Norinchukin Bank is best known outside of Japan as an investing whale in the market for bonds that package up loans to private equity businesses, known as collateralized loan obligations. But it’s the firm’s bets on safe, vanilla government debt that have hurt the lender, in an echo of what happened to some US banks last year.

And, like Silicon Valley Bank, the Japanese lender known as Nochu has given itself a major headache by failing to manage its exposure to interest rates. It’s a fresh warning to others to buck up their risk management as the Federal Reserve looks set to maintain tighter policy for longer.

Losses from Nochu’s bond holdings have escalated to an eyewatering $9.5 billion, it warned last week; luckily, and unlike SVB, its problems seem to be well contained. Other Japanese banks aren’t similarly exposed, and Nochu’s decision to offload $63 billion of its US Treasuries and European government bonds doesn’t seem to have knocked debt markets either.

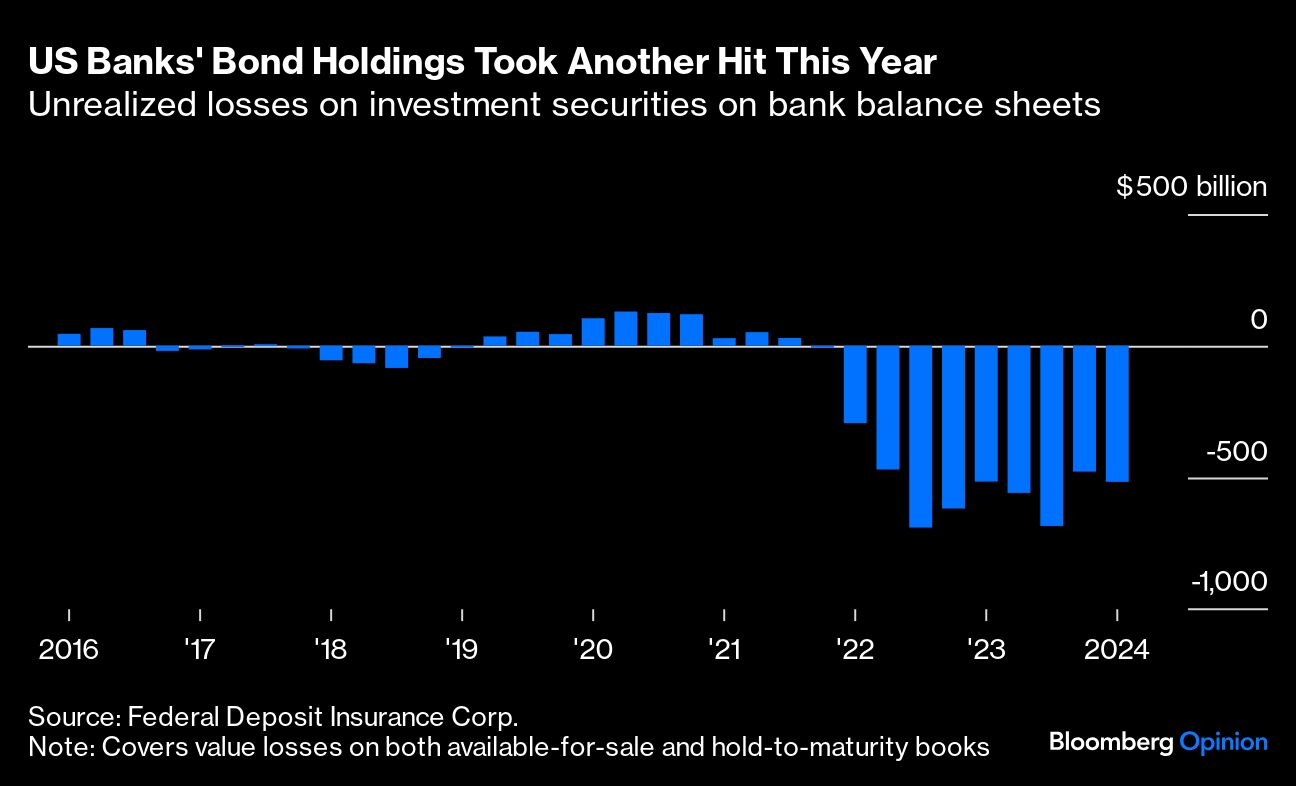

The pain of holding long-term, fixed-rate bonds worsened again in the first quarter of this year after Treasury yields jumped. Total unrealized losses on bonds held by US banks jumped by 8% to $516.5 billion, according to the Federal Deposit Insurance Corp. These moves are still causing problems for smaller US lenders: Bank of Hawaii Corp. was put on review for downgrade by credit ratings firm Moody’s Inc. at the end of May, partly due to its unrealized losses on its fixed-income holdings. The bank raised $165 million of fresh capital last week to bolster its balance sheet.

