A fifth of Americans are on the hook for an 833% jump in the cost to ensure the lights stay on. The folks being paid that premium, mostly electricity generators in this instance, face that most welcome of problems: What to do with a windfall. Shares in the likes of Constellation Energy Corp. and Vistra Corp. were up by double-digit percentages Wednesday morning.

But they also face an unwelcome complication: Politics.

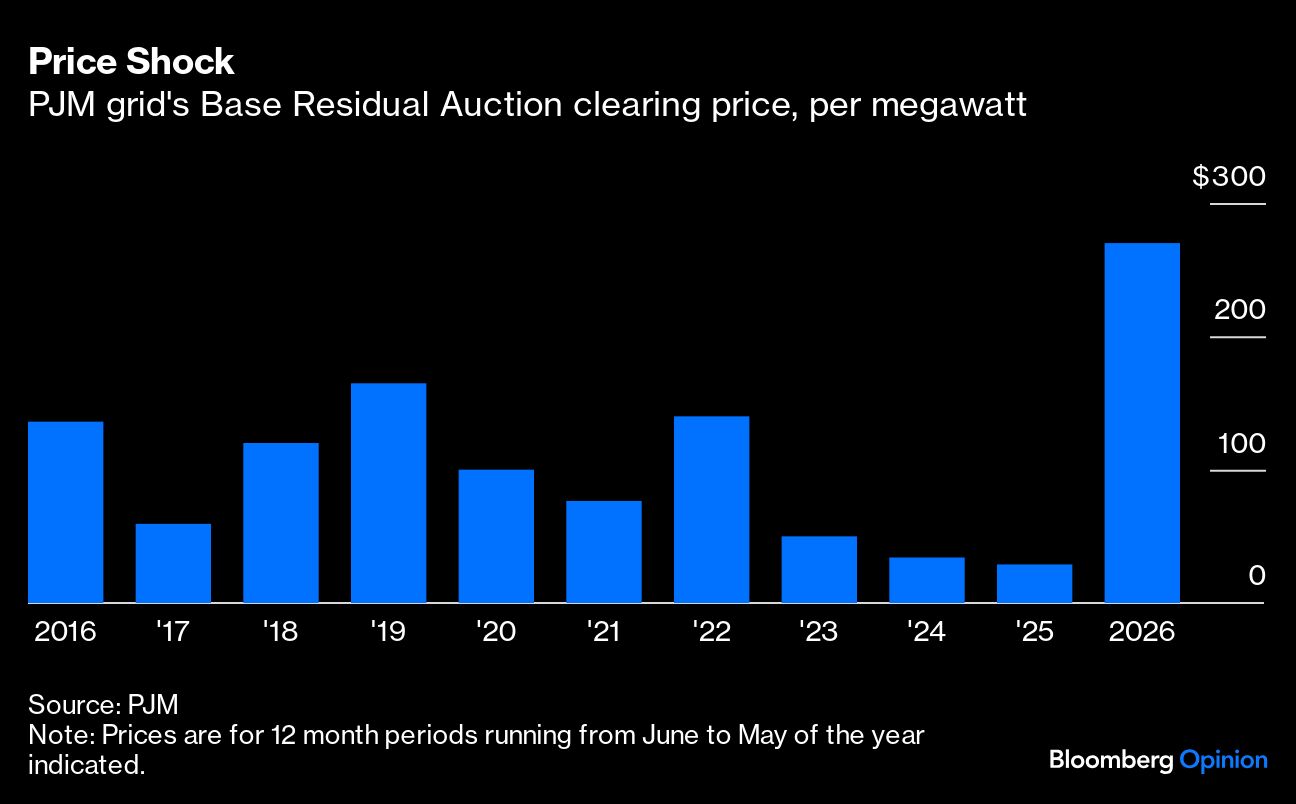

The insurance to which I’m referring goes by the ungainly name of the PJM Base Residual Auction. This is the capacity market for the PJM regional transmission organization, a power grid stretching across a swath of the mid-Atlantic and Midwest regions that accounts for about a fifth of US electricity consumption. The auction sets the price to be paid to generating plants in return for them being available when needed in the future (or, conversely, for large users of power to agree to curtail demand as required) such as during a particularly hot day when everyone has their air conditioning running. This encourages older, less-profitable plants to stay open and new ones to be built. Insurance for the grid, in other words.

The latest results, announced Tuesday evening, looked like someone had misplaced a decimal point: Almost $270 per megawatt compared with about $29 last time. The consensus expectation was about $60 to $100.

For generators, this is pure profit — being paid just to be there, essentially. And this will really move the needle. Constellation, for example, should net an extra $600 million of Ebitda in 2025, according to Andy DeVries, a utilities analyst at CreditSights, equivalent to a 13% boost to the consensus forecast.

On the customer end of things, paying insurance on a service powering almost every aspect of one’s daily life is hard to argue with. At an implied 1.5 cents per kilowatt-hour of demand across PJM’s grid, the increment here isn’t as severe as that 833% would suggest. It’s still a hike though, equivalent to about 10% of the average residential tariff in Virginia, for example.

The really big, if underlying, issue concerns the why. PJM’s rising insurance premium relates to a step-change upward in demand forecasts. PJM isn’t alone in this; there’s been a gathering national freak-out about the grid over the past year, as demand picks up after more than a decade of flatlining as novel sources of consumption tap in: electric vehicles, reshored factories — and datacenters.

The latter, turbocharged by Big Tech’s race to master artificial intelligence, are emerging as a significant potential draw on the power grid in various parts of the US, but PJM most of all. Virginia is already the capital of US datacenters and, along with other states under PJM, has attracted more new projects under construction than any other region. One big draw is that PJM is viewed as a reliable grid with adequate spare capacity to absorb extra demand from all those chips.

Much as local politicians like the tax revenue paid by new datacenters, their power demand is emerging as a political lightning rod. Grids generally defray the cost of upgrades and new equipment across all users — in effect, for example, the cheaper-to-service urban household subsidizes the cost of building and maintaining power lines to remote villages that would otherwise be uneconomic to serve. Everyone is usually fine with this. But when a datacenter requires an expensive new power line, things can get contentious.

It’s harder to relate to AI and, unlike a new factory, datacenters don’t bring much in the way of jobs, which are more visible than tax payments. Moreover, for environmentally minded residents, the jump in expected demand will likely mean coal plants stay open longer on PJM’s grid, raising greenhouse gas emissions through 2030, according to Hugh Wynne, a utilities analyst at Sector & Sovereign Research.

For opponents of the datacenter boom, the PJM auction’s blowout quantifies the costs in a tangible, readily digested way — as do, on the flipside, those jumping stock prices for generators. For datacenter developers, it also undercuts the sense that PJM’s spare capacity, either in terms of megawatts or political tolerance, is necessarily abundant.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Liam Denning