Bond investors pared back their expectations for Federal Reserve interest-rate cuts slightly as data showed US inflation ebbed further in July, reinforcing the case for a quarter-point reduction next month.

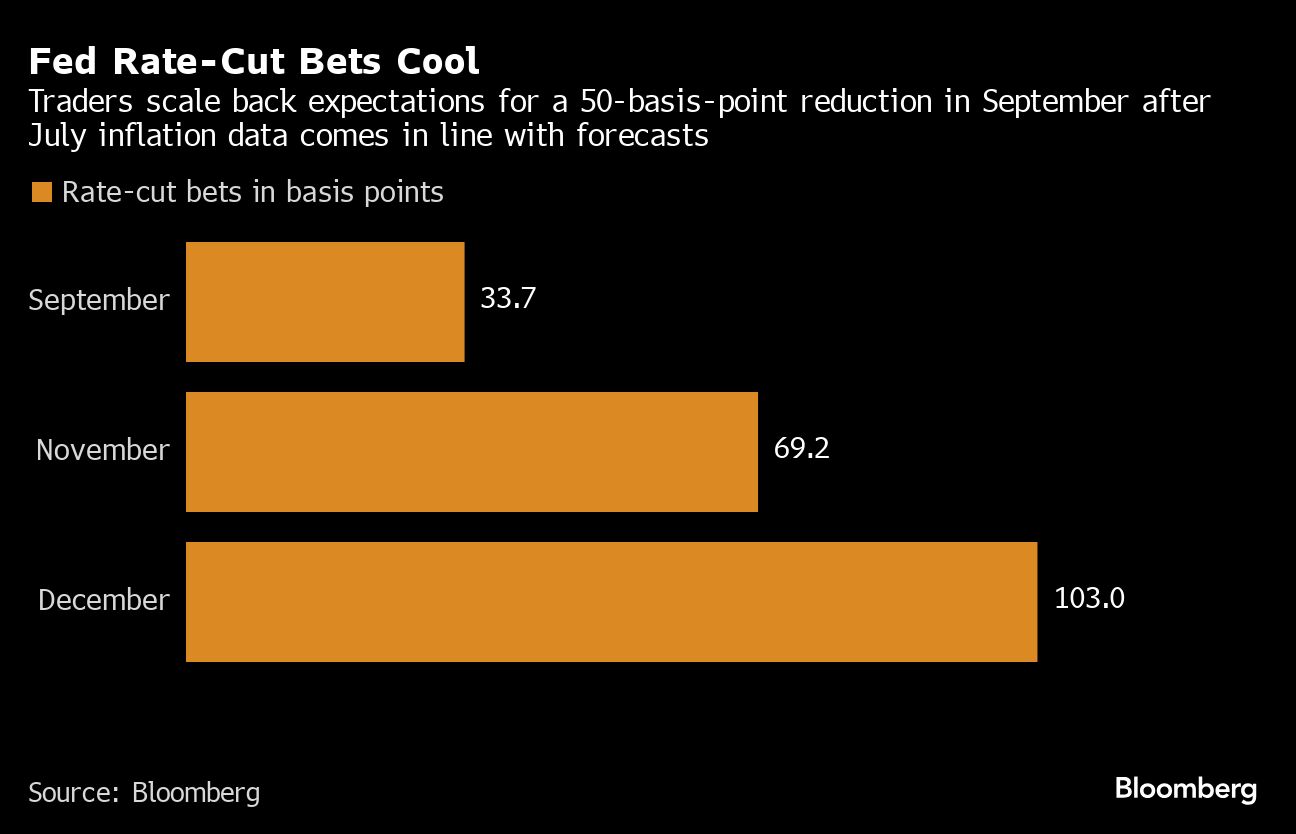

Traders are pricing in 33 basis points worth of easing at the September gathering, down from about 37 basis points a day earlier. That lowers the odds of a half-point cut at the next central bank meeting to around one-third after underlying US inflation eased for a fourth month on an annual basis in July.

The CPI data is “confirmation the inflation problem is whittling away,” David Kelly, chief global strategist at JPMorgan Asset Management told Bloomberg Television. A CPI figure “close to expectations is a case of sell the news — and that’s going on in the bond market.”

The policy-sensitive two-year yield rose as much as about six basis points to 3.99%. Benchmark yields remained a touch higher across the curve, with the exception of the 30-year yield.

Ahead of the data, investors had been positioned for a rally in Treasuries as expectations rose for aggressive Fed rate reductions. In recent sessions, the market pricing had shown a split on the outcome of either 25 or 50 basis points in easing in September.

Traders continue to price in just over 1 percentage point worth of rate reductions in 2024.

The data “cleared the way for a 25 basis point cut in September while not completely shutting the door on the chance of a 50 basis point cut,” said Lindsay Rosner, head of multi-sector fixed income at Goldman Sachs Asset Management.

On Tuesday, Atlanta Fed President Raphael Bostic said he’s looking for “a little more data” before supporting a reduction in interest rates, emphasizing he wants to be sure the US central bank will not have to change course once it begins cutting. Earlier that day, data showed producer price index rose in July by less than forecast.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Michael Mackenzie