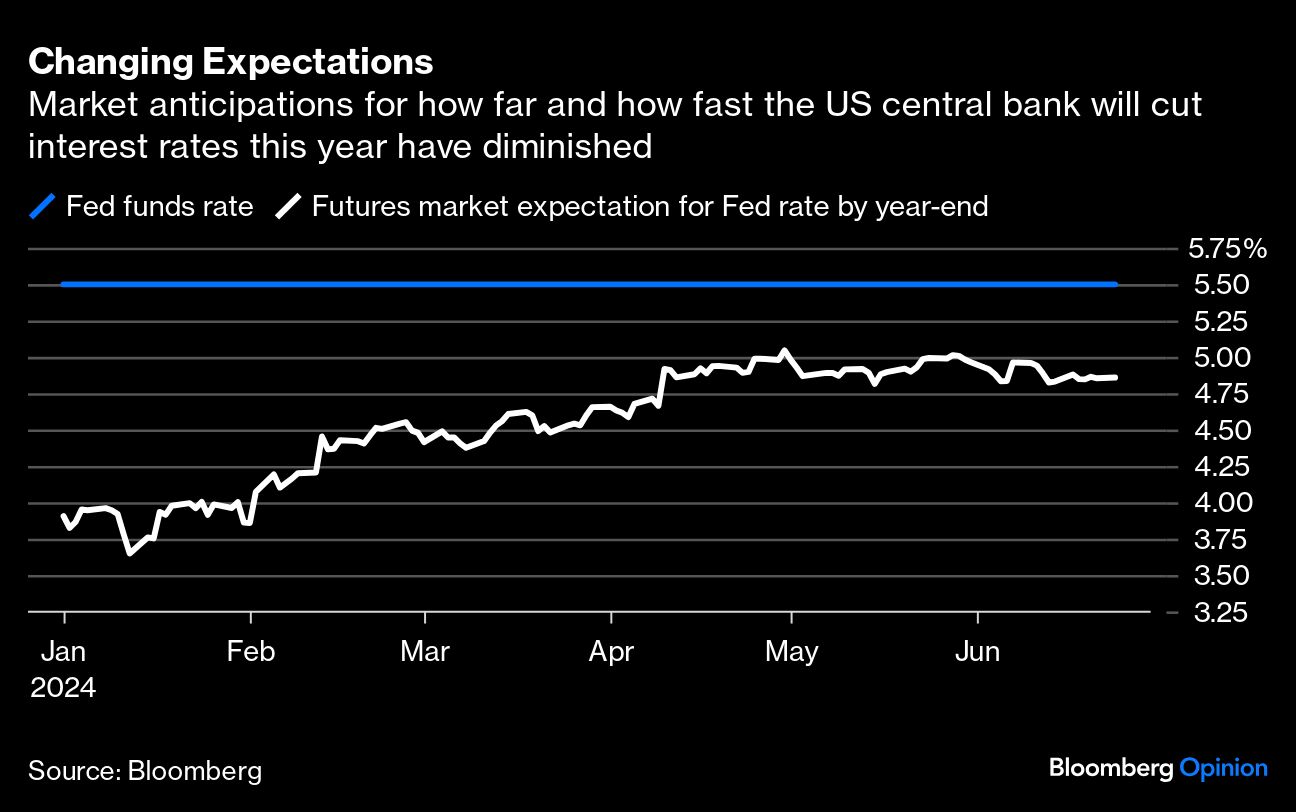

At the same time, expectations for the scale of cuts in official US interest rates collapsed, putting upward pressure on short-term funding costs. In January, the market was expecting nearly 2 percentage points of cuts in 2024, but by the end of March that had halved. Now, 75 basis points of cuts are expected at best.

Nochu took blasts from both barrels: Its holdings of foreign long-term government bonds are funded with short-term foreign currency borrowing, mainly via currency swaps and forwards, repurchase agreements and institutional deposits. It costs more than 5% to fund US Treasury positions from Japan; while that’s down from more than 6% in the middle of 2023, its way above the levels seen earlier in the decade.

