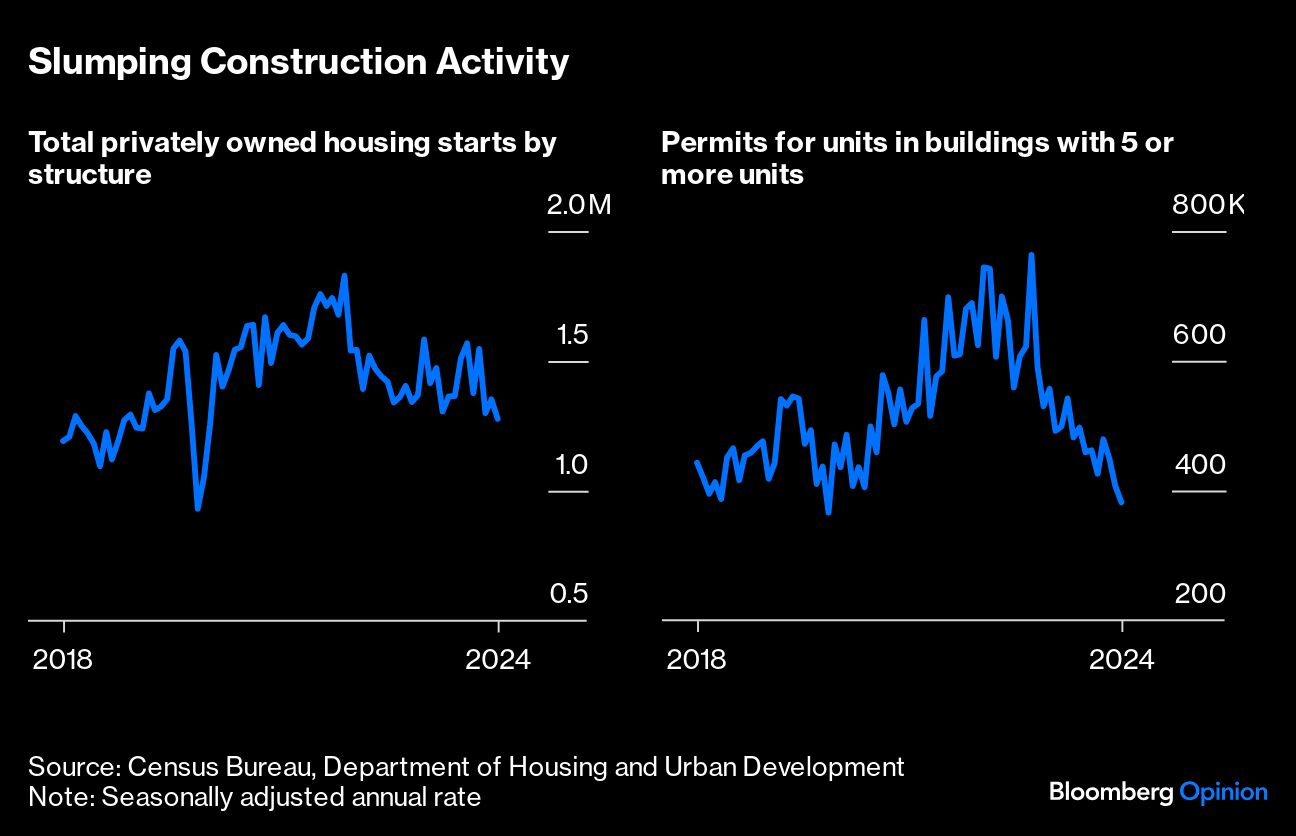

New home construction slumped to the weakest level in four years in May, confirming a trend that’s been evolving for the past few months — residential construction is once again acting as a drag on economic growth in the US.

This should give the Federal Reserve more confidence that it’s appropriate to cut interest rates later this year. But it’s bad news for those hoping for an increase in supply to address America’s structural housing shortage. And it’s particularly bad news for communities dependent on smaller builders for more housing construction.

To understand why construction starts are sputtering, it’s helpful to treat single-family and multifamily housing separately. The story in the multifamily segment is by now a familiar one: Developers built a ton of apartments in fast-growing metros in 2021 and 2022 when borrowing costs were low and rent growth was surging. We’re temporarily in a rental market downturn as that supply gets absorbed.

Multifamily building permits fell in May to near their lowest level in a decade, and new construction is likely to remain low well into 2025. This is because there’s still a historically high number of units under construction, and developers — and their financiers — likely won’t have the confidence to begin a new building cycle until that number normalizes somewhat and rents grow more strongly. The decline in activity should have a modestly negative impact on construction employment and economic growth, adding to the case for rate cuts from the Fed.

In single-family housing, the story is largely one of stability. New builds are no longer the only game in town — as they were in 2023 — with rising inventories of existing homes for sale making the market more competitive, particularly in places such as south Florida and Texas. At the same time, stubbornly high mortgage rates at around 7% have sidelined many buyers. Builders are responding to the subdued demand with steady to lower output compared with the burst of activity that came last year when interest from buyers was surprisingly buoyant. Hopes that strong single-family-construction growth would help fill a housing deficit of about 2 million homes have been dashed, at least with interest rates at current levels.

Behind the scenes, the industry is in a state of flux. Large, publicly traded firms, with economies of scale and access to cheaper capital, are growing market share while smaller, privately held homebuilders are struggling in the more competitive environment.

In the aggregate, single-family housing starts fell 1.7% year-over-year in May. Yet Lennar Corp, the second-largest homebuilder in the US, said last week that new orders were up 18% year-over-year in the second quarter, while KB Home reported a 2.6% increase. DR Horton, the largest homebuilder in the US, saw orders rise 14.3% year-over-year in the first quarter.

If the nation’s two biggest developers are reporting double-digit order growth when single-family housing starts are shrinking, it means everyone else is losing ground. An index measuring sentiment among members of the National Association of Home Builders — where the median member constructs just six residences per year — declined in June to the lowest level in 2024, pressured by a triple whammy of higher rates, labor shortages and a dearth of buildable lots. Large firms are now reaping the benefits of fortifying their balance sheets and streamlining processes and supply chains over the past two years, something many small developers have been unable to do.

This matters at the local level because the biggest builders tend to operate in lower-cost, faster-growing metro areas. Lennar and DR Horton gaining share at the expense of smaller builders is fine if you live in Florida — you’ll just get a Lennar-branded home instead of one from someone else. But these builders don’t operate in the Northeast or even in a big state such as Michigan. The fallout of the 2008 subprime mortgage crisis is instructive here: Back then, a recovery in housing construction was delayed by the collapse of smaller firms. Today, the risk is that the same thing happens in housing markets dominated by small builders.

The Northeast is a particularly acute example of this. States such as New York and Connecticut currently have some of the strongest rent growth in the country because they never saw the pandemic supply boom that swept through Sun Belt metros. Single-family inventory levels in many parts of the Northeast are 70% or more below pre-Covid levels. Yet building permits in the region remain very low, showing that neither low supply nor rising prices have led to an increase in construction.

An interest-rate cut from the Fed should revive sentiment among builders, and an easing couldn’t come soon enough for the most supply-constrained areas. What’s becoming clear is that higher-for-longer interest rates means lower-for-longer housing construction.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out ourvideos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.