The worst of the housing affordability crisis is behind us. But the past two years have shown that housing isn’t a bubble that is likely to pop overnight, nor can prices be forced lower in the short term with government intervention. Rising incomes, falling mortgage rates, more construction and thoughtful policy will slowly chip away at the affordability problem. It will probably take five years or more to approach the kind of purchasing power homebuyers enjoyed before the pandemic.

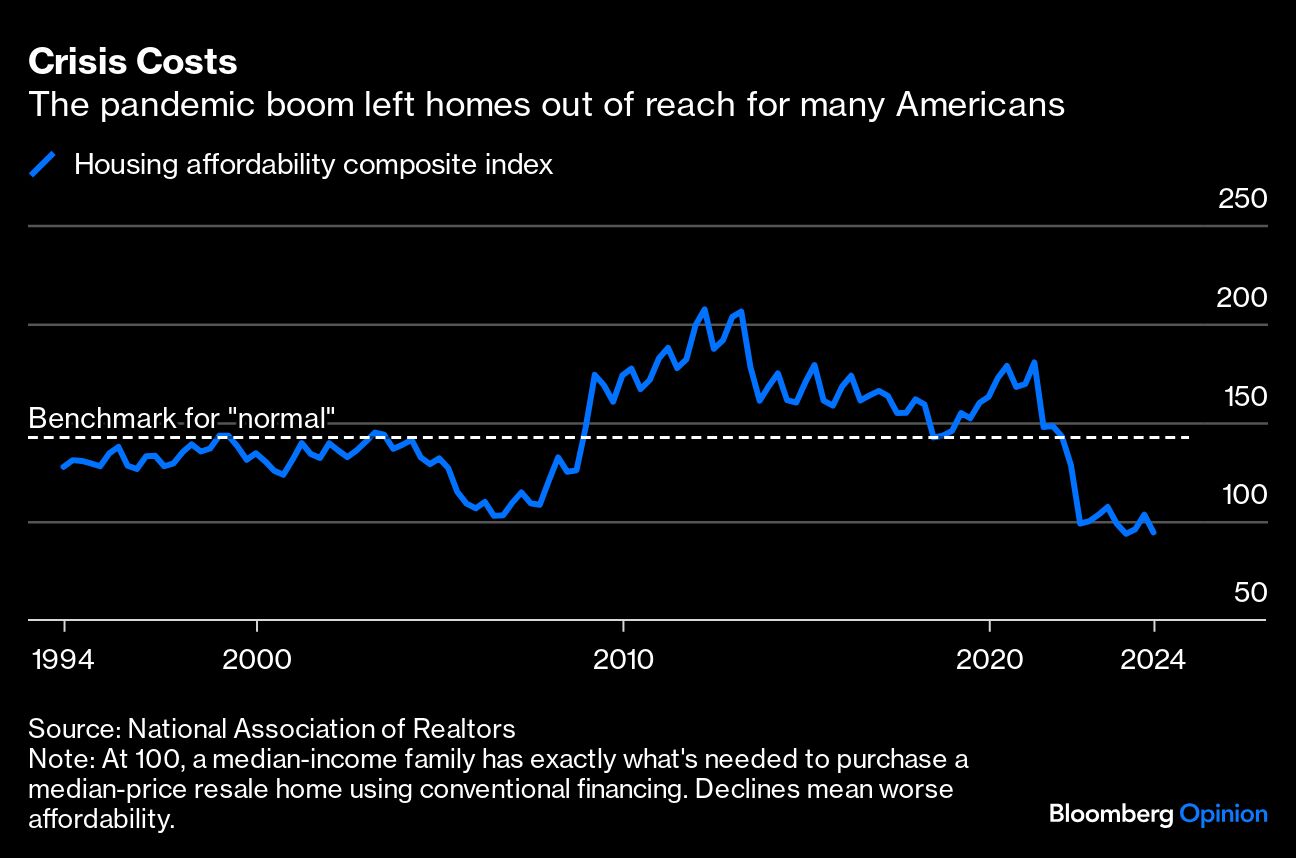

The National Association of Realtors’ affordability index helpfully combines median incomes, median home values and the cost of conventional financing to offer a gauge of just how far we need to travel. It’s nice having a standardized index because the housing market hasn’t been normal for any sustained period for about 20 years. First came the subprime-fueled boom of the mid-2000s, then a bust that stretched into the mid-2010s, then the low-interest-rate frenzy of the pandemic and, finally, the generationally high mortgage rates of the past few years. A good benchmark of “normal” to strive toward is June 2018 — the most unaffordable month of the 2010s but similar to what conditions looked like between the mid-1990s through the early-2000s.

That month, the median resale price was $274,000 and mortgage rates were around 4.5%, which translated to a monthly payment of $1,382 using the standard assumptions on the Zillow mortgage calculator for property taxes and home insurance. Given average hourly earnings for private sector employees at the time, the monthly payment was 30.7% of a full-time worker’s income.

Now let’s look at where we are today. Plugging in resale home prices from June, a 6.5% mortgage rate and last month’s average hourly earnings, those same assumptions mean workers would need to allocate 43.2% of their income to monthly payments. Returning to the kind of housing affordability that Americans enjoyed in mid-2018 overnight would require home values to drop 30% or for mortgage rates to decline to 3% — needless to say, this isn’t very likely.

People have been calling for a crash in home values ever since interest rates began to rise sharply in the spring of 2022. And while higher rates have largely arrested price appreciation, declines haven’t happened in most places.

Most homeowners have low mortgage rates or own their homes outright and simply don’t have to sell. Even with resale inventory rising throughout the country, it remains low by historical standards, and those underlying dynamics are unlikely to change. Prices may fall modestly in some parts of the country and stagnate in many more, but widespread large-scale declines are unlikely.

The interest rate cuts priced into the futures markets — a fed funds rate approaching 3% by the end of 2025 — would probably only take mortgage rates down to somewhere in the 5% to 5.5% range. The 3% home-loan rates of the pandemic were a crisis response, and we should hope to never experience those conditions again.

Building more homes will help with affordability over time, but even here the near-term outlook is challenged. Apartment construction has stalled ever since interest rates soared and rent growth slumped. Leading homebuilders have also grown a bit cautious on single-family construction in recent months as rising resale inventories in places such as Texas and Florida put downward pressure on prices.

Government incentives to increase construction and offer first-time buyers a hand can make a difference, but this will take time, and success is far from guaranteed.

In a speech last week, Vice President Kamala Harris laid out a plan to provide first-time homebuyers with $25,000 to help with a down payment and pledged to build 3 million new homes and rentals by the end of her first term if she wins the presidency. Yet she’d probably need Democrats to control both the House and Senate to pull that off — an outcome with a 1-in-4 chance, according to prediction market site Polymarket. Even with a Democratic sweep, building an additional 750,000 homes per year on top of the current pace of construction isn’t feasible given supply chain, labor and other logistical challenges. Building even half that over four years would be an achievement.

A plausible path to improved affordability over time is annual wage growth of 3.5%, home price growth of around 2% — lower than the historical average because of both increased construction and rising resale inventories — and mortgage rates at 5%. Over five years, this combination would bring housing affordability back to within 12% of those 2018 levels, with perhaps some down payment assistance from Washington closing the remaining gap. Affordability should improve every year from here, just not as fast as anxious homebuyers would like.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Conor Sen