Pressure is again mounting on the proxy advisory firms that recommend how investors should vote on executive pay and other corporate matters. Regulators need to remember who should be prioritized here — investors, not company management.

The corporate sector has an enduring complaint that this niche industry, which is dominated by Institutional Shareholder Services Inc. and Glass Lewis & Co., is too opaque and too powerful. In 2022, the US Securities and Exchange Commission scrapped tighter regulation on proxy advisers. Now the debate is creeping into the UK regulatory conversation, with the British governance watchdog this week flagging plans for greater scrutiny.

April’s annual shareholder letter from JPMorgan Chase & Co. boss Jamie Dimon sums up the concerns of the C-suite. A longstanding proxy critic, he portrays an investment ecosystem where voting decisions are made by asset managers’ so-called stewardship committees without heeding the investment professionals who run the funds. These committees blindly follow proxy adviser recommendations based on information that’s frequently “not representative of the full view and not accurate,” Dimon goes on. To cap it all, corporates struggle to get errors corrected. In sum, he says these advisers have “undue influence.”

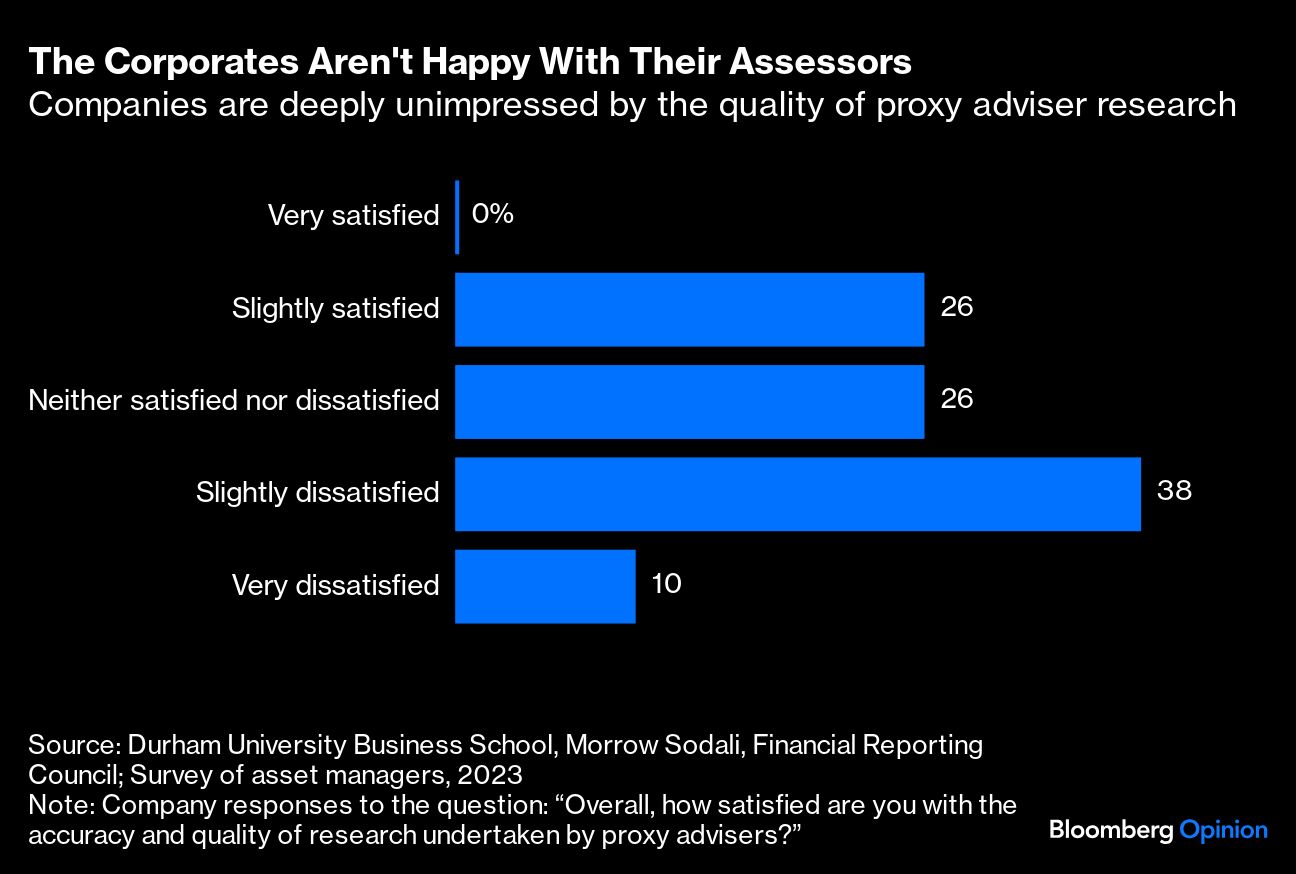

In the same month, amid frowning at a proposed pay bump for AstraZeneca Plc Chief Executive Officer Pascal Soriot, the drugmaker’s chairman wrote that proxy advisers’ “double standards” on pay did “serious harm” to UK corporate competitiveness. Research by Durham University and consultant Morrow Sodali published last year found that some UK companies reckoned proxy advisers were box-tickers ignorant of corporations’ freedom to disregard governance best practice so long as they explained why.

