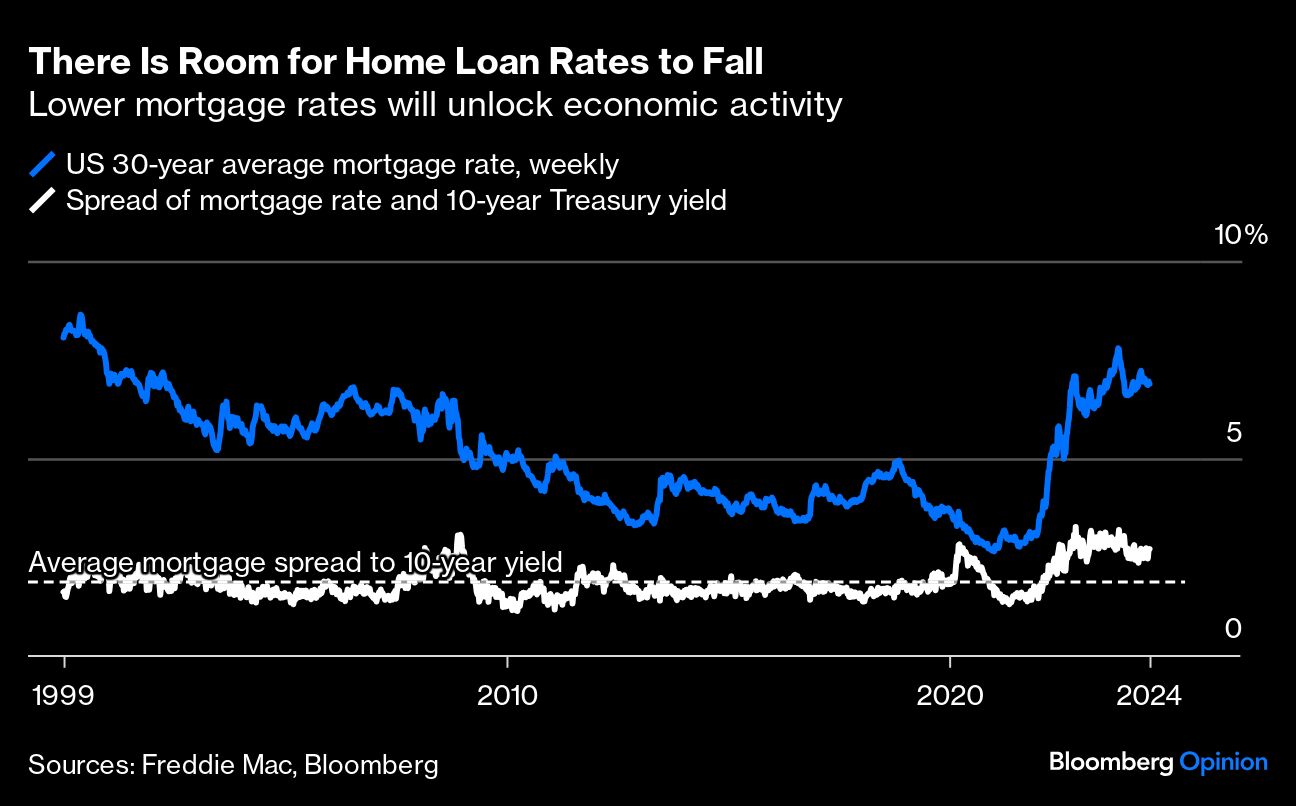

It’s been clear since the fall of 2022 that the housing market needed lower interest rates to fix many of its problems including a lack of affordability for buyers, the mortgage rate lock-in dynamic for homeowners, and reduced activity for companies ranging from Home Depot Inc. and Lowe’s Cos. to suppliers of building materials.

But the Federal Reserve was more focused on containing inflation than helping the housing market. No more. Economic data over the past few months have shifted policymakers’ priorities, with investors expecting the first of several interest rate cuts in September. The Fed now needs to support the labor market, and that means treating housing as an industry to boost rather than suppress, and using its health to gauge whether monetary policy has been eased enough to hold the economy in balance.

It’s not that the labor market is an immediate problem. What’s concerning is its direction. The unemployment rate has risen for three consecutive months — the first time that’s happened in eight years — and at 4.1% stands around the Fed's longer-term forecast. If it was likely to stay at 4.1%, the Fed could have confidence that the economy was in balance, but all signs point to a continuing deterioration — something Chair Jerome Powell doesn’t want to see.

Worries about a recession in 2023 and sluggish demand this year have made businesses reluctant to add workers even as the labor force continues to grow. The goal of monetary policy should now be to change all this — lower interest rates will boost demand and, in turn, spur hiring, consumer confidence and spending.

All this brings us back to the housing market, the most obvious place for lower borrowing costs to work their magic. Existing home sales are running at a rate that’s 25% below what should be considered normal; owners are sitting on record levels of home equity that they won’t access until rates are lower; and housing-related industries ranging from remodeling to furniture to freight have been in downturns since 2022.

An increase in transactions would mean more work and commissions for real estate agents, loan officers and workers associated with moving. They would likely unlock home equity between mortgage refinancings and home sellers spending some of their capital gains, powering consumption. Furnishing sales are highly correlated with transactions, too, so we can expect demand to improve for home goods retailers, the factories that supply them and the railroads and trucking companies that transport goods.