As Pete Stavros addressed the private equity industry’s yearly shindig in Berlin last month, the KKR & Co. executive’s words were slightly less headline grabbing than those of Apollo Global Management’s co-president Scott Kleinman. But they were just as troubling.

Whereas Kleinman went in hard with his warning that “everything is not going to be okay” for buyout firms, Stavros joined in with the concession that his industry may have gotten “too creative” lately. Noisy or not, his comment strikes at the heart of an issue that’s starting to disturb everyone from investors to regulators: PE’s current mania for financial engineering.

For decades the private equity model seemed unassailable, transforming the industry’s image from Barbarians at the Gate to crucial pillar of capitalism. Funds raised money, bought businesses, loaded them with debt, exited at a profit and convinced happy investors to do it all over again — at ever greater scale. Surging borrowing costs have stalled that engine.

Even though buyout firms say they see green shoots in the M&A market, they’re deep into a third year of higher rates and scant opportunity to sell assets at decent prices, and they’ve been forced into a host of wheezes to keep things going: “Payment in kind” (PIK) lets PE-owned companies defer crippling interest payments in exchange for taking on even more costly debt; “net asset value” loans allow cash-strapped buyout firms to borrow against their holdings.

This endless kicking the can down the road — in the hope that rate-cutting central bankers will at some point ride to the rescue — is making the pensions, insurers and others who back PE firms uneasy. When buyout groups do look to sell, PIKs, NAV loans and other kinds of excess baggage are creating obstacles.

At the same time regulators are becoming ever more fearful about what’s being hidden from view, and the threat of contagion from any private-markets meltdown to the banking system and real-economy jobs. Investors simply want firms to return to their founding mission: Improving the companies they own.

“PIKs are like a Pacman that eats away at the equity,” says John Graham, president and chief executive officer of the Canada Pension Plan Investment Board, a C$632 billion ($464 billion) behemoth that’s one of the world’s largest private equity investors. “It gets back to the ability to grow the operating performance of the companies and making sure that returns” come from that rather than from “financial leverage,” he tells Bloomberg.

Some top industry figures don’t dispute the perils of gulping down more and more varieties of debt. “On things like NAV loans and margin loans, it’s just additional leverage and if things go against you, you can have a problem,” Stavros, KKR’s cohead of global private equity, said at the Berlin event.

A broader worry is that while buyers’ hunger may be back for higher-quality companies, as shown by the uptick in investment-banking activity on Wall Street, the books of PE firms are stuffed with less attractive businesses snapped up at inflated prices. Many were acquired at the buyout boom’s zenith in 2021 and 2022, and often paid for by piling them up with floating-rate debt. This means the high-wire juggling act of PIK, NAV and the rest will likely carry on until rates fall meaningfully — or something breaks.

“We’re seeing a slow-grinding implosion of this titanic asset bubble that started in 2012,” says Dan Zwirn, CEO at Arena Investors.

“Valuations are way, way off in some cases, and there will come a point, I expect soon, when auditors say they’re unable to sign off on the accounts anymore,” he adds, explaining that many asset sales in secondary markets will be done at far lower values than where they’re being priced by firms today.

Private Grief

Private markets — made up of PE firms who take stakes in companies, and private credit funds who lend to them — have ballooned since the turn of the millennium, expanding by 15 times according to a September report from the International Organization of Securities Commissions. McKinsey and Co. estimates private-market assets were $13.1 trillion at the end of June 2023.

Regulators have applauded this revolution for shifting riskier corporate lending away from Wall Street. And yet private firms’ lack of transparency is a source of increasing angst. “We don’t have a good understanding because there’s just not the information on who holds what, and what are the interrelationships,” says Jose Manuel Campa, the European Banking Authority’s chairperson.

This opacity makes it hard to see how much trouble is being kept from view. And the use of PIK and other forms of so-called “back leverage” makes it even more difficult to get a clear picture on the state of privately owned companies.

The amount of distressed debt owed by portfolio businesses of the 50 biggest PE firms has climbed 18% since mid-March to $42.7 billion, according to data compiled by Bloomberg News using rankings from Private Equity International. “We expect defaults to go up,” Daniel Garant, executive vice president and global head of public markets at British Columbia Investment Management Corp., another Canadian pensions giant, told Bloomberg recently.