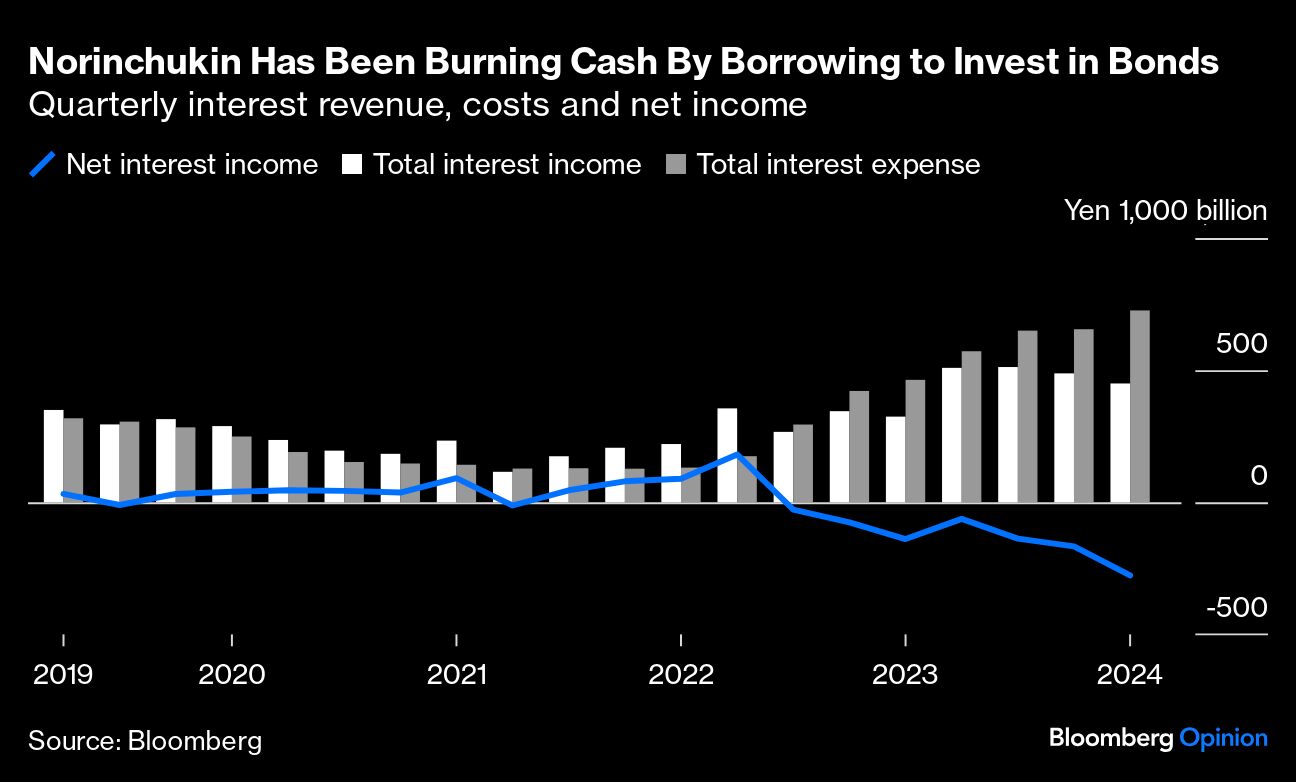

Unlike other big Japanese banks, Nochu has no natural source of foreign currency to rely on because its clients are all domestic agricultural cooperatives who don’t do business overseas. The bank’s stubbornly high overseas borrowing costs have played havoc with its net interest income, which has turned increasingly negative since early 2022.

Meanwhile, declining government bond values have saddled it with growing losses: At the end of March, it was carrying ¥1.8 trillion ($11.4 billion) of unrealized losses on securities, according to its recent full-year results filing. That was up from ¥678 billion a year earlier. Unlike SVB and other smaller US banks, these losses are already subtracted from Nochu’s regulatory capital, so there’s no shock capital hole to suddenly appear for the Japanese bank’s owners.

It’s raising more capital, ¥1.2 trillion worth, but that’s probably to help it move some of its investments into slightly riskier assets with higher capital charges than government debt in order to earn enough yield to cover its funding costs. Still, Nochu might choose to shrink its borrowing and investing activities until the path for US rates becomes clearer, according to Bloomberg Intelligence.

The episode raises two big question: Why is a Japanese farmers’ bank making leveraged bets on foreign interest rates in the first place — and why didn’t it hedge the risks? Answering the first is fairly straightforward: Investment yields in Japan have been terrible for decades, and Nochu has also seen weak demand for credit among its clients in the past couple of years. To generate returns for rural savers, it was forced to look overseas for higher returns.

The answer to why it didn’t hedge its interest rate risk — or didn’t hedge it well — is still a bit of a mystery, as is the question of why it held on to its trades even as losses increased. Other major Japanese banks and insurers dumped large holdings of Treasuries when the Fed started lifting rates sharply in 2022, according to Bloomberg News.

The irony is that if Nochu could hold on to its portfolio for another year or two, rates would very likely fall, bond values would rise and its bets would come good. But it’s costing too much in net interest cash flows for that to be possible. At the start of the year, the bank’s bosses must have thought they’d soon be back in the black; but as US economic strength has kept confounding expectations, those hopes have evaporated.

Some judicious hedging would have solved this problem before it arose. It's amazing that banks big and small keep getting this wrong two years into the higher-for-longer world. And its a warning that even as we look forward to the first Fed interest rate cuts, nasty surprises can still pop up.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul Davies