economic slowdown.

“We’re kind of seeing what we wanted to see, which was gradual cooling in demand,” he said.

He said that ultimately rates will need to come down to keep supporting the economy but there’s been no need to do so yet. “We’ll have to see where the data light the way,” he said.

What Bloomberg’s Strategists Say....

“A much lower-than-expected CPI drove punters into an asset-buying frenzy, for understandable reasons given the abrupt shift in both the surprise and the direction of key measures. Yet on the surface the dot plot and economic projections were quite hawkish, with inflation forecasts ratcheted up and the 2024 Fed funds median firmly ensconced at 5.125%. Even taken at face value, the dot plot is arguably less hawkish (in terms of reaction function) than the previous couple. Add in the prospect of another dovish tilt should the downturn in the inflation trajectory persist, and the CPI reaction looks like the right one.”

— Cameron Crise, strategist.

The CPI figures were seen as an encouraging sign by traders who were burned by a series of stronger-than-expected readings at the start of the year, as well as by the selloff that raced through the bond market Friday after a surge in job growth.

The Wednesday report showed that core inflation — which excludes volatile food and energy prices — was up 3.4% from a year before, the slowest advance since April 2021. That drove futures traders to price in strong odds that a first rate cut could come as soon as September.

“I got the impression that the Fed will pivot fast once the jobs market shows a rapid deterioration,” said Akira Takei, a fixed-income manager at Asset Management One Co. in Tokyo. “I don’t think the market has priced in that risk,” said Takei, who has overweight positions in five- to 10-year Treasuries.

The gains largely held after officials’ median estimates showed they expect just one cut this year, though that was partially offset by the addition of one more move to the 2025 outlook.

Powell seemed to endorse the market’s skepticism by downplaying the importance of the rate forecasts, saying the actual path will depend on future economic data. He said that the May inflation data was “welcome” and officials “hope for more like that.”

“Powell came across more hawkish,” said George Goncalves, head of US macro strategy at MUFG. “This is just an attempt to try to get the focus away from timing of the first cut.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Michael Mackenzie