With US equities on the rebound, this summer’s selloff is looking more like a pause in the bull market than the beginning of its end.

Of course, traders have struggled to forecast where the economy is headed — and the recession fears that helped drive the recent pullback could resurface again just as quickly as they faded. On top of that, the US elections and geopolitical tensions are adding other elements of uncertainty.

But beneath the surface, there are some reassuring signals. Among them: The selloff hit a relatively small slice of the market, with nowhere near the breadth of the routs set off by the Federal Reserve’s rate hikes, the pandemic and other pivotal events. And while valuations are at risk of another recalibration if the economy does wind up sputtering, the S&P 500 Index during the recent retreat held above a threshold that — to technical analysts, at least — telegraphs investors’ continued confidence.

Moreover, the benchmark has already recovered all of its August decline and is now just 2.2% away from its mid-July record high.

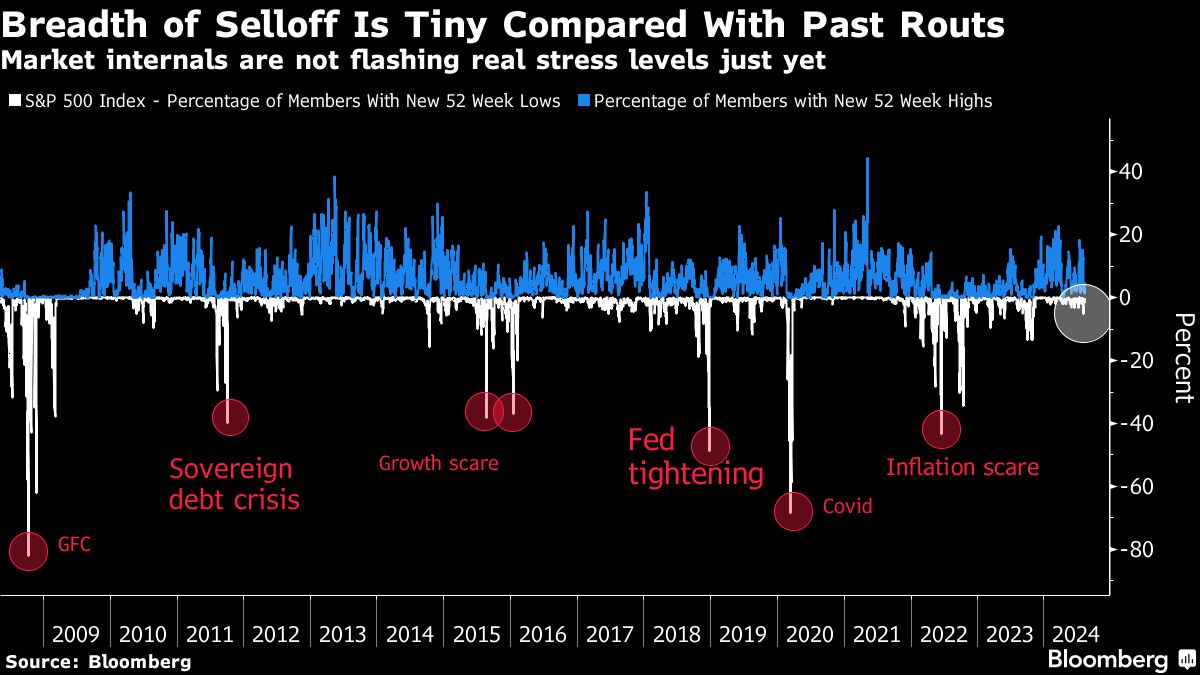

Contained Selloff

While the slide that started last month was sharp and swift, sending the tech-heavy Nasdaq 100 Index into a technical correction in three weeks, it was driven by a narrow number of stocks.

During its depths, only about 5% of S&P 500 members fell to a one-year low, according to data compiled by Bloomberg. That means the drop had a far more limited scope than previous ones set off by major macroeconomic shifts. After the inflation surge drove the Fed to hike rates aggressively in 2022, nearly half the index tumbled to a 12-month low. The pandemic sent about two-thirds to that level.