It's against this backdrop that the UK Financial Reporting Council (FRC) has been canvassing opinion on changes to its stewardship code for the investment industry. Small wonder that on Monday it said its revisions would seek “greater transparency of [proxy advisers’] activities.” The code is technically voluntary. In reality, there’s a de facto obligation on investment and proxy firms to sign up.

The fact that shareholder democracy is largely funneled through two proxy advisers is a matter of public interest. Quality matters here. But the cost-benefit analysis for more direct oversight isn’t compelling.

In an ideal world, we wouldn’t need them. Investment managers would reach their own conclusions on company resolutions. Dimon has committed to this approach at JPMorgan’s own asset management arm. His counterpart Larry Fink at asset manager BlackRock Inc. has likewise decried his industry’s reliance on proxy advisers.

But not all fund firms have the capacity to handle the avalanche of voting decisions that hit in the annual meeting season. Outsourcing makes sense. Most company resolutions are uncontroversial; a proxy advisory firm can triage, freeing asset managers to focus on the trickier issues. Even JPMorgan’s investment arm will continue using proxy firms for research.

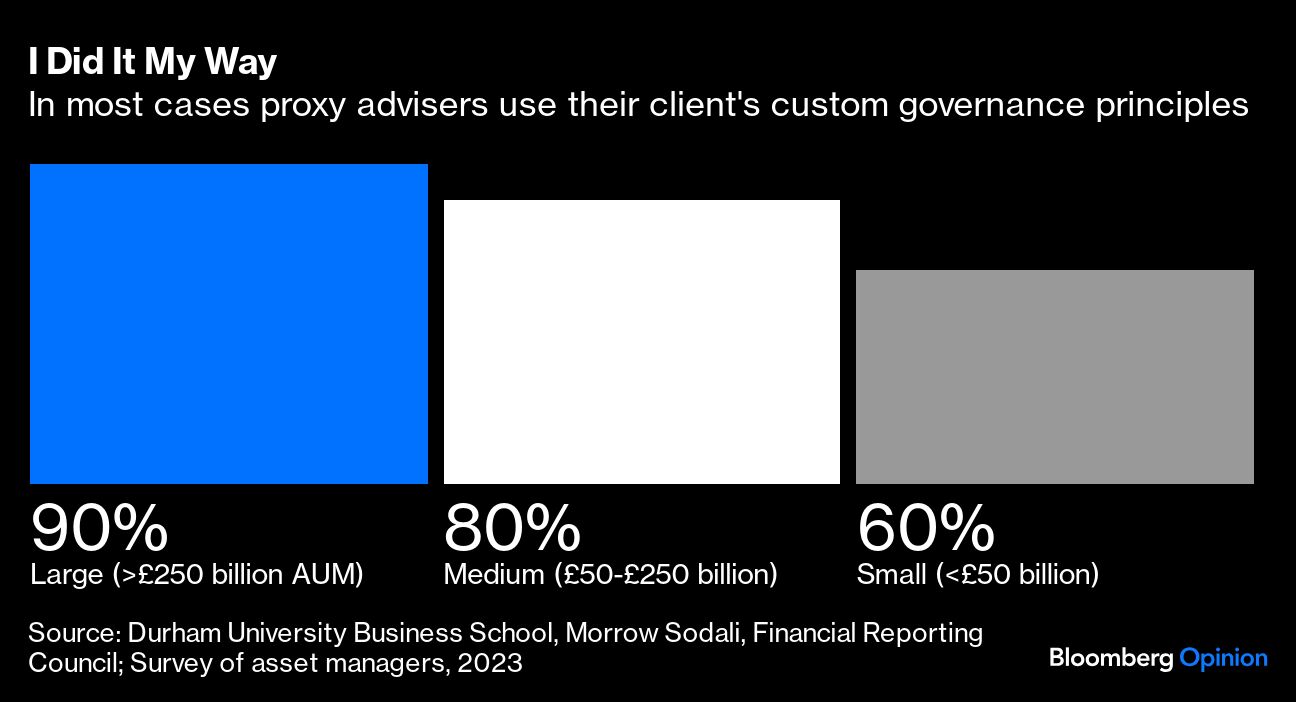

Does this lead to excess influence? Not in the way that’s commonly assumed. Most asset managers require proxy advisers to generate voting recommendations based on their client’s own governance principles.

That still leaves the gripe that recommendations are crunched from box-ticking, whether against the proxy adviser’s rubric or the client’s, and overlook the corporation’s individual circumstances, with fund managers going along willy-nilly. The fact that investment managers don’t always side with proxy advisers against management suggests otherwise. Soriot got his remuneration.