A key challenge for regulators is that much of PE’s borrowing was arranged with loose legal terms at a time when lenders were fighting for deals, making it easier today to use financial wizardry to keep sickly businesses alive.

“You don’t know if there are defaults because there are no covenants, right?” says Zia Uddin of US private credit firm Monroe Capital. “So you see a lot of amend and extend that may be delaying decisions for lenders.”

All this additional debt makes it tougher, too, for PE owners hoping for exits.

Take Advent International and Cinven. They took on heavy debts when buying TK Elevator including a roughly €2 billion ($2.1 billion) PIK note they loaded onto the lift maker that’s swelled to about €3 billion, according to people with knowledge of the situation. The tranches carry an interest rate of 11%-12%.

To clear a path for a potential initial public offering that could come as early as 2026, prospective advisers have suggested pushing this debt up into the holding company or getting cash from a pre-IPO investor, the same people say. At present, a capital increase that would dilute the PE firms and help pay down the PIK is seen as the most likely option, although the backers haven’t started formally exploring any particular exit route.

Advent and Cinven declined to comment.

Such cautionary tales haven’t deterred others. Apex Group, a provider of services to asset managers, has just refinanced a slug of debt with a $1.1 billion PIK loan from Carlyle Group Inc. and Goldman Sachs Private Credit.

Apex is trying to fix a problem common to many PE-owned companies: that their debt was only partially hedged against spiking base rates, meaning interest costs have spiraled dramatically. It says its owners are looking for a 2026 exit at the earliest.

Concerns about PIK loans have also begun to impact the people who provide them, often private credit funds. Canadian lender Ninepoint Partners has had to temporarily halt payouts from three funds, one of which offers borrowers the fallback option of using PIK if needed.

Desperate to deploy their mountains of dollars, private credit firms have stepped up that kind of lending even though they may not get cash interest payments for years and are taking risks by lending more money to strugglers.

