Only Musk’s Robotaxi Can Save Tesla Investors Now

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsTesla Inc. is, according to its promoters — very much including Chief Executive Elon Musk — an artificial intelligence giant trapped in a carmaker’s body. That much was evident from quarterly sales and production numbers, and the market’s reaction to them, on Tuesday morning.

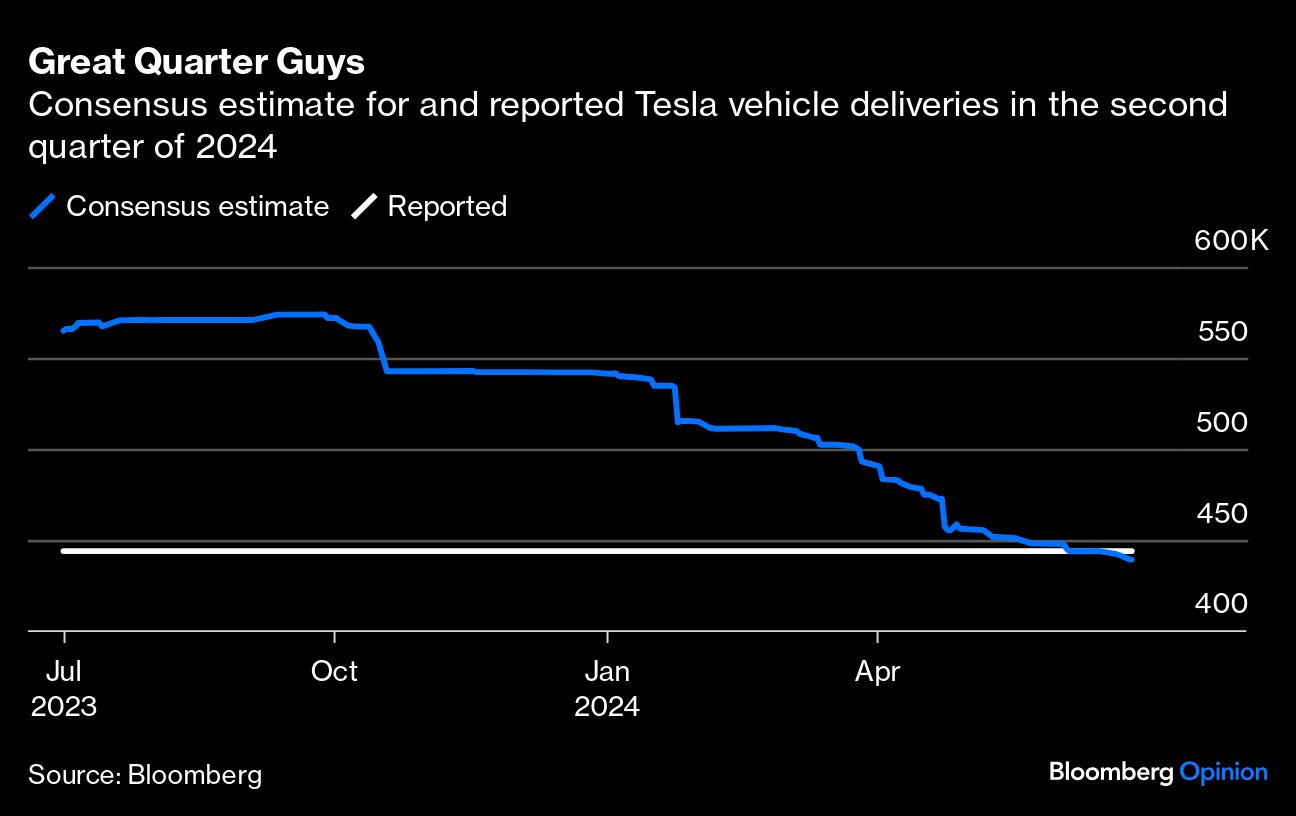

Tesla made about 411,000 vehicles and delivered about 444,000 in the second quarter. This was better than expected, with deliveries slightly beating the consensus estimate and, importantly, outpacing production. Tesla’s stock jumped as much as 10% in response.