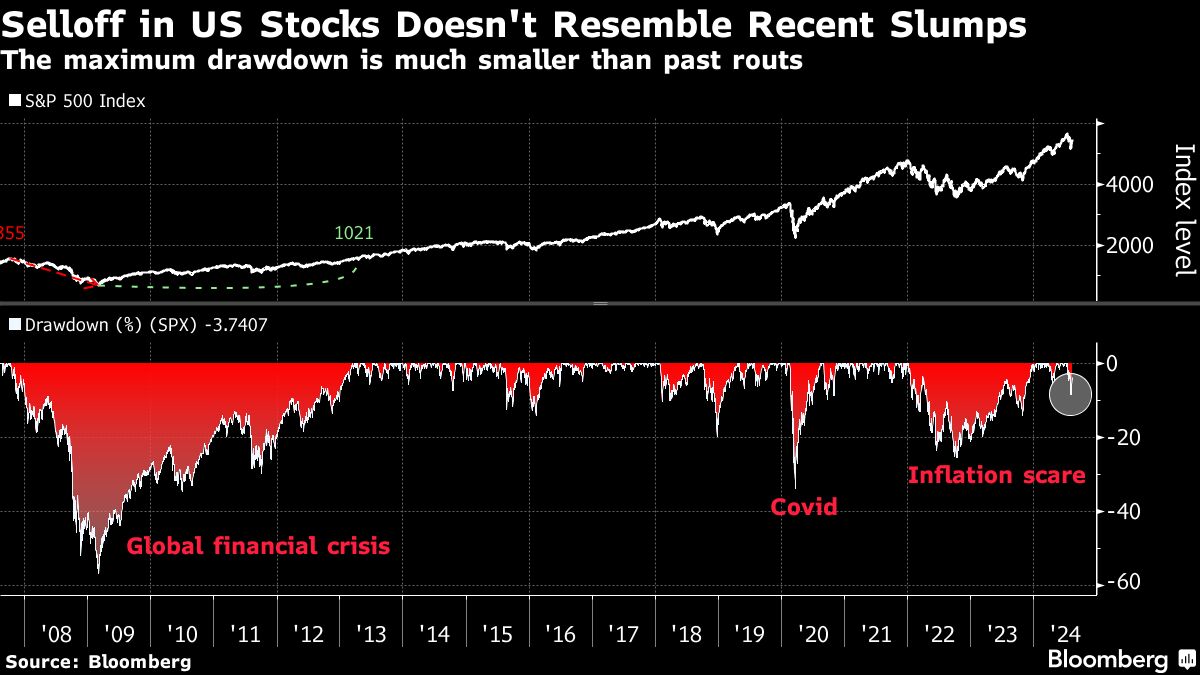

Limited Drawdown

Before last month, the S&P 500 had been on its longest stretch without a 2% one-day decline since the start of the global financial crisis in 2007. From one perspective, that makes the reset look overdue.

Unlike the Nasdaq 100 — whose drop reflected long-simmering concerns about heady tech valuations — the S&P 500 never dipped into official correction territory, rebounding after an 8.5% drop from its peak.

In 2022, the index sank 25% before a sustained rebound. And during the global financial crisis, it plunged as much as 57% — and then took four years to fully recover.

Above Key Levels

The S&P 500’s 200-week moving average has been a strong indicator of the index’s floor since the turn of the century. More recently, the benchmark bounced back after hitting it during the economic growth scare in 2016, the US-China trade war in 2018 and again in 2022.

This time around, it came nowhere near that threshold even at its lowest point. While that also indicates how much further the index could slump in a renewed selloff, it shows that investors were confident enough to swoop in well before the market tested a new bottom.

Japan Rebounding

Japan was at the heart of the global turmoil after its monetary policy tightening sent the yen to one of its strongest levels this year, driving hedge funds to sell off assets to unwind carry trades financed by low-cost loans in Japan.

The currency is now easing again because policymakers there were quick to reassure markets that further rate hikes were likely off the table. That’s flowed through to stocks in Japan, too.

Warning Sign

On the other hand, the economic risk that the Fed has waited too long to start cutting rates hasn’t gone away. So the recent rebound means that more of a soft landing is being priced in, exposing the market to another slide if that proves off base.

One measure of what investors are counting on can been seen in how stocks linked to the economic cycle — or so-called cyclical sectors — are faring relative to their less-exposed peers.

In the US, a Goldman Sachs Group Inc. basket that measures the relative move between the groups shows that while cyclicals have trailed defensives recently, they are still priced for an economic expansion.

On Thursday, the unexpectedly large jump in retail sales lent credence to that view. But previous figures have also pointed to a cooling in job growth and declining activity in the manufacturing sector.

“By no means am I hitting the panic button here, but compared with other asset classes, the S&P 500 seems to have priced in very little uncertainty,” said Matt Stucky, chief equity portfolio manager at Northwestern Mutual Wealth Management.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Sagarika Jaisinghani, Michael Msika