Treasuries Are a Whisker Away From Erasing This Year’s Loss

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsUS Treasuries are on the brink of breaking even during a roller-coaster first half of the year.

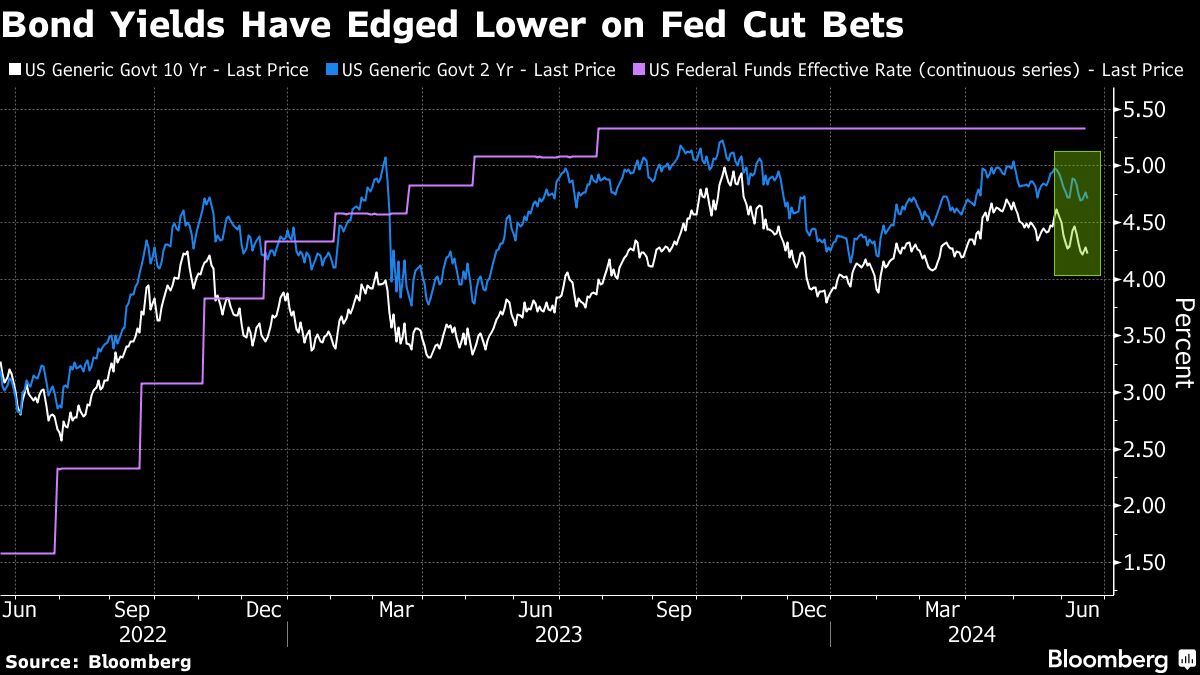

A Bloomberg gauge of returns in the world’s biggest bond market was down just 0.1% in 2024 through Tuesday after having lost as much as 3.4% for the year in April. The loss may endure for at least another day, however. Yields climbed as US markets reopened after a holiday despite weaker-than-anticipated housing starts data for May.

At the heart of the market’s recovery from the April nadir are investor bets that cooling US prices will convince the Federal Reserve to cut interest rates sooner and by more than officials have signaled, effectively putting a lid on how high Treasury yields can climb.

“We’ve seen the peak in yields,” said Stephen Miller, four-decade market veteran and investment strategist at GSFM in Sydney. “Bonds are now back as having a deserved place in a multi-asset portfolio.”

Treasuries have been whipsawed this year, with policy-sensitive two-year yields surging above 5% in April as investors anticipating indefinitely elevated Fed rates dumped bonds. They’ve since dropped back under 4.75%, after inflation and retail sales data suggested the world’s biggest economy may finally be cooling enough to warrant lower borrowing costs.

Traders are positioning for the Fed to make about two-quarter point cuts this year, with the first one fully priced in for November, based on swaps. That’s despite comments by Fed officials Tuesday that more evidence of slowing inflation was needed in order to cut rates.

Fed Governor Adriana Kugler said it will likely be appropriate for the central bank to reduce rates “sometime later this year” if economic conditions unfold as anticipated. St. Louis Fed President Alberto Musalem said in his first major policy speech that it could take “quarters” for the data to support a cut.

Lower Volatility

Rachana Mehta sees the Treasury 10-year yield in a broad range of about 4.2% to 4.5% with movements toward the top of that a good window to buy.

“The volatility we saw in the past, hopefully it has died down given the recent US data,” said Mehta, co-head of regional fixed income at Maybank Asset Management, speaking in an interview with Bloomberg Television. “You can continue to be long duration at about 4.4% to 4.5% in 10-year Treasuries.”

Volatility in the $27 trillion Treasury market has fallen from its recent highs as the views of the Fed and investors over the number of rate cuts expected this year have begun to coalesce. The ICE BofA MOVE Index — a gauge of bond volatility that tracks anticipated swings in US yields based on options — is hovering at about 98, down from an April high of 121.

“The key thing here is that that spread between market expectations and what the Fed is pricing has narrowed,” said Desmond Fu, a portfolio manager at Western Asset Management in Singapore. “That reduces volatility.”

Not everyone sees upside for Treasuries. Strategists at Barclays Plc earlier this month recommended switching back to shorting the 10-year note as they wager on a rebound in US economic activity.

Core PCE

Swaps traders, meanwhile, see a more-than-60% chance the Fed may cut rates as early as September.

The market is keenly focused on the June 28 release of the central bank’s preferred inflation gauge, predicted to show a “very subdued” pace of price pressures in May, according to Padhraic Garvey, head of global debt and rates strategy at INF Financial Markets.

The personal consumption expenditures core price index will fall to an annualized pace of 2.6% in May, according to the median estimate of economists surveyed by Bloomberg. That would be the lowest since 2021.

“That will harden the build of a rate-cut discount for September,” New York-based Garvey wrote in a note with his colleagues. “We continue to eye 4% as a viable target” for the 10-year Treasury yield, he said.

Credit Outperforms

So far this year, corporate bonds fared better than Treasuries. They’ve generated an excess return over their government peers of 1.32%.

But that’s down from a high of 1.74% at the end of May, according to a Bloomberg index.

Company bond spreads have widened in June as the same signs of economic weakness that have boosted Treasuries keep credit risks alive — particularly among weaker borrowers.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All