The slightest of digging yields a somewhat less bullish interpretation. First, that consensus has been going downhill faster than a Cybertruck with pedal issues. Only a month ago, Tesla’s numbers would have missed.

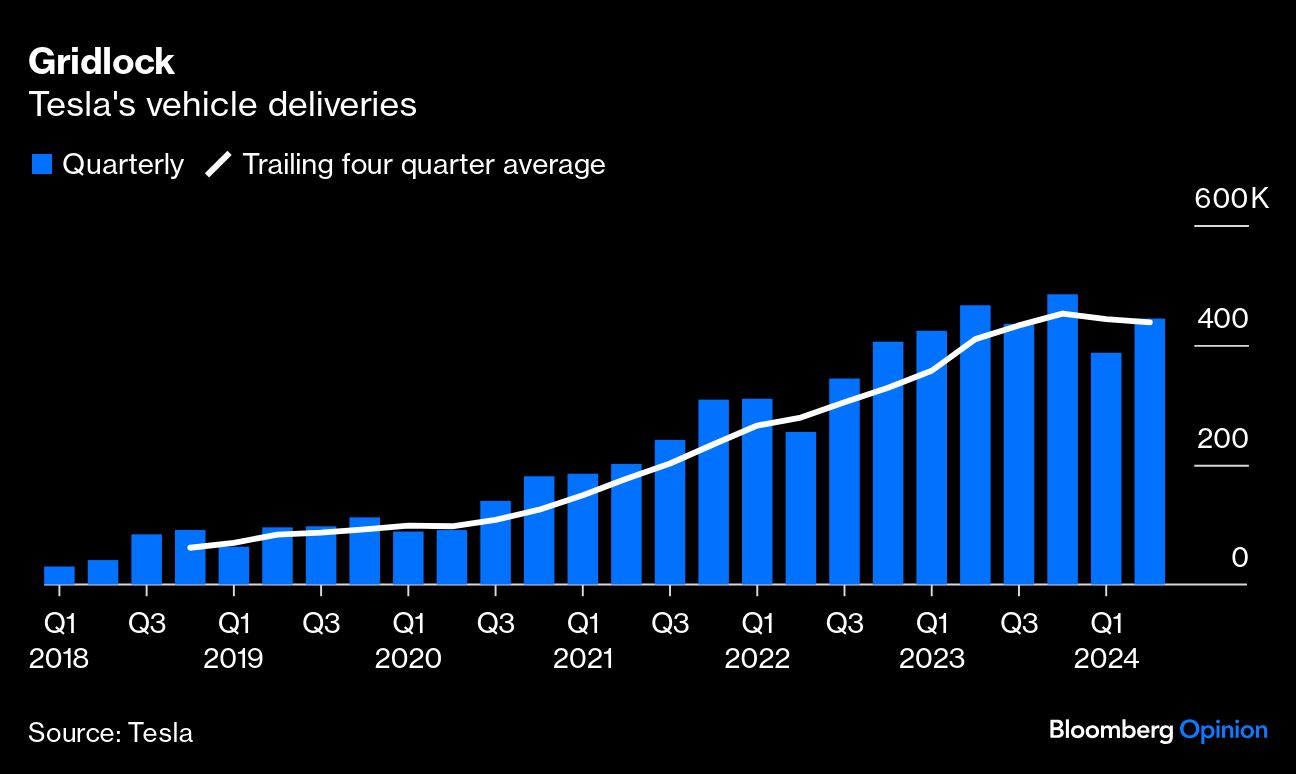

Moreover, even beating estimates meant a 5% drop in deliveries, year over year. On a rolling four-quarter basis, Tesla’s vehicle sales flattened out last summer and Musk in January explicitly abandoned the company’s previous growth target of 50% per year, compounded. The beaten-down consensus estimate implies sales dropping outright in 2024. With the first-half numbers now in the books, even hitting that forecast requires two record quarters in a row, averaging 487,000 deliveries apiece. Pending that next “growth wave,” Tesla’s core business, accounting for 89% of its gross profit, isn’t growing.

