FedEx Corp. dropped a bomb on the market Tuesday afternoon with the announcement that it will do an “assessment” of its freight unit. Investors seemed to like the move, pushing up the shares as much as 15%, on the possibility of a windfall and a more pure-play package delivery and logistics company. A deal could make a lot of sense.

Certainly, the company’s fiscal fourth-quarter earnings report contained other good news: a 2025 fiscal year earnings-per-share outlook at the midpoint of $21, beating analysts’ midpoint estimate of $20.85; cost cuts of $2.2 billion; and share buybacks of $2.5 billion for the year ending May 31. This is all more proof that Raj Subramaniam is executing well on the transformation plan that he laid out soon after taking over as chief executive officer in June 2022 from founder Fred Smith.

But the highlight was the potential spinoff or sale of the freight unit, which comes a bit out of left field. Still, it’s not a done deal. The move was couched in enough corporate-speak that the company may end up keeping the business if it doesn’t get the right offer:

“FedEx management and Board of Directors are conducting an assessment of the role of FedEx Freight in the company’s portfolio structure and potential steps to further unlock sustainable shareholder value.”

Subramaniam declined to elaborate on a conference call to discuss the company’s results. Still, the most likely outcome will be a transaction to shed the unit, which is the largest less-than-truckload, or LTL, carrier in North America. LTL carriers use a network of warehouses to consolidate smaller shipments of customers’ freight to fill up a full trailer.

If there’s a transaction, it’s likely to be a spinoff, said Lee Klaskow, an analyst with Bloomberg Intelligence. There’s value in the multiple differential. Three of the largest LTL carriers trade at a price-earnings ratio of 26.6 times compared with 13.6 times for FedEx and UPS combined.

“A strategic review of FedEx Freight could unlock considerable value, given the premium that less-than-truckloads are trading at versus parcel carriers and the broader market,” Klaskow said in a note.

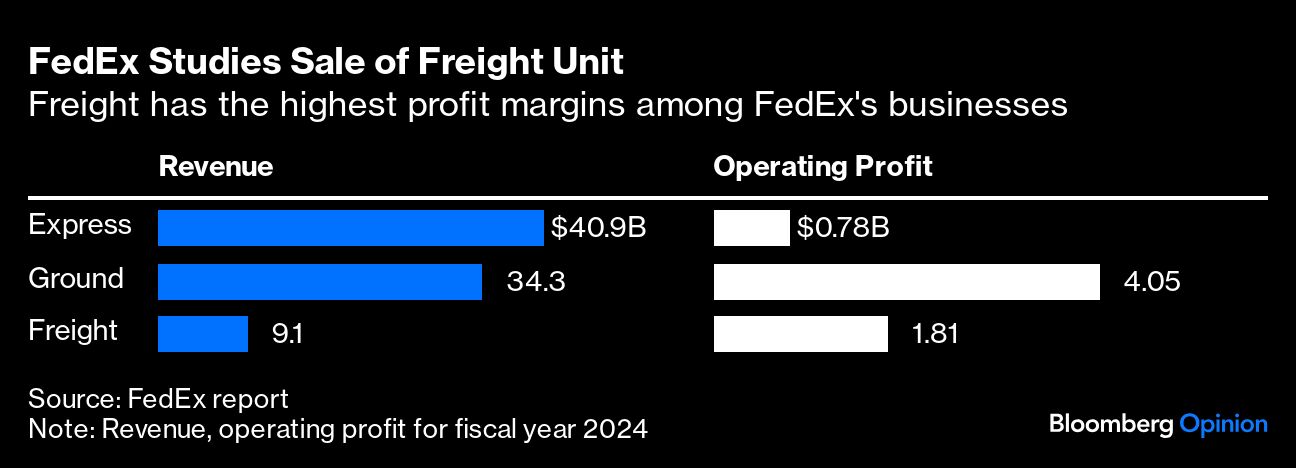

FedEx Freight had sales of $9.1 billion in the 2024 fiscal year and, more important, operating margins of 20%. This margin is much higher than the company’s ground package unit at 13% and 1.9% at FedEx’s struggling Express unit, which is the company’s largest business by sales.

While investors seem to be keen on the value that the courier could unlock through a transaction involving its LTL trucking business, any deal would dilute FedEx’s margins. Think of it this way: Freight contributed $1.8 billion to operating profit in 2024, more than twice as much as the $776 million of operating profit at the Express business for which FedEx is famous.

A deal to sell or spin off the freight unit would make FedEx a more pure-play small-package delivery and logistics company and would follow the lead of United Parcel Service Inc., which sold its LTL trucking business in 2021 to TFI International Inc., a Montreal-based trucking company, for $800 million.

FedEx would fetch many times more than that price for its freight unit: UPS’ unit was much smaller, didn’t make money and had a unionized workforce, which limited the companies willing to bid on the business.

FedEx Freight commands 15% to 20% of the market share, according to a FedEx presentation in December. The next largest is Old Dominion Freight Line Inc., which boasts the industry’s highest LTL margins, with just more than a 10% share. XPO Inc., which in the last few years spun out its freight brokerage and a warehouse-operating unit to concentrate on LTL, has just less than 10% of the market.

If FedEx does go down the route of a sale — the company said it would make a decision by the end of the year — XPO would definitely be a suitor. XPO bought the most assets from the bankruptcy of Yellow Corp., and its chairman, Brad Jacobs, has made his career by snapping up companies. A spinoff would be most efficient on the tax side. Private equity can’t be ruled out. There will be lots of interest. Investors will be sorely disappointed if a deal doesn’t materialize.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Thomas Black