American consumers have surprised many economists this year by continuing to spend even as their savings shrink and the labor market cools. They’ve been aided in part by pockets of deflation that have boosted their purchasing power on things such as gasoline, automobiles and airfares.

But with the personal saving rate near its lowest level since the mid-2000s, it’s fair to ask whether consumers will keep spending. The slow revival of a long-dormant financial product may offer a partial answer.

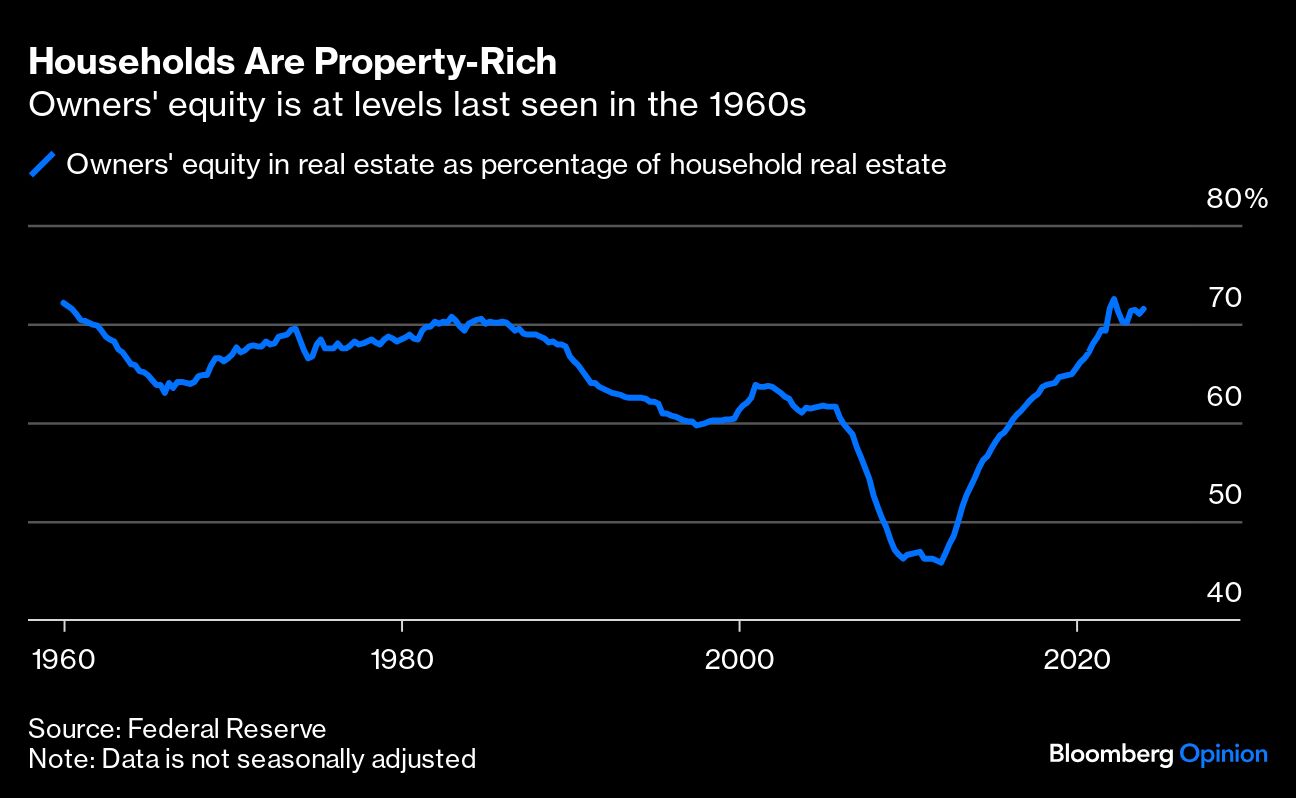

Home equity loans give people with substantial wealth locked up in a house the ability to take money out to fund things like renovations or debt consolidation or a family vacation without having to refinance their entire existing mortgage. We’ve started to see a slow but consistent rise in such loans on bank balance sheets, with 2025 looking like a year of growth for a product that fell out of favor after the subprime mortgage crisis.

There’s good reason why home equity loans faded into irrelevance. Underwriting standards tightened significantly following the 2008 financial crisis after being way too loose in the mid-2000s. It took years for home values to go up enough for homeowners to even have enough equity to borrow against. Households generally spent much of the 2010s paying down debt rather than taking on new debt. And mortgage rates continued to hit new lows throughout the decade, making a full mortgage refinance more compelling than home equity loans, which are pricier.

