On the surface, the US employment report for June looked pretty good. Some 206,000 jobs were added, which exceeded the 190,000 median estimate of more than five dozen economists surveyed by Bloomberg. Also, wage growth continued to moderate, easing concern that fast-rising earnings would underpin inflation. But peel back the curtains and you can clearly see why so many are worried the soft patch that the economy seems to have run into may get even softer — or worse.

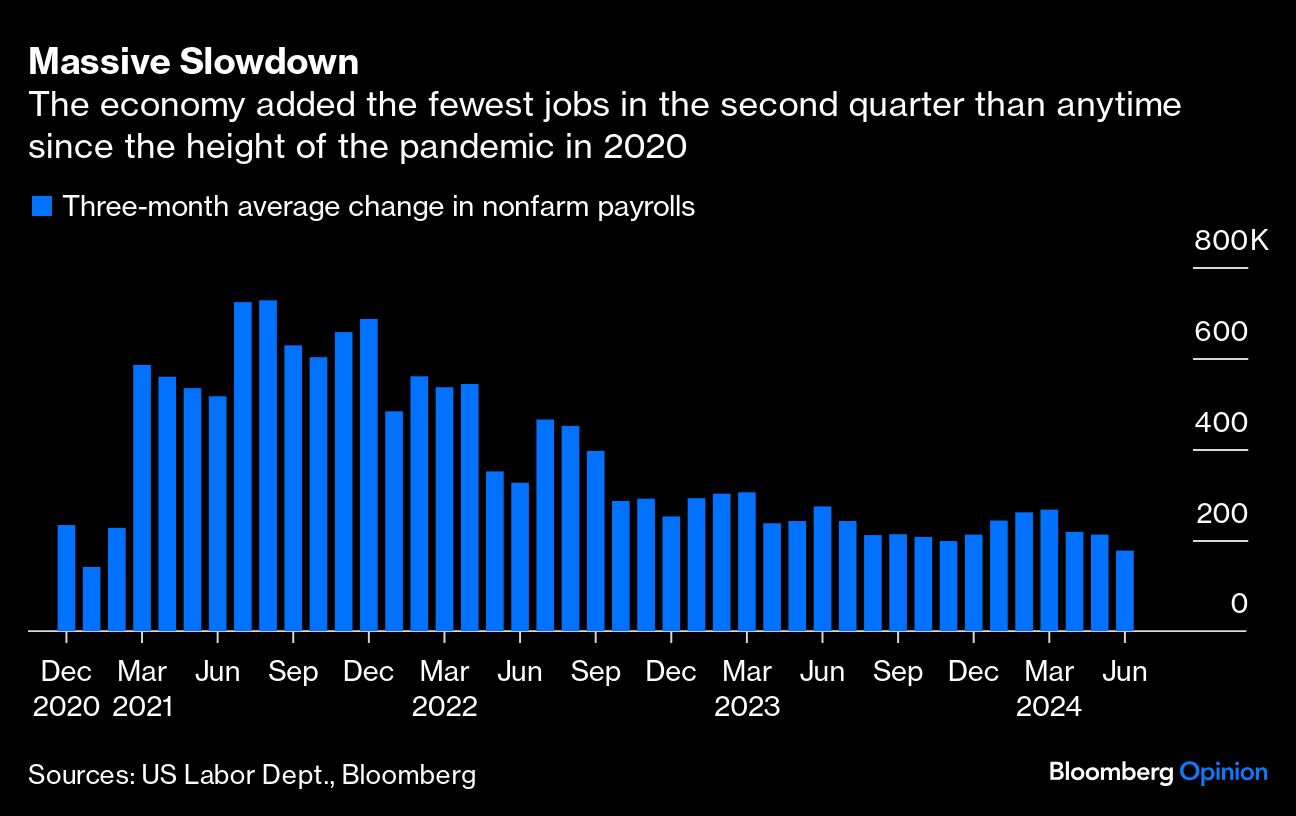

The best place to start is with the revisions to recent monthly labor data. The Labor Department said 111,000 fewer jobs were created in April and May than originally reported. What that means is that monthly payrolls expanded by an average of 177,000 in the second quarter, down from 267,000 in the first three months of the year.

Digging a little deeper we find that the median time it takes for an unemployed worker to find a job rose to 9.8 weeks, the most since February 2022, according to Bloomberg News. On top of that, the number of temporary employees on payrolls tumbled by 48,900 in June, the most since April 2021. The takeaway here is that employers have little need for extra help because they see business demand softening. Those two data points help explain why continuing claims for unemployment applications, a proxy for the number of people receiving jobless benefits from the government, increased to 1.86 million in the week ended June 22, the highest since November 2021.

There are lots of caveats here. Although the unemployment rate ticked above 4% for the first time since November 2021, coming in at 4.1%, it’s mostly rising for the right reasons. In other words, the gain is not so much due to companies laying off workers, but rather an expansion in the labor force. This is allowing employers to become more picky when hiring workers and helping to slow the gains in wages that have helped underpin inflation.