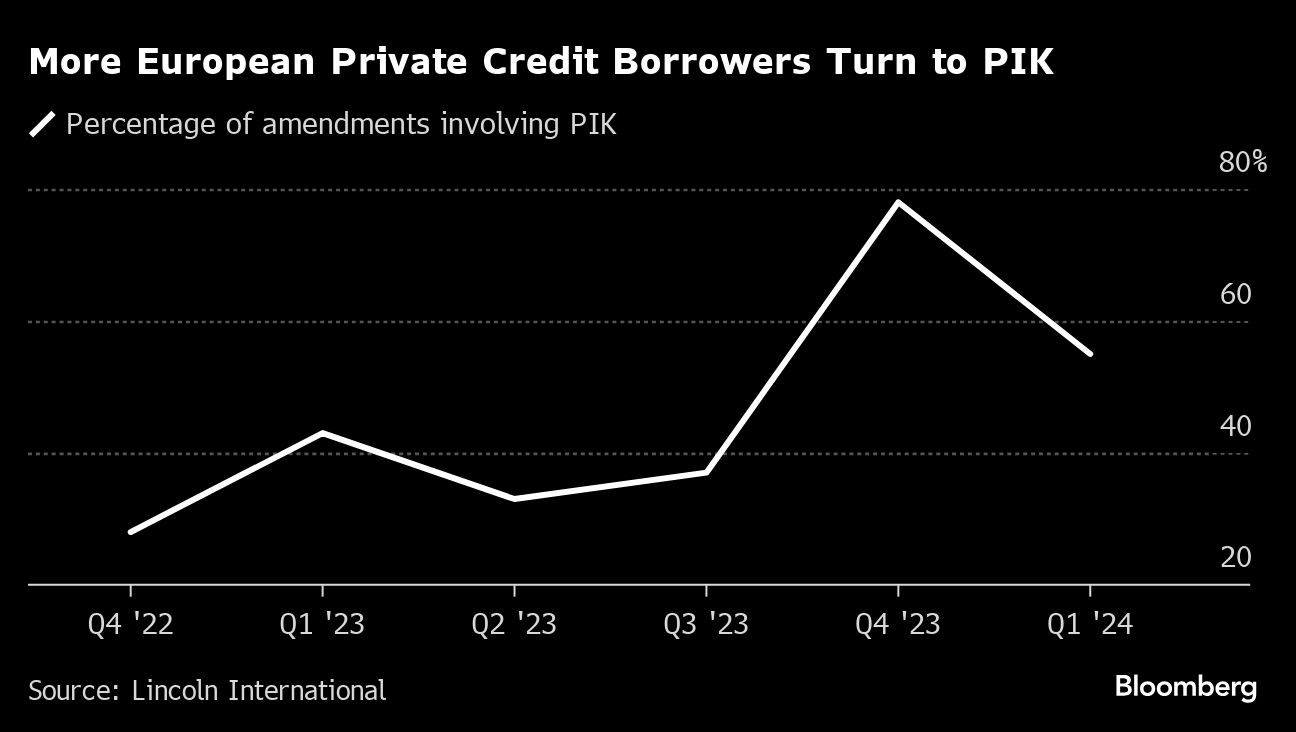

In Europe, most private credit borrowers have been turning to PIK when reworking debt obligations, according to data from Lincoln International. In the US, Bloomberg Intelligence reckoned in a February note that 17% of loans at the 10 largest business development companies — essentially vehicles for private credit funds — involved PIK.

Some investors don’t want firms using such tools to flatter returns. One senior pension fund executive says they try to avoid managers who use NAV as they view it as firms being lazy about exits, adding that they’d prefer to crystallize losses than get distributions this way.

A report from Goldman Sachs Asset Management at the end of last year warned that “LPs should be mindful that these transactions represent financial engineering, rather than true operational value-add.”

The proliferation of NAV, PIK and similar has also deepened connections between PE firms and their credit cousins, a possible contagion risk if things go wrong. In the US almost 80% of private credit deal volume goes to private equity-sponsored firms, according to the Bank for International Settlements.

Other unconventional financing is raising eyebrows, too, such as continuation vehicles — a controversial practice of firms selling sometimes troubled assets to a new fund that they also manage. The second quarter of 2024 saw a “considerable uptick” in such funds, says Jeff Hammer, global cohead of secondaries for private markets at Manulife Investment Management.

CVC Capital Partners came up with a novel use of extra leverage during its March IPO of Douglas AG. It borrowed €300 million from banks, injecting it as equity in the German beauty retailer to strengthen its balance sheet, and pledging Douglas shares as collateral in a so-called margin loan, according to the offering’s prospectus.

A fall of 30% to 50% from the IPO price would trigger a margin call, according to people with knowledge of the matter who declined to be identified as the information is private. The stock is down about a quarter since the listing. CVC declined to comment.

Mattis Poetter, co-CIO of Arcmont Asset Management, says the gloom around buyout firms shouldn’t be overdone, especially those with a record of returning cash to investors. “PE firms have gone through very tough environments in the financial crisis and after,” he says in an episode of Bloomberg’s Credit Edge podcast. “And they’re quite good at managing difficult periods.”

Others see PE’s relentless plate-spinning as proof that regulators’ anxiety around “nonbanks” shouldn’t be confined to private credit funds and how generously they “mark” their own loans. One leading industry executive says it’s wrong to discuss private credit’s flaws without considering the greater risk for capital that’s junior to that debt: namely, the buyout firm’s equity.

“You could argue that all private valuations are incorrect since current practices don’t use the latest market inputs,” says Noel Amenc, associate finance professor at EDHEC Business School. Data from his team shows most private assets are marked in “significantly different” ways to where they’d be priced if their valuers incorporated data representative of their market.

A new BIS report warns that “a correction in private equity and credit could spark broader financial stress,” citing potential knock-on effects on the insurers that heavily invest in these funds and on banks as the “ultimate providers of liquidity.”

“Some features in the financial markets have probably postponed the impact of the rise on interest rates, for example fixed rates, longer maturities and so on,” Agustin Carstens, BIS’s general manager, told Bloomberg TV last week. “These can change, and will be changing in the near future.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Kat Hidalgo, Allison McNeely, Neil Callanan, Eyk Henning