Markets today pose a new existential question: Can there be a bubble in something if it has no price?

As a believer in efficient-ish markets, I am uncomfortable calling anything a bubble. Recognizing a bubble requires spotting an asset or asset class that is objectively overvalued before everyone else does. Making this determination is almost always impossible in real time, even if it’s screamingly obvious in hindsight. And that’s in public markets, where prices are easily observed and constantly updated as investors form views and incorporate information.

Sometimes, however, you get an inkling that something isn’t right — and lately I am feeling that about private markets, especially private equity, even if there are no prices that can collapse or be inflated.

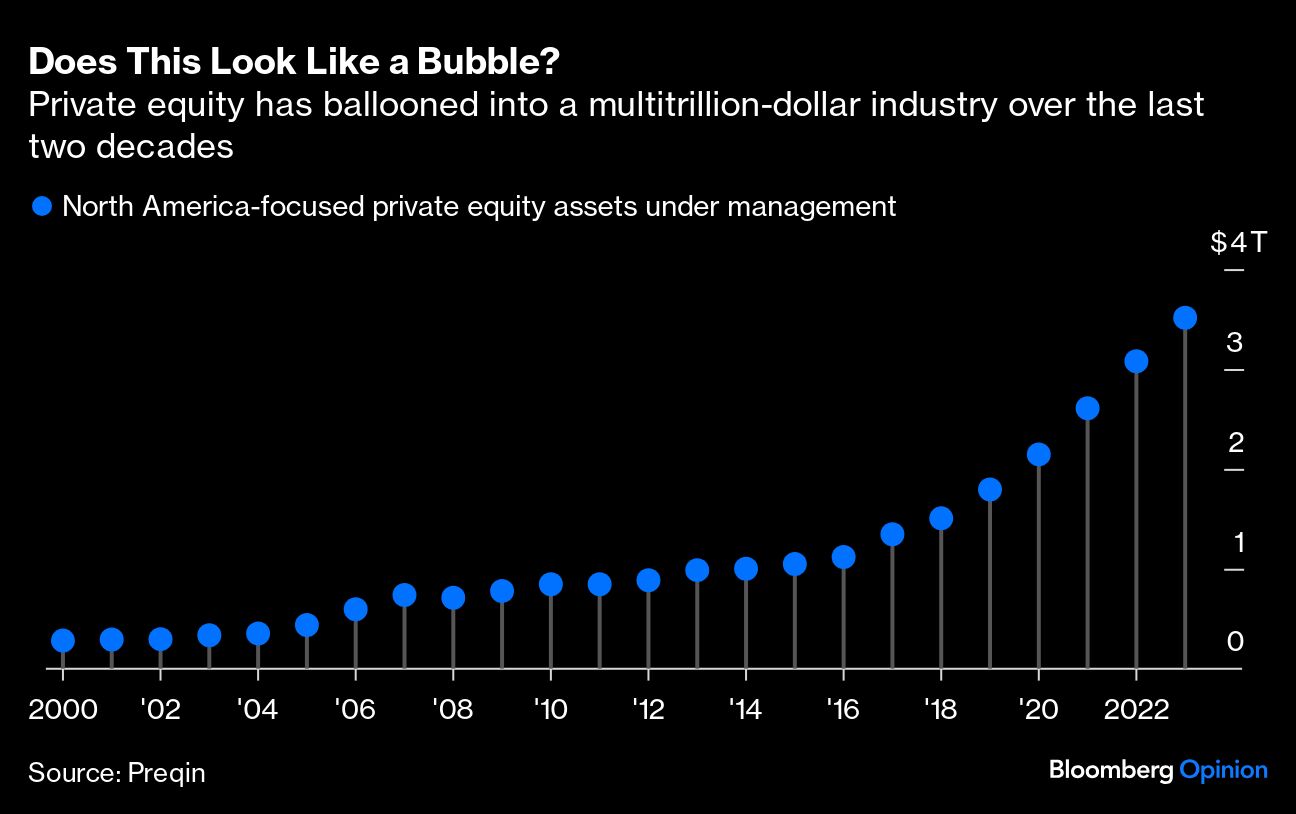

There are several reasons to worry the private equity market is due for some sort of reckoning. Over the last few decades, private markets were flooded with money. Institutional investors — under pressure to achieve high returns, especially in a low-rate environment — turned to private markets that promised high future returns and attractive current valuations (though these were impossible to verify or dispute). In 2023, the value of North American private equity assets under management was estimated to be $3.5 trillion, more than 10 times what it was two decades earlier.

Any asset class inundated with money often gets frothy, and for private markets that means more investments that may not pay off. The higher-forever rate environment poses an extra challenge, as the industry thrived and grew with rates near zero. Some parts of the private asset industry will weather higher rates, but others (commercial real estate, for example) may not be able to. The question is how much of a reckoning is coming, and how much damage will it cause?

“Everything is not going to be OK,” Scott Kleinman of Apollo Global Management recently said. He compared the private equity investments that won’t pay off to a pig being digested by a python. In other words, investors will face fewer realizations and lower returns.

There are reports of pension funds not getting the big payouts they expected — or not getting anything at all, their money essentially tied up in “zombie funds.” Some pensions are short of money and need to take loans from the funds. Other pensions need to sell their stakes at a discount on the secondary market.

Technically, private markets can’t be in a bubble if there are no prices. Valuations can neither collapse nor be bid up by investors. Valuations can certainly fall, and with higher rates they should. But the funds still have a great deal of control over what they say their investments are worth.

A growing secondary market should provide more information, although it remains too opaque, and the creation of better indices may make performance easier to measure. But even with better information, the lack of liquidity also means limited partners can’t suddenly sour and sell their stakes in the funds. Private investments are mostly limited to accredited investors, such as pension funds, endowments or rich people — so at least grandma won’t be losing her life-savings.

That’s not to say there is no reason to worry. The lack of transparency and accountability means bad investments and waste can continue for much longer in private markets. That means capital is not going to its best use, which is bad for growth.

Even if grandma does not directly own any private equity, she is still exposed. In the last decade, public pension funds have been especially keen on private markets, with private equity now accounting for about 15% of their portfolios. It is remarkable that despite one the best bull markets in recent memory, the funding status of many pension funds worsened. That’s largely because their optimistic assumptions about investment returns (enabled by their private investments) did not pan out. If their private investments don’t pay out at all, either pensioners will see their benefits cut or taxpayers will need to pay up.

And private markets do play an increasingly important role in the economy. Between the higher-rate environment and disappointing realized returns, many investors may look elsewhere, and the private equity industry will shrink. In the short term, that would be painful. Many firms have become dependent on private credit or equity for financing. There are many reasons for this, including increased regulatory scrutiny of public markets. But if private markets do shrink, more firms may find themselves short of capital and with nowhere to turn. That could result in people losing their jobs.

Unlike public markets, when the private equity bubble deflates, it probably won’t happen all at once. But just because there is no pop doesn’t mean there was no bubble. Over the past decade or more, private equity has grown too big too fast. That increases the chances it will cause economic damage that the country will have to deal with for years.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Allison Schrager