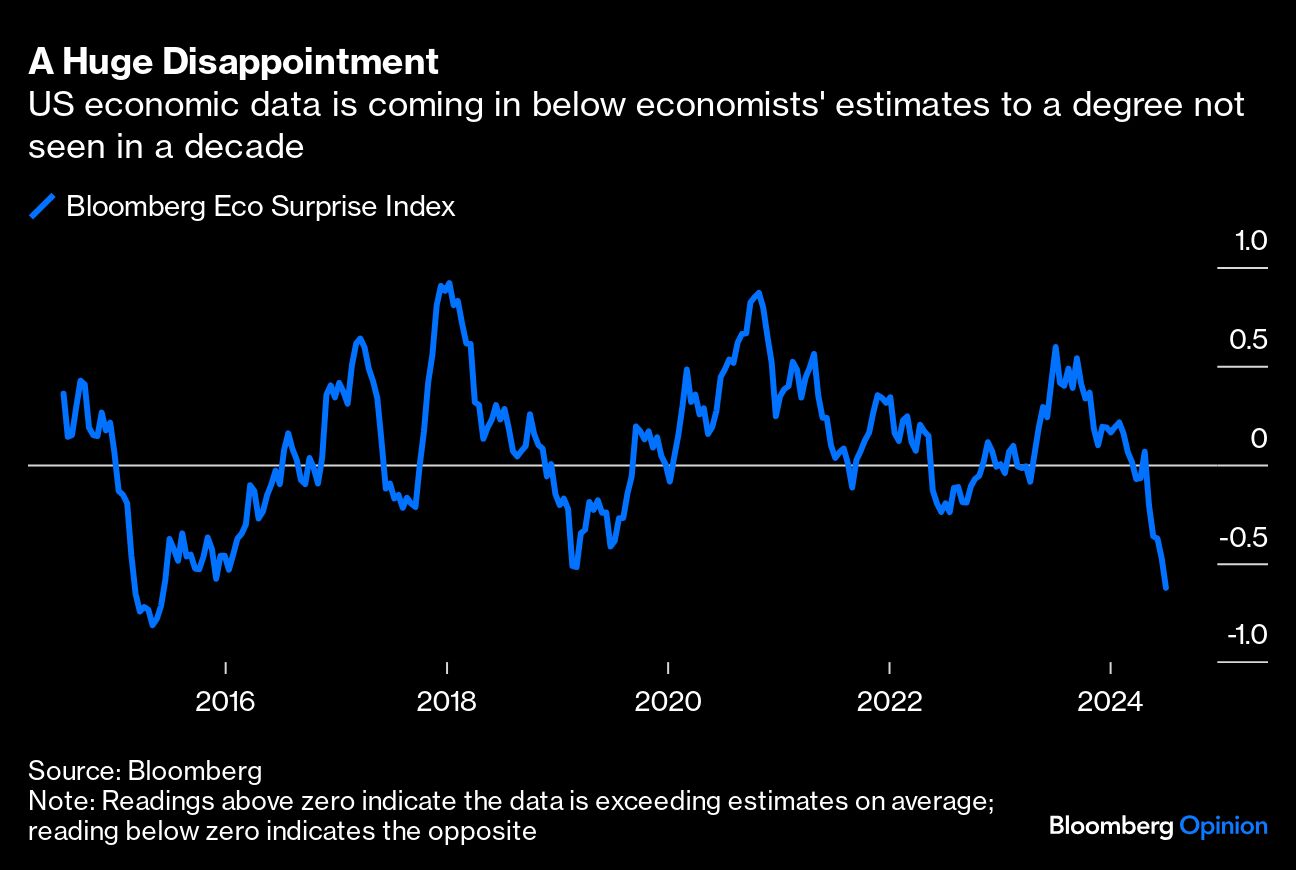

Even so, it’s hard to avoid being concerned that the economy is in the midst of a sharp slowdown. Within the last two weeks alone, we have seen disappointing data from both the ISM manufacturing and services indexes, as well as big declines in new home sales and pending home sales that exceeded economists’ estimates. In fact, the numbers have been disappointing to a degree not seen since 2014, according to data compiled by Bloomberg. In response, the Federal Reserve Bank of Atlanta’s widely followed GDPNow Index, which aims to track growth in real time, has dropped to 1.55%, the lowest reading since December and down from above 4% as recently as May.

So, you can bet Federal Reserve policymakers spit out their morning coffee when this jobs report landed. Fed Chair Jerome Powell was asked earlier this week at a central banking forum in Sintra, Portugal, what keeps him up at night, and he pointed to the delicate balance between taming inflation and avoiding a significant deterioration in the labor market. “It’s very much understood by us that we have two-sided risks, and we have to manage them,” Powell said.

Powell also said he is on high alert for signs of softness in the labor market, but that the central bank can take its time before adjusting monetary policy. Based on this jobs report, time may be running out. Policymakers don’t meet to decide monetary policy until the end of the month, and while almost no one expects them to reduce interest rates then, do expect them to start flagging that a reduction is coming sooner rather than later.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Robert Burgess