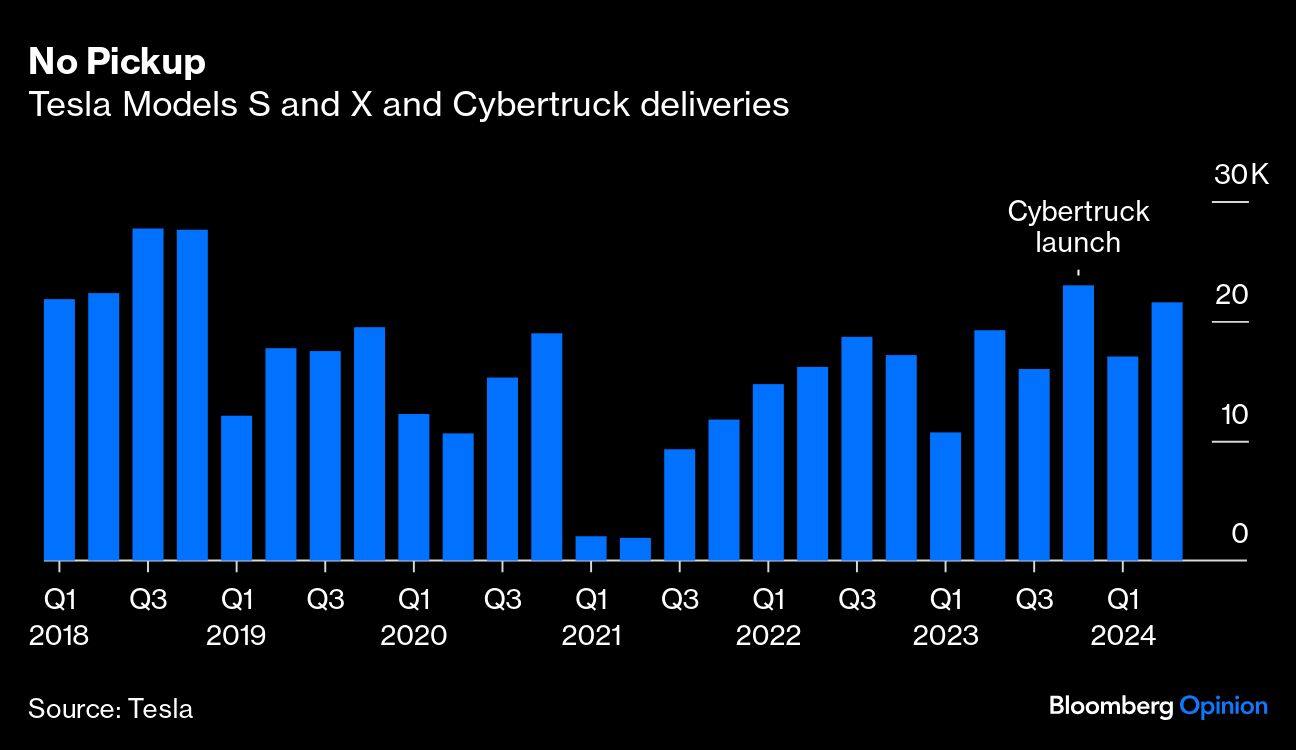

Strikingly, sales of Tesla’s premium models, other than the mass-market-ish 3 and Y, were actually lower in the second quarter than in the fourth quarter of 2023. You may recall that is when the Cybertruck joined the Models S and X in the high-priced segment; meaning the addition of this third model hasn’t boosted those sales overall (which also came in a bit below production). Multiple recalls for the months-old Cybertruck probably haven’t helped fully offset the continued ageing of the S and X when it comes to attracting buyers, even as rival models proliferate and Rivian Automotive Inc., a serious challenger at that end of the market, has received a financial lifeline from Volkswagen AG.

Deliveries of the mainstay Models 3 and Y, while down year over year, did come in higher than production. That cleared about 36,000 vehicles from inventory, which should mean better free cash flow in the second quarter compared with the prior quarter’s big burn.