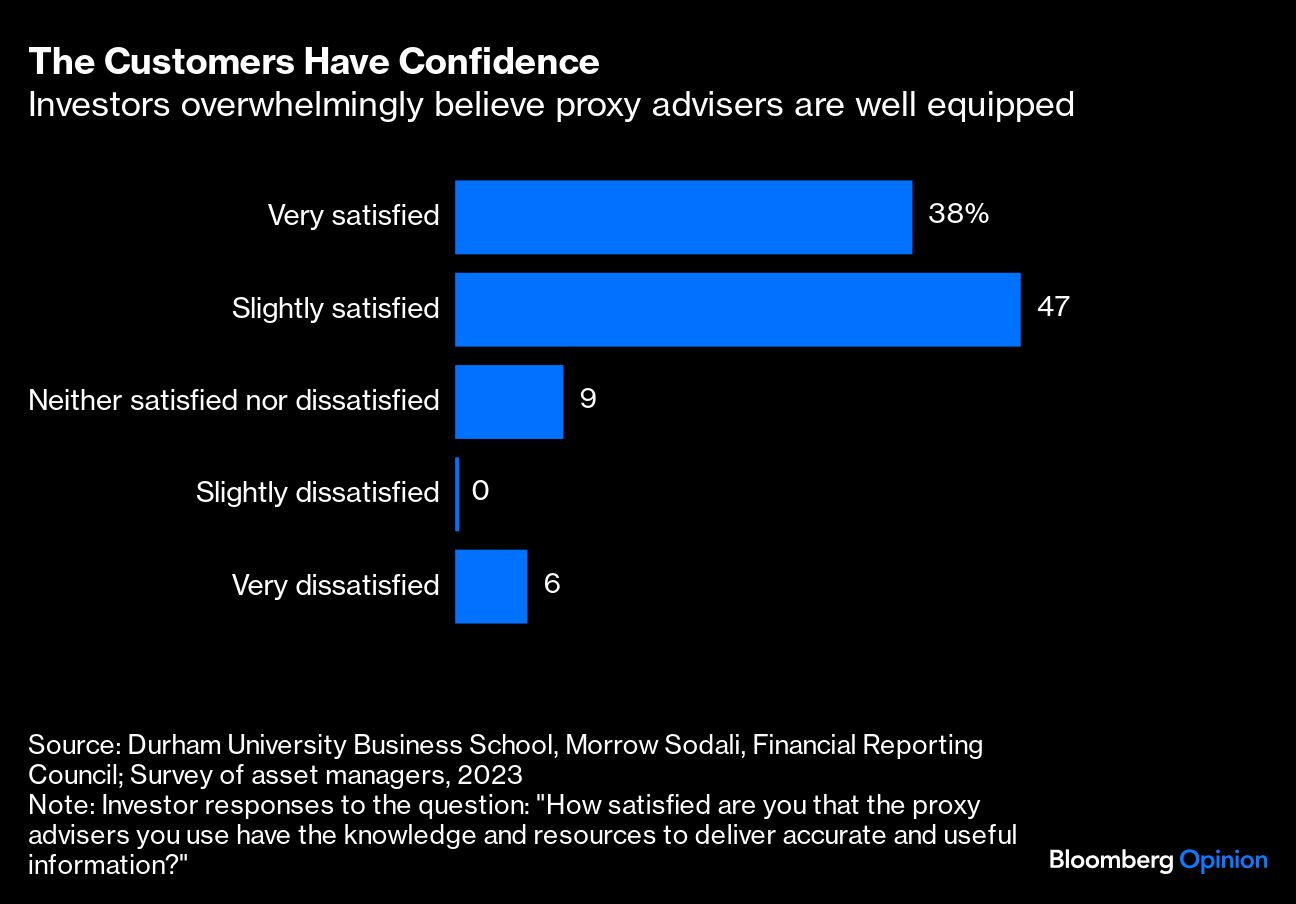

The investor is the paying customer. So the economic incentives are to generate accurate, unbiased advice. There’s little evidence proxy advisers are routinely producing recommendations against company management based on falsehoods or incomplete information, let alone that these are also winning the day.

It’s not clear what disclosure requirements the FRC is mulling as it seeks to show how voting recommendations are devised. The risk is that guidelines add cost or indirectly stifle editorial independence. The quality of the proxy advisers’ work boils down to the persuasiveness of the final recommendation in controversial cases. The corporation in focus is free to broadcast its counterargument if it believes the reasoning is flawed. Investors can then make up their own minds.

A key question here is whether the resource constraints in the asset management sector are replicated among the proxy advisers. This is a low-fee business. The time between resolutions coming out and voting cutoffs can be as little as two weeks. A greater regulatory burden could just put more pressure on the independent voice when the corporate sector has ample resources to get itself heard.

Any transparency drive might be better targeted downstream (where Dimon wants more disclosure). This could help ensure fund managers are forming their own conclusions and using the proxy advisers as a resource while treating them as just another opinion in the market.

In the UK, there are some general requirements that asset managers disclose how much they use proxy advisers’ default recommendations. But a couple of specific disclosures could be usefully made industrywide: Firstly, the proportion of voting recommendations that were actively reviewed by the investment manager, and secondly, the proportion of voting recommendations that were discussed between the stewardship team and the portfolio manager. That would meet the corporate griping head on.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Chris Hughes