For people of a certain age, there was also a negative stigma attached to home equity loans — in the aftermath of the 2008 recession, a stereotype that gained little sympathy was the homeowner who borrowed against their house to buy a boat or a car, only to wind up losing their job and house.

There are two types of home equity loans. Fixed-rate loans function as a second mortgage with a lump sum being borrowed, a predetermined repayment schedule, and usually a fixed interest rate. And there are home equity lines of credit, or HELOCs, which act more like credit cards; they have variable interest rates and allow borrowing up to a set limit.

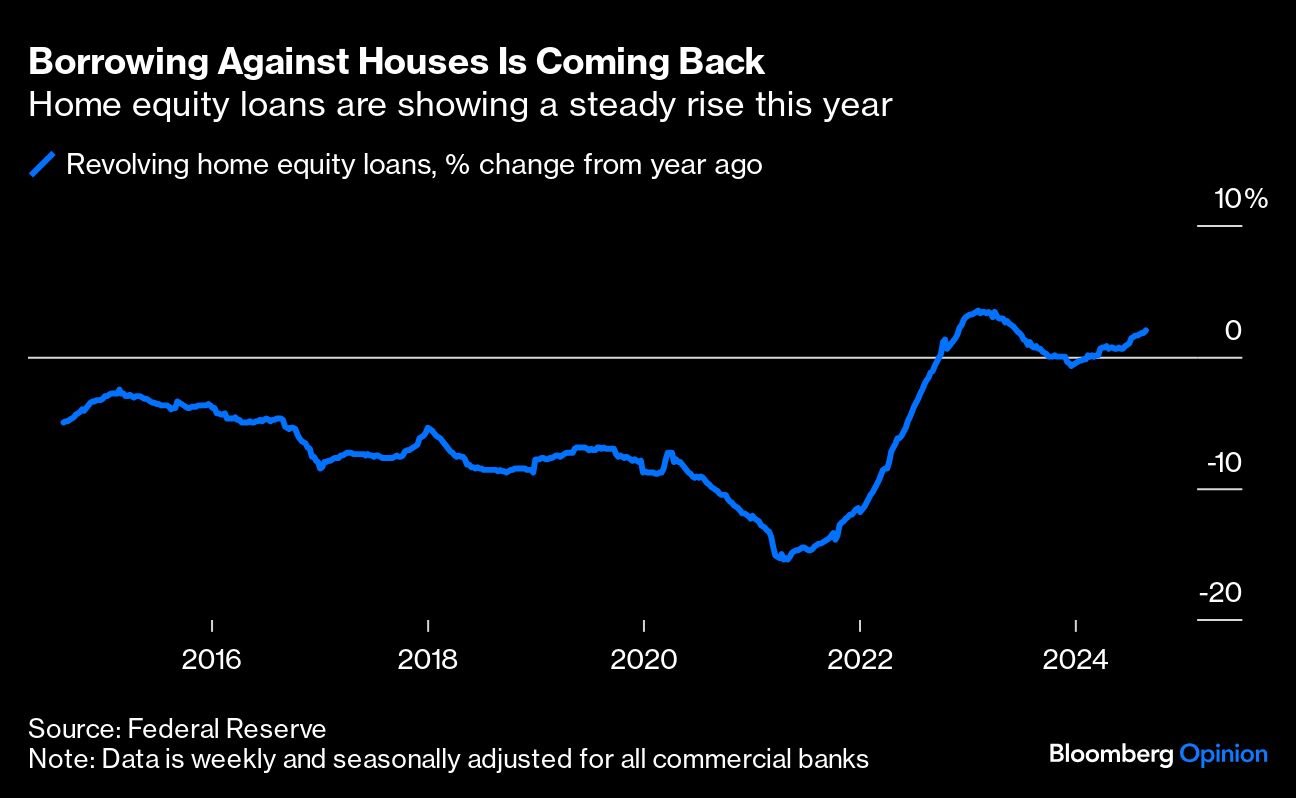

HELOC balances at banks shrank throughout the 2010s and even in the early 2020s as low mortgage rates incentivized full refinancings. Revolving home equity loans have been climbing by 1% or more, year over year, in recent weeks, indicating banks and borrowers are beginning to favor these products again.