Yet, overall, Tesla only cleared about a quarter of its big pile of unsold vehicles that has built up since the second quarter of 2022. Moreover, it did so partly via further discounts and even resorting to zero-rate financing in China, which implies an effective price cut of several thousand dollars for those vehicles. Even then, preliminary data from China’s Passenger Car Association show a 24% drop in shipments from Tesla’s Shanghai factory in June, year over year.

As much as these headline delivery numbers beat a hurdle that had been all but buried, the wider context suggests little prospect of turning around what should be the main story: another big decline in earnings. The consensus estimate for 2024 now implies a 22% drop from last year, which saw a 29% drop from 2022.

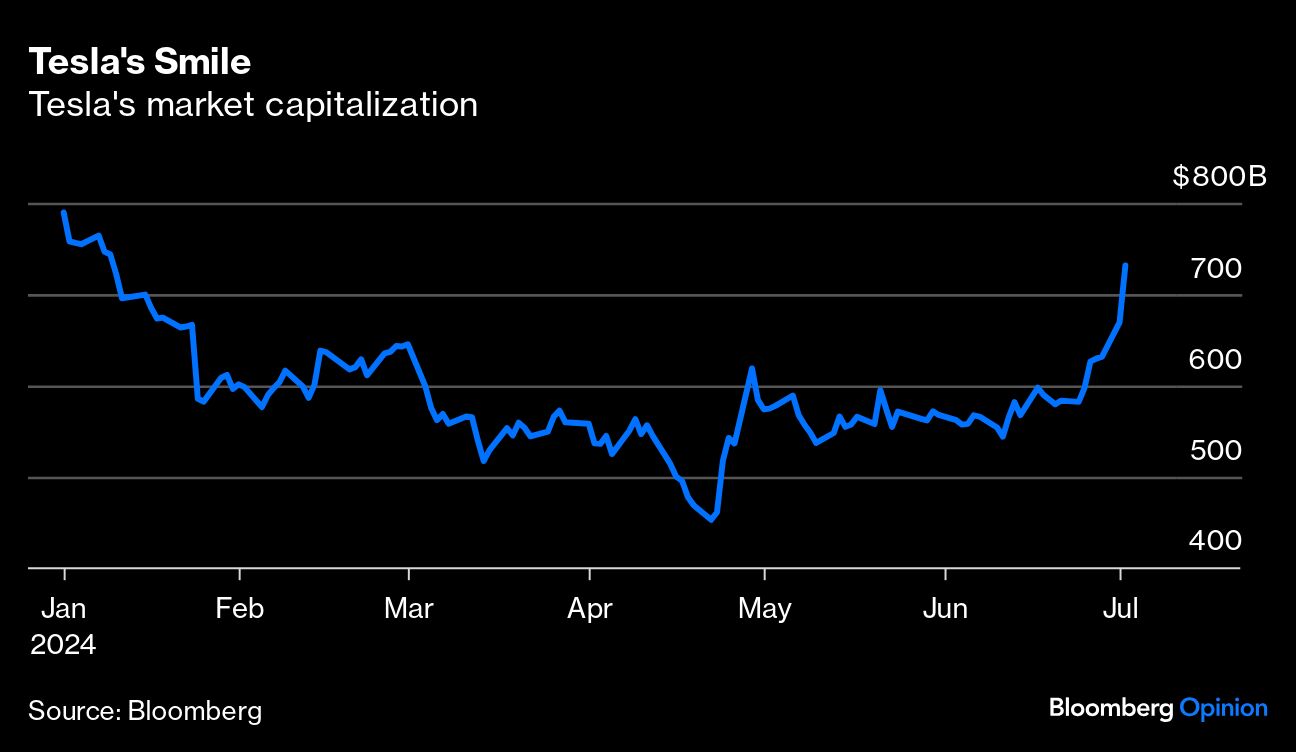

Yet a car company with flattened sales in its core business, an aging lineup and shrinking profits has seen its market capitalization expand by about $275 billion since hitting a low point in April, with a fifth of that on Tuesday morning alone.

As growth and margins in the existing business of making electric vehicles have faltered, the need for AI-related promises to pick up the slack has only intensified. Luckily for Tesla, in the face of repeated disappointments and structural challenges to Musk’s robotaxi vision, investors remain eager as ever to pull on that rope.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All